Articles

- BLOG / Articles / View

- Articles

Liberty Energy's Perspective in Q1 2026: KEY Takeaways

By Avik on May 11, 2026 in Articles

Industry Outlook

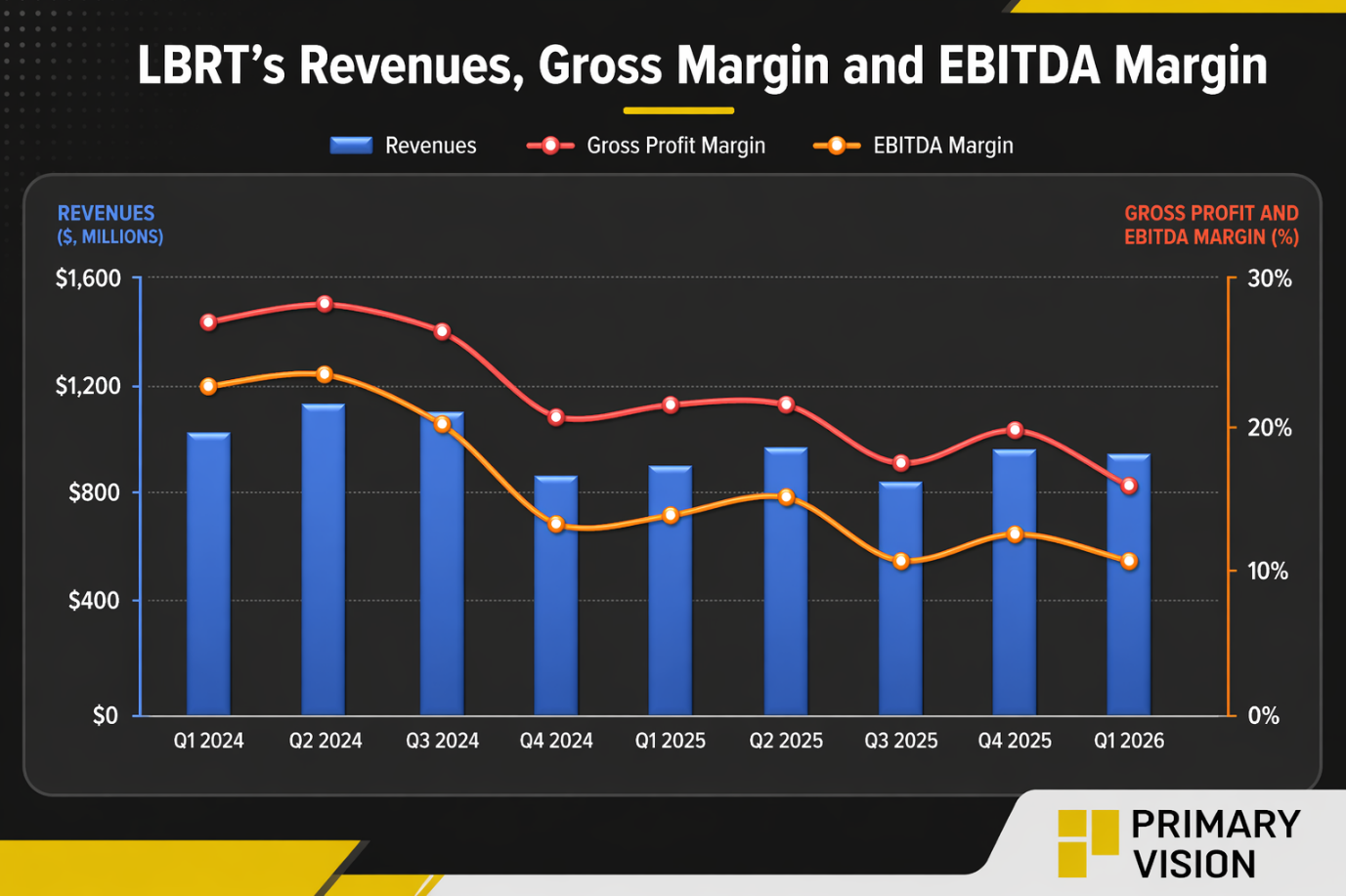

We have already discussed Liberty Energy's (LBRT) Q1 2026 financial performance in our recent article. Here is an outline of its industry outlook. Geopolitical conflict in the Middle East is raising supply risks and pushing oil prices higher. LNG markets may also face multi-year constraints due to damage to key infrastructure.

Asia is feeling the sharpest impact, with supply tightness forcing demand rationing. North America is emerging as a more reliable supplier, benefiting from shifting global energy dynamics. Higher oil prices are improving E&P economics and tightening the balance between frac supply and demand..

Fracking Business & Technology

North American oilfield activity appears to have reached a cyclical floor, with momentum beginning to improve. Supply disruptions and energy security concerns are driving a more constructive outlook for frac demand. Improving frac demand from private E&Ps and accelerated DUC activity is driving an earlier-than-expected pricing recovery.

On the technology side, DigiPrime represents a key innovation with 100% natural gas engines and variable speed capability. Upgrades to existing fleets will expand these capabilities across a majority of assets. Overall, these advancements improve efficiency, lower costs, and strengthen competitive positioning.

Top of Form

Bottom of Form

Power Solutions Business Outlook

LBRT’s management sees that the demand for distributed power is accelerating as grid constraints and AI-driven infrastructure needs push hyperscalers toward on-site solutions. This shift is supported by policy mandates and increasing demand for integrated, end-to-end power systems. Liberty is gaining traction with turnkey solutions, backed by advanced testing capabilities and AI-driven control systems to ensure reliability and performance.

The company is scaling its platform toward a 3 GW power deployment target by 2029, supported by long-term project pipelines and milestone-driven execution. To fund this growth, Liberty raised $1.3 billion in convertible debt. So, the power business is emerging as a multi-year growth engine, reinforced by energy security concerns and structural shifts in global supply dynamics

Company Outlook

In Q2, the company expects sequential revenue growth and improved profitability driven by higher utilization and prior strategic investments. U.S. power demand is accelerating rapidly, with Texas grid demand projected to quadruple by 2032, driving the adoption of distributed power solutions. Hyperscalers are increasingly shifting toward on-site generation to bypass grid constraints. Liberty is positioned as a key infrastructure provider enabling this transition with scalable, decentralized power systems.

Relative Valuation

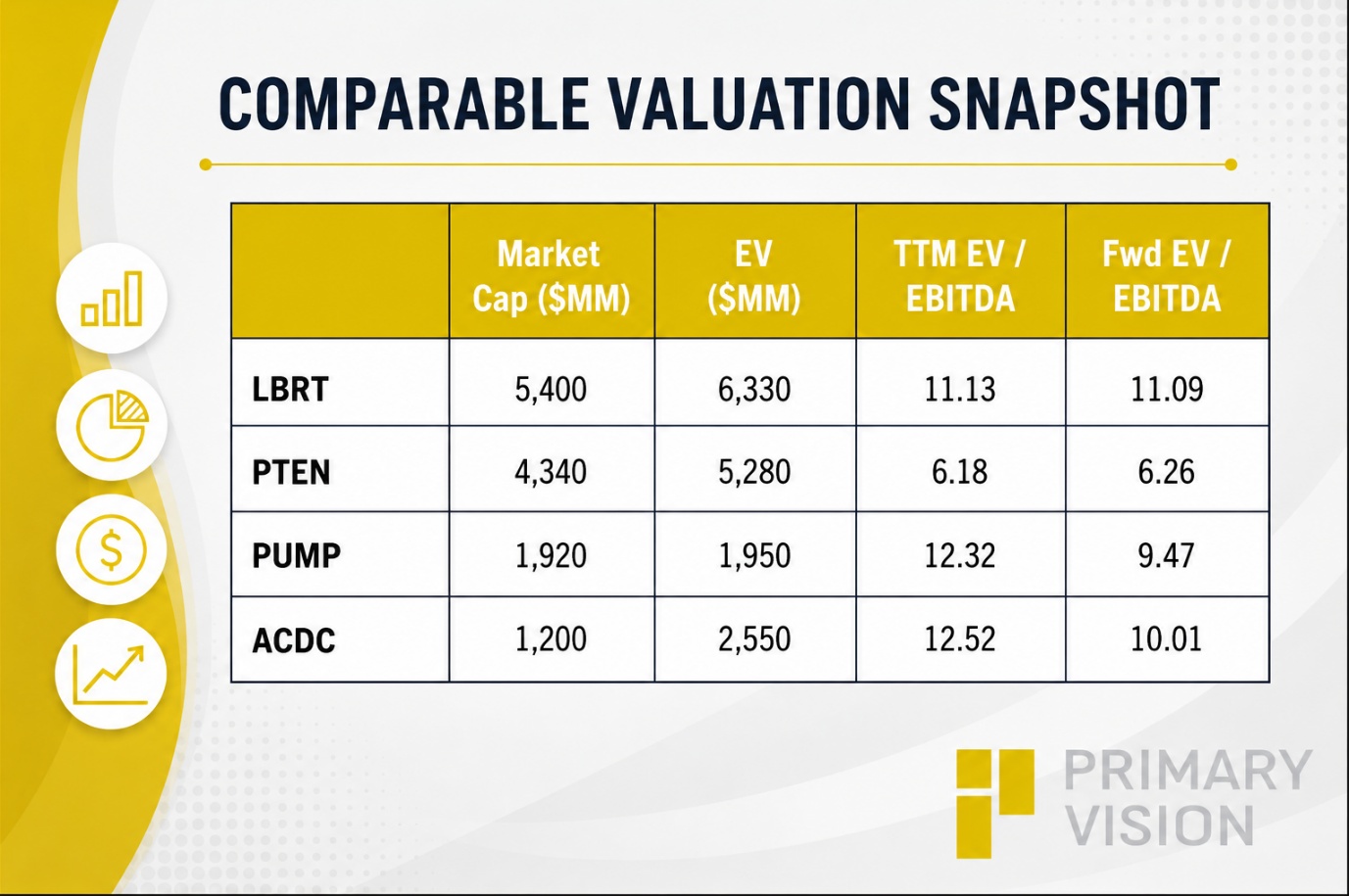

Liberty is currently trading at an EV/EBITDA multiple of 11.1x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is nearly unchanged. The current multiple is higher than its five-year average EV/EBITDA multiple of 9.8x.

LBRT's forward EV/EBITDA multiple versus the current EV/EBITDA is unchanged compared to a fall in the multiple for its peers because the company's EBITDA is expected to remain unchanged versus a rise in EBITDA for its peers in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock's EV/EBITDA multiple is higher than its peers' (PTEN, PUMP, and ACDC) average of 10.3x. So, the stock appears to be overvalued compared to its peers.

Final Commentary

LBRT views that the energy industry backdrop is turning more constructive, with geopolitical risks tightening supply and supporting higher oil prices. North America is benefiting from this shift, with improving frac demand and a more balanced supply environment. Liberty’s technology, particularly DigiPrime, is enhancing efficiency and strengthening its competitive positioning.

At the same time, the power business is emerging as a key growth driver, supported by rising demand for distributed energy and a 3 GW build-out target. Overall, I believe Liberty is well-positioned to benefit from both the cyclical recovery in frac and the structural growth in power solutions. Compared to its peers, the stock appears overvalued.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform