Articles

- BLOG / Articles / View

- Articles

Patterson-UTI's Perspective in Q1 2026: KEY Takeaways

By Avik on May 15, 2026 in Articles

The Market Outlook

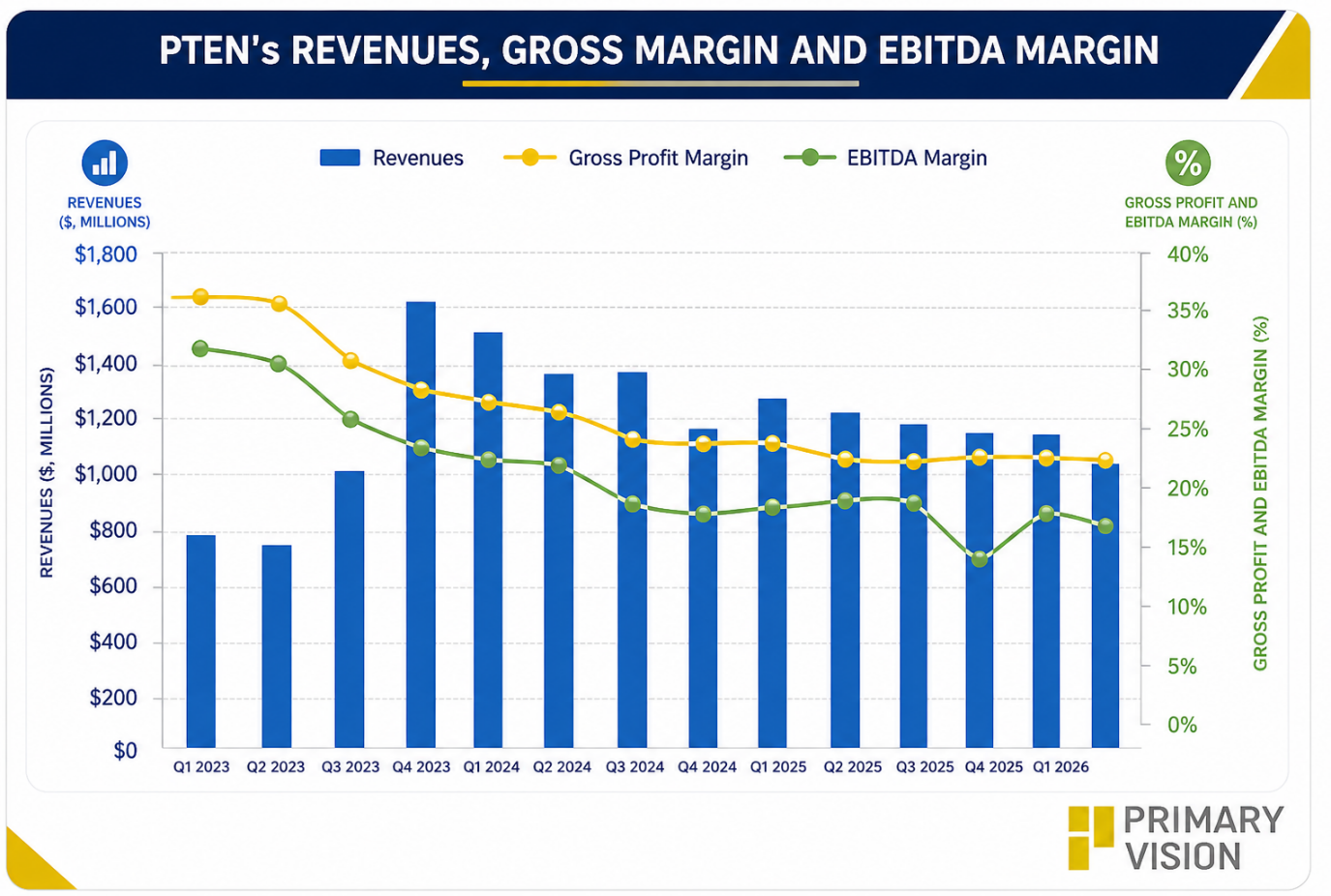

We discussed our initial thoughts about Patterson-UTI Energy's (PTEN) Q1 2026 performance in our short article a few days ago. This article will dive deeper into the industry and its current outlook. According to PTEN’s management, geopolitical disruptions and oil supply risks have shifted the commodity outlook, reinforcing the importance of U.S. shale and a diversified global energy supply. As U.S. shale activity begins to recover, it expects to benefit from prior investments and positioning. While open to expanding into new geographies and product lines, it remains disciplined on capital allocation and returns.

