Key Developments and Outlook: NBR’s management expects US onshore activity to continue improving, with rig count projected to exit Q2 at ~69 rigs and remain stable through year-end. International growth remains supported by SANAD newbuild deployments, with four additional rigs scheduled in 2026 and continued expansion in Latin America and the Middle East.

However, cost pressures in the Middle East and logistics constraints are expected to persist, limiting margin expansion despite stable utilization. Capital spending remains disciplined at $730M–$760M for 2026, with a significant portion tied to contracted international rigs, reinforcing visibility but also anchoring capital intensity.

Key Drivers in Q1

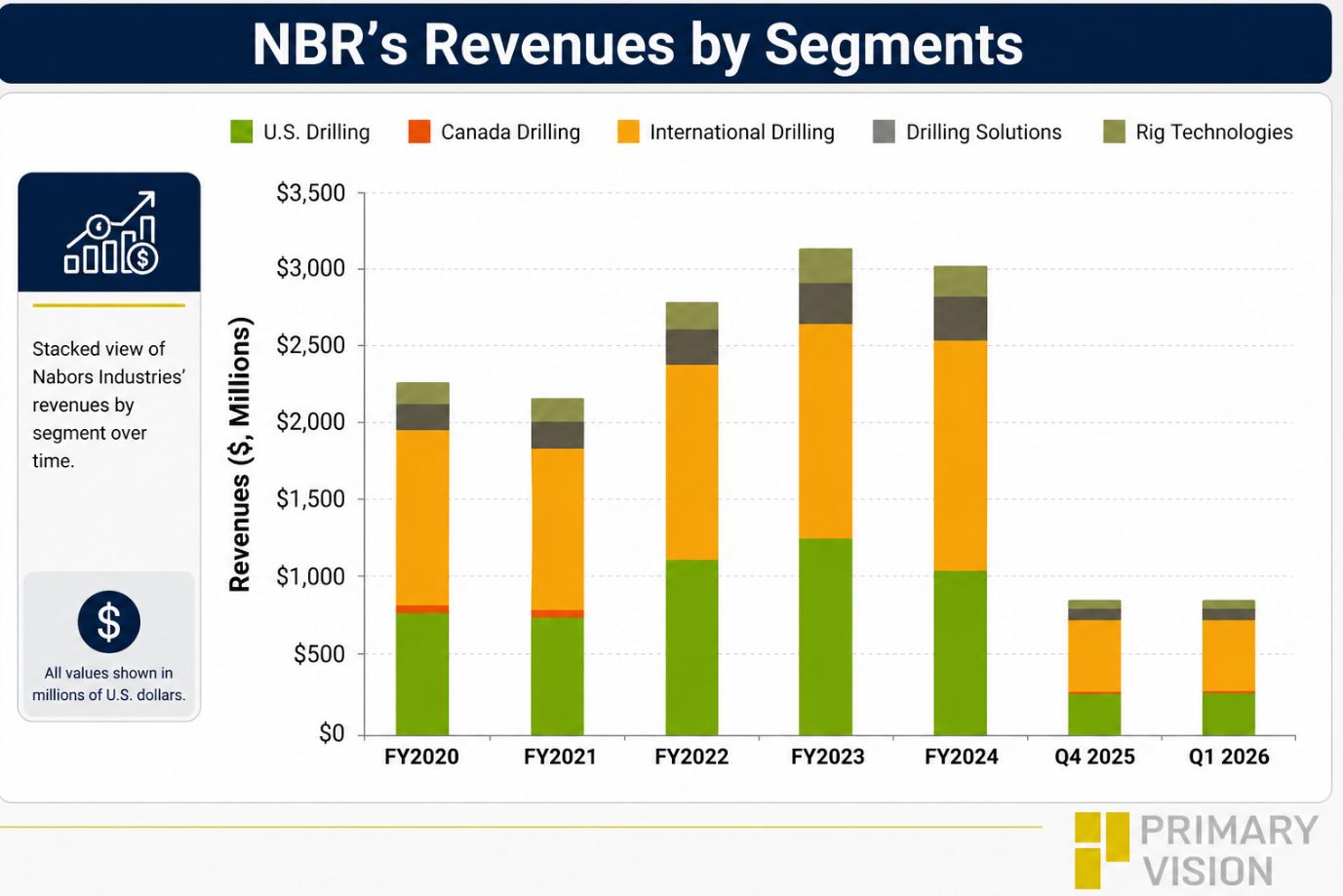

Quarter over quarter, NBR’s U.S. Drilling EBITDA declined ~6% in Q1 despite a ~9% increase in onshore count, indicating weaker pricing and mix. International Drilling EBITDA declined ~8% QoQ, with higher operating costs and activity disruptions offsetting stable utilization.

Drilling Solutions EBITDA declined ~6% QoQ as international growth was offset by lower U.S. third-party activity. Rig Technologies' EBITDA declined (from $5 million to near breakeven), reflecting weaker aftermarket demand and logistical delays. The net loss of $15 million in Q1 reflects both lower operating income and continued interest burden.

Debt was reduced: Nabors continues to prioritize balance sheet improvement, reducing total debt to $2.1 billion, with no maturities until 2029. Since year-end 2024, the company has reduced debt by $386 million. Capital allocation remains disciplined, with FY2026 capex guided at $730M–$760M, largely tied to contracted international deployments.

Thanks for reading the NBR Take Three, designed to give you three critical takeaways from NBR's earnings report. Soon, we will present a second update on NBR's earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.