Articles

- BLOG / Articles / View

- Articles

From AI to Oilfield Power: The AI Power Stack

By Avik on July 1, 2026 in Articles

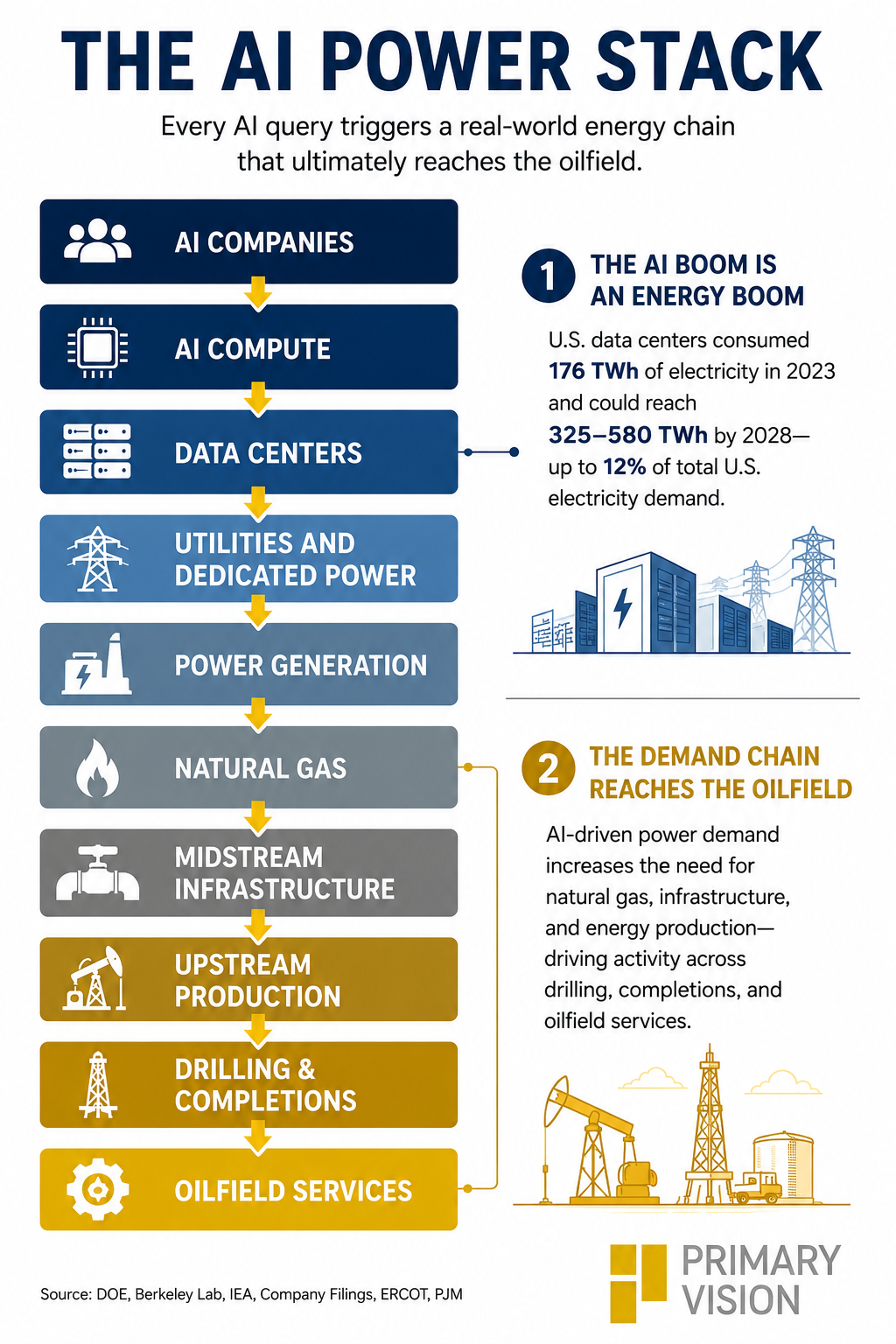

Introducing the AI Power Stack

Artificial intelligence is creating one of the largest new sources of electricity demand in decades. While most investors focus on semiconductors, cloud providers, and data centers, the infrastructure required to support AI extends much further. This article is the first installment in a six-part series examining how AI demand propagates through the energy ecosystem. We introduce the AI Power Stack—a framework that connects AI compute to data centers, utilities, power generation, natural gas infrastructure, and ultimately oilfield services.

Most investors focus on the first few layers of the stack. Yet every layer depends on the one below it, creating a demand chain that extends far beyond the technology sector.

AI Creates A New Horizon

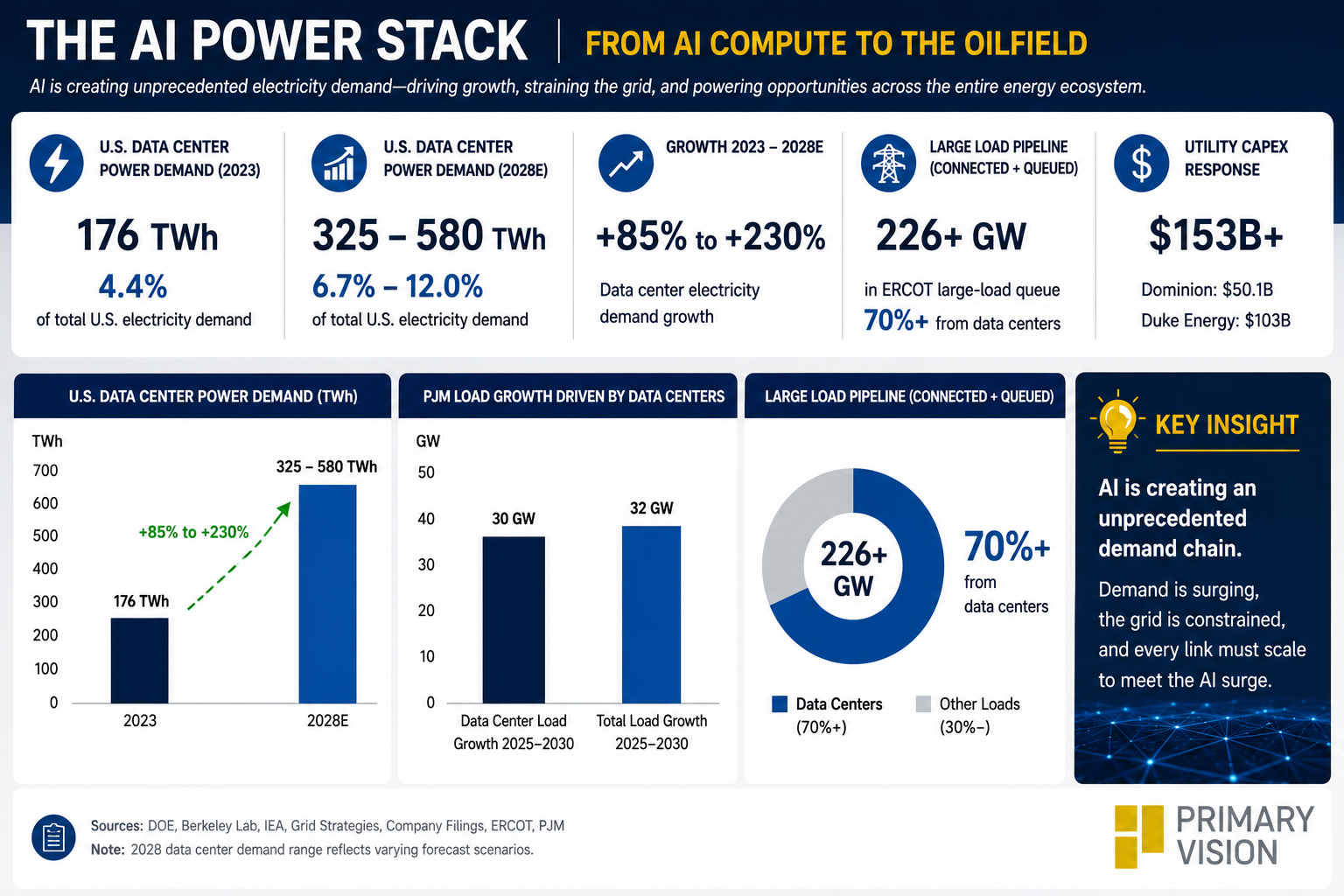

Artificial intelligence is creating one of the largest new sources of electricity demand in decades. U.S. data centers consumed 176 TWh of electricity in 2023, accounting for roughly 4.4% of total U.S. power demand. By 2028, that figure could rise to 325–580 TWh, representing 6.7%–12.0% of all electricity consumed in the country.

Those forecasts explain why investors are increasingly focused on data centers, utilities, and power generation. Yet the AI story extends far beyond electricity. Every AI query triggers a demand chain that reaches power plants, natural gas pipelines, upstream producers, and ultimately the oilfield.

AI Is Creating Utility-Scale Demand

The scale of AI infrastructure has changed dramatically. Traditional hyperscale data centers typically required 100–300 MW of power. Today’s AI campuses are increasingly being designed around 500 MW to 1 GW loads, while several proposed projects exceed multiple gigawatts. At those levels, a single data center can rival the electricity consumption of a midsized city.

The result is a fundamental shift in power planning. For much of the past two decades, electricity demand growth remained relatively modest. Utilities now face large-load requests measured in gigawatts rather than megawatts, forcing them to accelerate generation, transmission, and distribution investments. AI is no longer simply a technology deployment story. It is becoming an infrastructure buildout story.

Utilities Are the First Beneficiaries

The first companies seeing the impact are utilities. Dominion Energy, which serves Northern Virginia’s data-center corridor, forecasts approximately 4.2 GW of data-center billing demand and reported a 19 GW increase in contracted capacity from data-center customers. The company subsequently increased its five-year capital plan to $50.1 billion.

Duke Energy has secured roughly 4.5 GW of data-center load and expanded its capital plan to $103 billion as it prepares for accelerating demand growth. NextEra Energy has reported a 6 GW technology and data-center backlog and has discussed the potential for up to 30 GW of dedicated data-center hubs by 2035.

These numbers demonstrate that AI demand is already reshaping utility investment plans. The first beneficiaries of AI are not necessarily AI companies themselves. They are often the utilities responsible for supplying power.

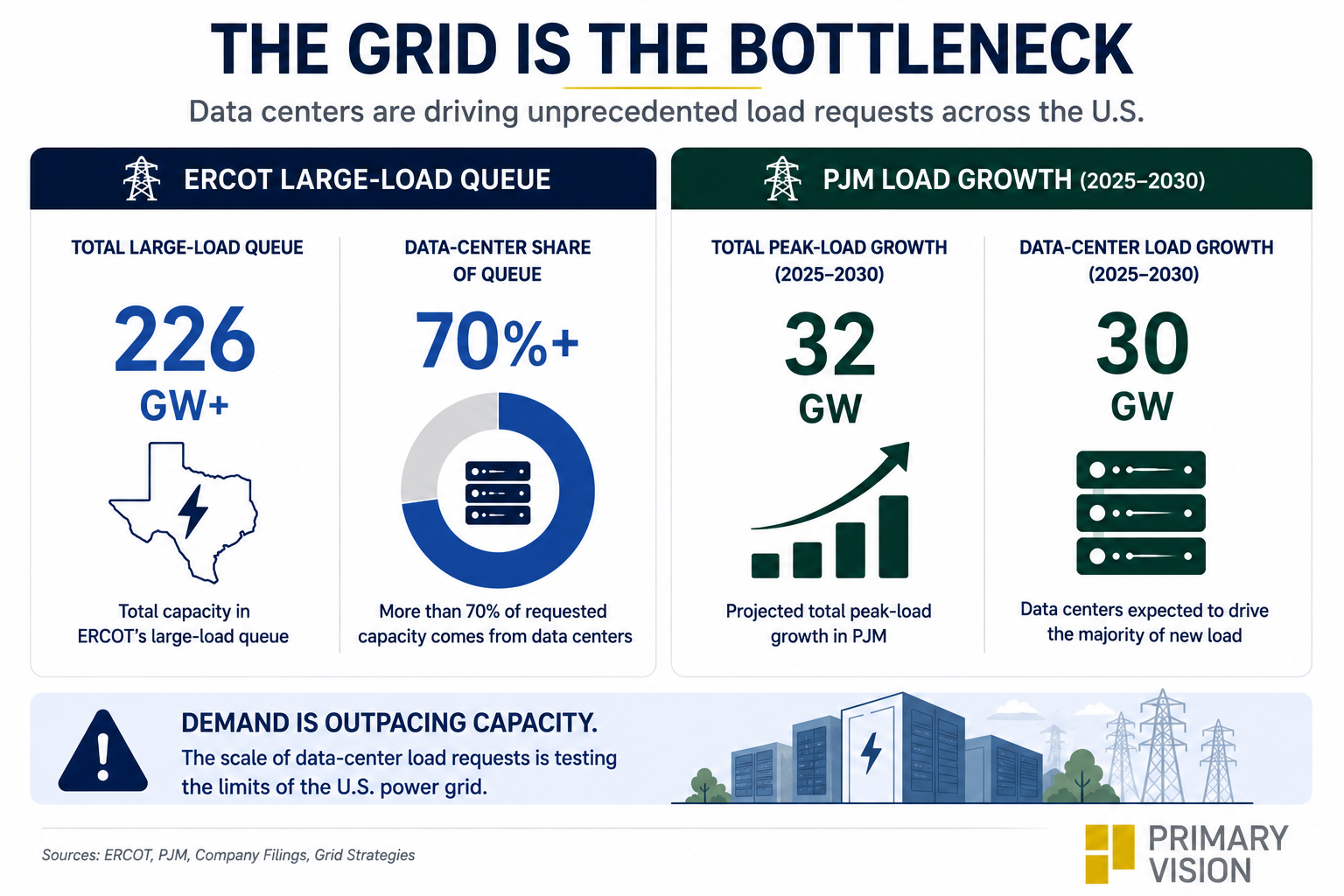

The Grid Is Struggling to Keep Pace

Demand growth is occurring faster than power infrastructure can be deployed. ERCOT’s large-load queue has surpassed 226 GW, with data centers accounting for more than 70% of requests. In PJM, data centers are expected to drive approximately 30 GW of the region’s projected 32 GW of load growth through 2030.

The bottleneck extends beyond transmission and interconnection queues. Turbine manufacturers report significant backlogs, while developers increasingly face multi-year waits for new power capacity. The challenge is not whether demand exists. The challenge is how quickly the power system can respond. This mismatch between AI deployment timelines and utility development timelines is becoming one of the defining themes of the AI infrastructure market.

AI Demand Becomes Fuel Demand

Electricity demand ultimately becomes fuel demand. While renewables, storage, and nuclear power will all contribute to the solution, natural gas remains one of the most scalable and dispatchable sources of power available today. As a result, much of the incremental demand associated with AI is expected to flow through the natural gas value chain.

Using a representative gas-fired generation framework, every 1 GW of continuous AI load requires approximately 0.18 Bcf/d of natural gas demand. At 10 GW, demand rises to roughly 1.8 Bcf/d. At 20 GW, demand approaches 3.6 Bcf/d.

For context, 3.6 Bcf/d would represent a meaningful source of incremental demand for the U.S. gas market and would require additional production, gathering, processing, and transportation capacity. The AI boom is therefore creating opportunities not only for utilities and power generators, but also for natural gas producers and pipeline operators.

Conclusion

The AI boom is often framed as a battle among software developers, cloud providers, and chip manufacturers. Increasingly, however, it is becoming a power story. Data-center electricity demand is projected to rise sharply over the next several years, forcing utilities, power developers, and fuel suppliers to expand at an unprecedented pace.

The next question is no longer whether AI will require more power—it is who can deliver that power at the scale and speed the market now demands.

Sources

Berkeley Lab, United States Data Center Energy Usage Report

International Energy Agency (IEA), Energy and AI

Grid Strategies, National Load Growth Report

Dominion Energy Investor Presentations and Earnings Materials

Duke Energy Investor Presentations and Earnings Materials

NextEra Energy Investor Presentations and Earnings Materials

ERCOT Large Load Interconnection Queue Data

PJM Load Forecasts and Planning Materials

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform