Outlook and Key Projects:

BP’s outlook reflects improving fundamentals but continued short-term volatility. Management expects upstream production to decline sequentially in Q2 due to seasonal maintenance and Middle East disruptions, while refining margins and customer volumes remain sensitive to geopolitical conditions. Over FY2026, production is expected to remain broadly flat, with oil stability offset by weaker gas and low-carbon volumes. Capital discipline remains central, with $13B–13.5B capex guidance and $9B–10B of divestments, including the Castrol transaction, supporting balance sheet improvement and portfolio simplification.

In Q1, BP signed a new exploration block agreement in the Red Sea and made a significant gas discovery offshore Egypt, alongside sanctioning the Harmattan gas development. In oil, the company delivered multiple project milestones, including production start-ups in Angola (Ndungu and Quiluma), continued development in the North Sea (Solveig Phase 2), and new exploration exposure in Namibia. The company advanced the planned divestment of the Gelsenkirchen refinery and ongoing progress toward the Castrol transaction.

The Q1 Results Analyzed

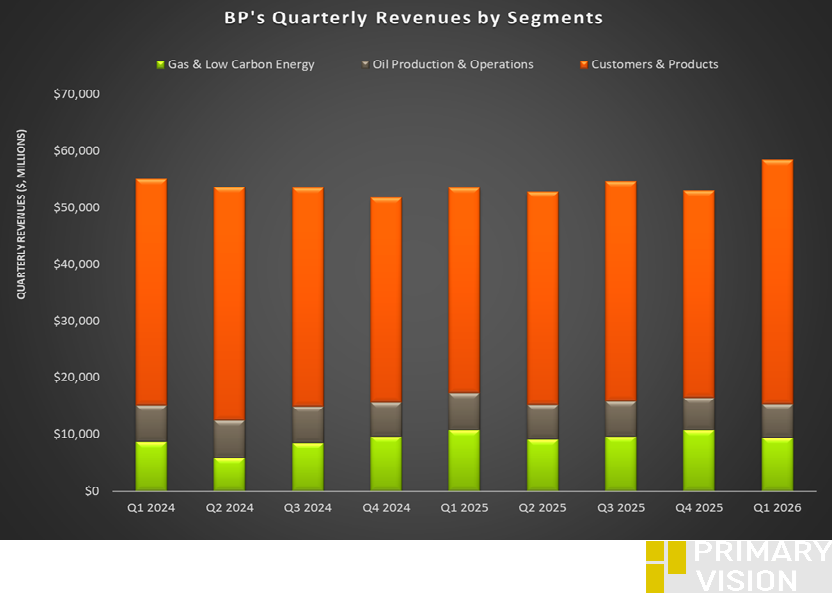

BP’s underlying RC (Replacement Cost) profit rose sharply to $3.2 billion in Q1 from $1.5 billion in Q4, driven by exceptional oil trading and stronger refining margins. Customers & Products was the standout segment, with 18% higher sales and underlying profit increasing significantly due to improved refining performance, higher throughput, and strong midstream optimization.

Upstream earnings remained broadly stable sequentially, as higher realizations offset portfolio impacts, including the North Sea divestment. Net income rebounded to $3.8 billion from a loss in Q4, reflecting both operational improvement and the absence of prior impairments. RC profit reflects BP’s underlying operating earnings, excluding inventory holding gains or losses caused by commodity price movements.

Cash Flows and Buyback

Operating cash flow remained broadly flat year-over-year but was weighed down by a significant working capital build driven by higher prices and seasonal inventory effects. Net debt increased by 13% in Q1, highlighting short-term balance sheet pressure despite stronger earnings. BP continues to prioritize dividend stability and plans to reduce hybrid debt by ~$4.3 billion, reinforcing its focus on deleveraging.

Thanks for reading the BP Take Three, designed to give you three critical takeaways from WFRD's earnings report. Soon, we will present a second update on BP’s earnings, highlighting its current strategy, recent news, and notes from our deeper dive.