The industry outlook is improving, though the pace of recovery remains uncertain. Higher oil prices are expected to drive increased U.S. drilling and completion activity, with early signs of customers planning higher activity levels. Private operators are responding faster, and sustained pricing could support stronger activity into 2027. Natural gas demand is also set to rise, likely requiring increased drilling and completions as LNG exports expand.

Completion and Pressure Pumping Scenario

Completion demand is improving, with stronger momentum expected in the second half of 2026 as utilization tightens and pricing discussions gain traction. It indicated natural gas fleets are “sold out” / near full utilization. It has ~250,000 cold-stacked horsepower that could be reactivated. Available frac capacity remains constrained, and reactivating older diesel frac spreads is uneconomical at current pricing, requiring materially higher rates to justify incremental supply. The company is prioritizing high-grading its frac spreads, directing capital toward its Emerald fracs of 100% natural gas-powered assets, while allowing legacy horsepower to decline.

By year-end, more than 15% of active horsepower is expected to be fully natural gas-powered, with roughly 90% at least partially gas-powered. This reinforces a shift toward higher-efficiency, premium fleets. Industry consolidation and capital constraints among smaller players continue to widen the gap between high-spec and legacy equipment. It supports a more disciplined and structurally stronger completions market.

Drilling Activity Outlook

Rig activity is expected to increase, with exit rates in Q2 approaching the highest levels of the year. Demand is being driven by more complex wells, including deeper targets and longer laterals. This is increasing the importance of high-spec rigs, where supply remains limited and concentrated among top-tier contractors.

Q2 Outlook & Segment Guidance

PTEN’s management expects the U.S. shale activity to increase starting late Q2 and build through the second half, even if oil prices moderate. The company will continue prioritizing technology investments in completions over reactivating older equipment. In drilling, rig count is expected to average around 90 in Q2, exiting higher as rigs are reactivated, with modest near-term cost drag.

Completion Services is expected to operate at near full utilization, supporting stable profitability. Drilling Products margins are likely to soften slightly due to international weakness and seasonal impacts in Canada.

Relative Valuation

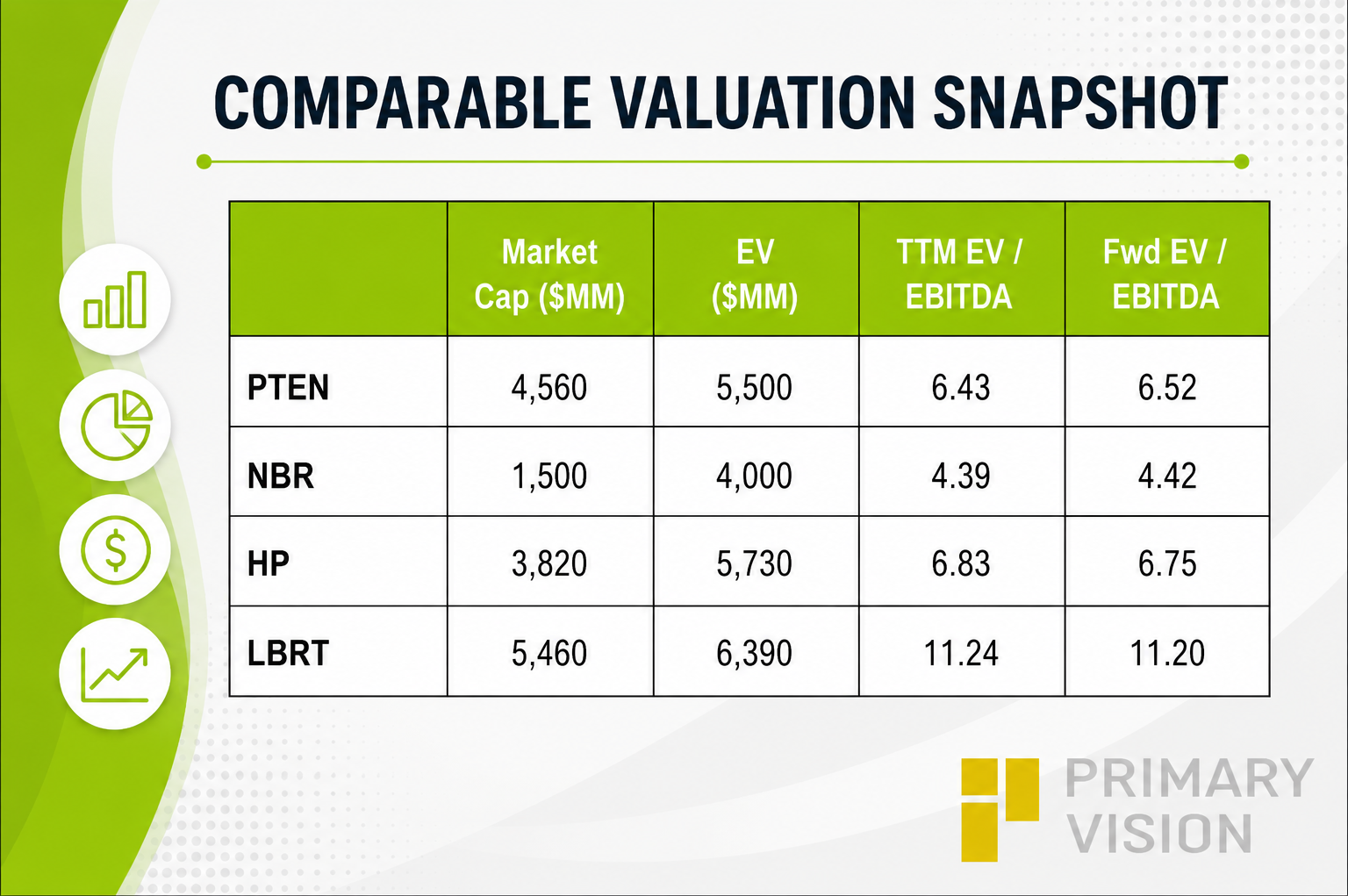

PTEN is currently trading at an EV/EBITDA multiple of 6.4x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 6.5x. The current multiple is lower than its past five-year average EV/EBITDA multiple of 8.0x.

PTEN's forward EV/EBITDA multiple is expected to marginally expand versus the current EV/EBITDA. This contrasts with the unchanged multiple for its peers, as the company's EBITDA is expected to decrease, whereas peers' EBITDA is expected to remain steady in the next year. This typically results in a slightly lower EV/EBITDA multiple. The stock's EV/EBITDA multiple is lower than its peers' (NBR, HP, and LBRT) average of 7.5x. So, the stock is reasonably valued, with a negative bias, compared to its peers.

Final Commentary

Geopolitical risks and supply disruptions are reinforcing the strategic importance of U.S. shale and a diversified energy mix. The industry outlook is improving, with higher oil prices supporting a recovery in drilling and completions, though the pace remains uncertain. Completion demand is tightening, with limited frac supply and rising pricing discussions pointing to a stronger second half of 2026. PTEN is prioritizing high-spec, natural gas-powered fleets, accelerating the shift toward premium equipment and away from legacy diesel assets.

Drilling activity is also set to increase, driven by more complex wells and constrained availability of high-spec rigs. Overall, the setup points to a gradual but structurally improving cycle, with activity and pricing expected to strengthen into 2027. The stock is reasonably valued, with a negative bias, compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform