Market and Outlook

We have already discussed Baker Hughes's (BKR) Q1 2026 financial performance in our recent article. Here is an outline of its strategies and outlook. Baker Hughes’s management expects global upstream spending to decline slightly more than previously forecast, mainly due to reduced Middle East activity. Spending in North America and other international regions is expected to remain broadly flat. Recovery depends on a resolution of the Middle East conflict by midyear, though uncertainty remains high. Over time, energy security concerns are likely to drive increased investment in diversified supply and energy infrastructure.

LNG Market and Power Business Outlook

Baker Hughes secured key gas infrastructure awards, including compression solutions in the Middle East and its first NovaLT deployment in South America. The company booked $1.2 billion in LNG equipment orders, highlighted by a major QatarEnergy contract for the North Field West project. This project includes significant turbine and compression equipment supporting 16 MTPA of capacity. The company is also seeing momentum in North America LNG, with a new agreement supporting an 8.4 MTPA export terminal offshore Texas.

In Q1, the company secured $1.4 billion in new energy orders, including a 1 GW data center project, supporting its $2.4–$2.6 billion 2026 target. It also won a major carbon capture contract in Qatar, involving compression systems to handle 4.1 million tonnes of CO2 annually.

Q2 Outlook

BKR’s Q2 revenue is expected to decline ~1.3% sequentially at the midpoint. Adjusted EBITDA is expected to decline ~2.4% QoQ at the midpoint. IET is expected to remain resilient with continued growth, while OFSE faces pressure from Middle East disruptions.

The company’s FY2026 performance will be influenced by backlog conversion, activity levels, and external factors such as FX and trade policy. For the year, IET is off to a strong start, supported by power and energy infrastructure demand. However, OFSE faces uncertainty due to ongoing geopolitical tensions, which may limit performance. Under a stable scenario, OFSE is expected to achieve the low end of its EBITDA guidance range.

Debt Raised

The balance sheet remains strong, with net debt to EBITDA at 0.32x and liquidity at $17.8 billion. The company raised $6.5 billion in U.S. bonds and €3 billion in European bonds to fund the Chart acquisition. It targets a net debt to EBITDA ratio of 1–1.5x within 24 months, supported by free cash flow and portfolio actions.

Relative Valuation

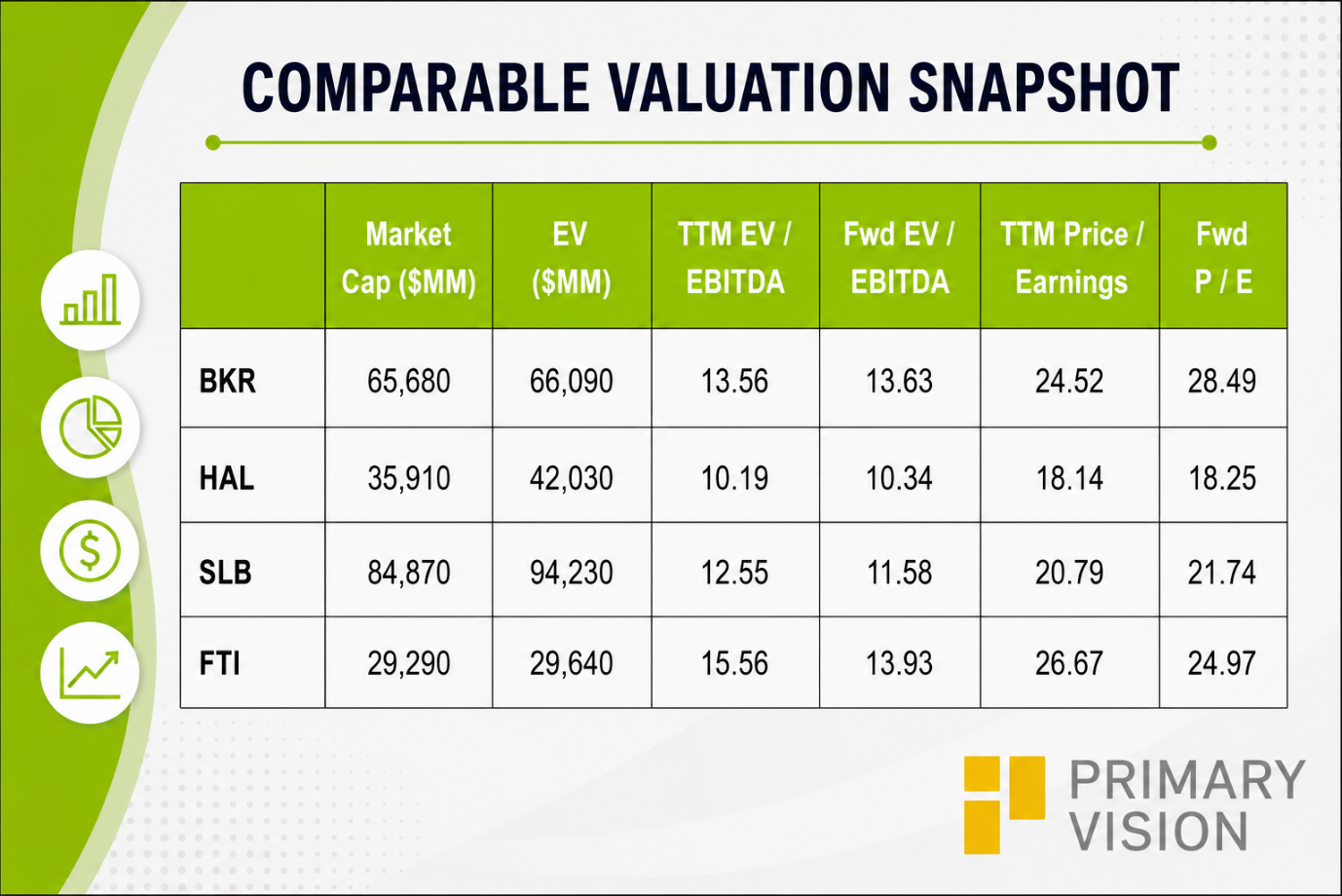

Baker Hughes is currently trading at an EV/EBITDA multiple of 13.6x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is nearly the same. The current multiple is higher than its five-year average EV/EBITDA multiple of 10.6x.

BKR's forward EV/EBITDA multiple versus the current EV/EBITDA is expected to remain unchanged compared to a decline in the multiple for its peers because the company's EBITDA is expected to remain unchanged versus a fall in EBITDA for its peers in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock's EV/EBITDA multiple is higher than its peers' (HAL, SLB, and FTI) average. So, the stock appears overvalued compared to its peers.

Final Commentary

BKR’s outlook is mixed, with Middle East disruptions weighing on upstream spending while other regions remain stable. LNG, gas infrastructure, and new energy orders are driving strong momentum, particularly in IET. Q2 is expected to see slight sequential declines, with IET resilience offsetting OFSE weakness. For 2026, IET is positioned for growth, while OFSE faces uncertainty from geopolitical risks. Overall, I believe a strong balance sheet and energy transition exposure support longer-term growth despite near-term volatility. The stock appears overvalued compared to its peers.