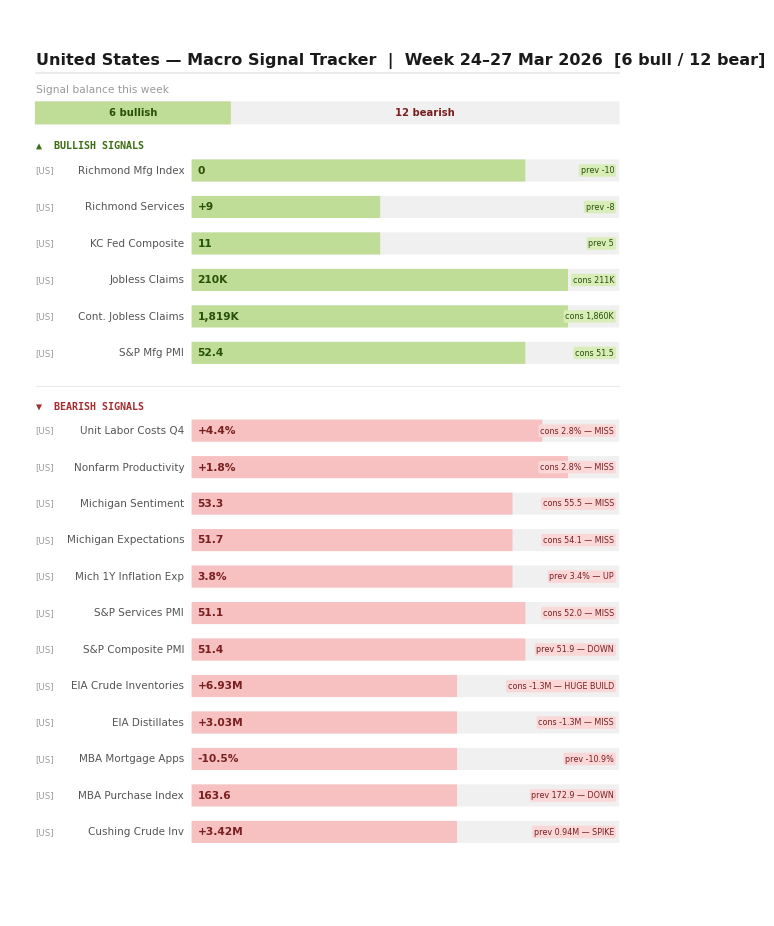

United States

The Richmond and KC Fed indices bouncing back from deeply negative readings look better than they are — both series mean-revert aggressively and carry almost no predictive weight for the next quarter. What actually deserves attention is the productivity-labour cost squeeze: output per worker grew at 1.8% when the market expected 2.8%, while unit labour costs came in at 4.4%. That gap is where margin compression lives, and it's the combination the Fed is most sensitive to right now. Michigan inflation expectations ticking up to 3.8% against a 3.4% prior tells you households are beginning to price in the Hormuz shock before it's fully arrived at the pump. The oil inventory build of nearly 7 million barrels against an expected draw is the one genuinely counterintuitive signal — domestic supply is accumulating at the precise moment global markets are screaming shortage. Tough path for Fed ahead. So far they have eased the markets by saying they are in 'no rush' to increase interest rates but this may not hold true if the wa drags on.

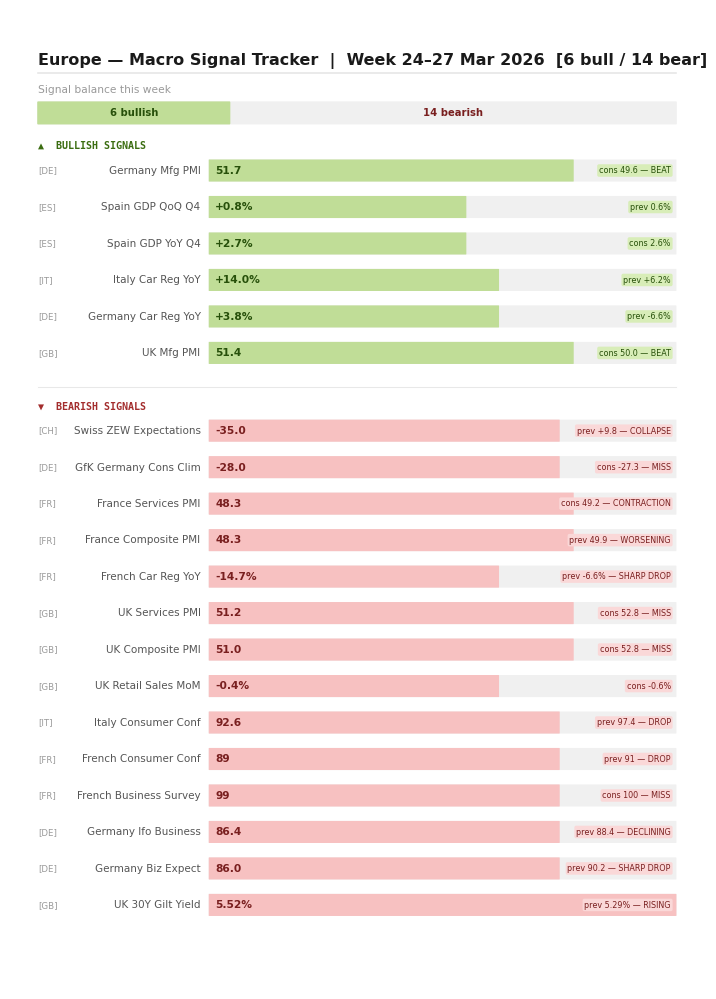

Europe

Germany at 51.7 on manufacturing — beating a sub-50 consensus — is the week's most consequential European print, not because it resolves anything but because it pushes back the recession narrative by another month. Spain growing at 2.7% year-on-year reinforces what has been true for several quarters: the eurozone's fiscal periphery is now its growth engine, which is a structural inversion that bond markets have not fully priced. France is the genuine concern. A services PMI at 48.3, contracting consumer confidence, and car registrations down nearly 15% year-on-year suggest a domestic demand problem that predates the energy shock and runs deeper than cyclical softness. The Swiss ZEW collapsing from +9.8 to -35.0 in a single reading is the number that should unsettle regional investors — financial sector expectations tend to lead the real economy by two to three quarters, and this is not a modest deterioration. Europe may be heading into a uniform slowdown with Germany and Spain holding while France accelerates toward something more serious.

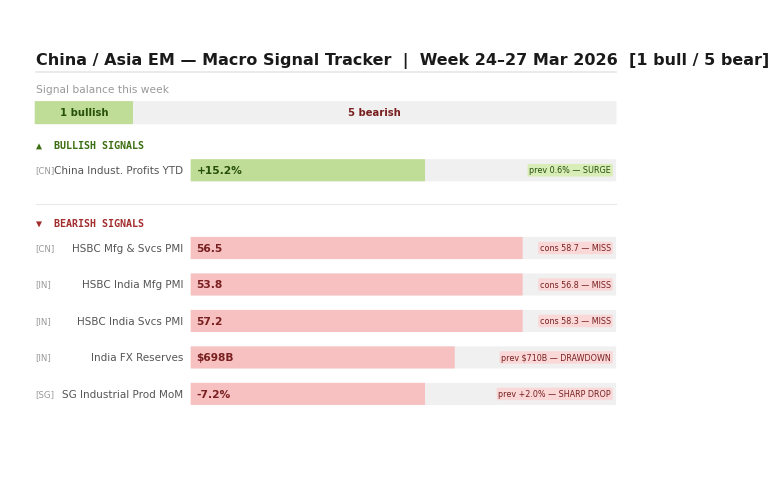

China / Asia EM

Industrial profits jumping from 0.6% to 15.2% year-on-year is the kind of number that invites scepticism before acceptance — but it's real, and it likely reflects a combination of commodity input cost relief and export volume recovery that has been building since late 2025. The more uncomfortable read is what the HSBC PMI misses say about forward momentum. India's composite came in at 56.5 against a 58.7 expectation, still expansionary but decelerating at precisely the moment the global energy shock is beginning to bite Asian import-dependent economies hardest. FX reserves slipping quietly to $698 billion from $710 billion suggests the RBI is intervening to defend the rupee — a pressure that will only intensify if oil stays above $100. China's data this week is too thin to draw a cycle conclusion, but the profit surge without a corresponding PMI beat is a classic late-cycle signal: margins recovering on cost tailwinds while forward orders soften. That divergence rarely sustains beyond two quarters.