Pressure Pumping Outlook

In our recent article, we have already discussed RPC's (RES) Q1 2026 financial performance. Here is an outline of its outlook. RES’s (Cudd Energy) management said current pricing still does not justify reactivating stacked frac fleets despite improving oil prices and reduced calendar white space. They see Middle East-related commodity strength as incrementally positive, with pricing pressure beginning to stabilize.

However, customer activity remains constrained by cautious operator spending and natural gas takeaway limitations in New Mexico. Management emphasized that any fleet reactivation would require stronger pricing visibility, longer-duration work, and sufficient volumes to support acceptable returns. For now, the company prefers maximizing pricing and utilization on existing active fleets rather than leaning into reactivating cold-stacked spreads.

Which Drivers Come To The Forefront?

Metal Max (all-metal downhole motor power section) is expanding into applications previously dominated by conventional power section components. Management sees significant additional displacement potential as customers increasingly recognize the product’s performance and value advantages. Investors may note that RPC’s Thru Tubing Solutions segment is increasingly using Metal Max to displace conventional power sections. However, it still represents only about 15% of total power section utilization, leaving significant room for adoption growth.

RES’s Thru Tubing Solutions is seeing accelerating adoption of its Metal Max metal-on-metal power section across more regions and motor sizes as inventory availability improves. The downhole tools business is also benefiting from growing adoption of its on-plug and surface vibratory technologies, particularly as longer laterals increase completion complexity.

Q1 Drivers

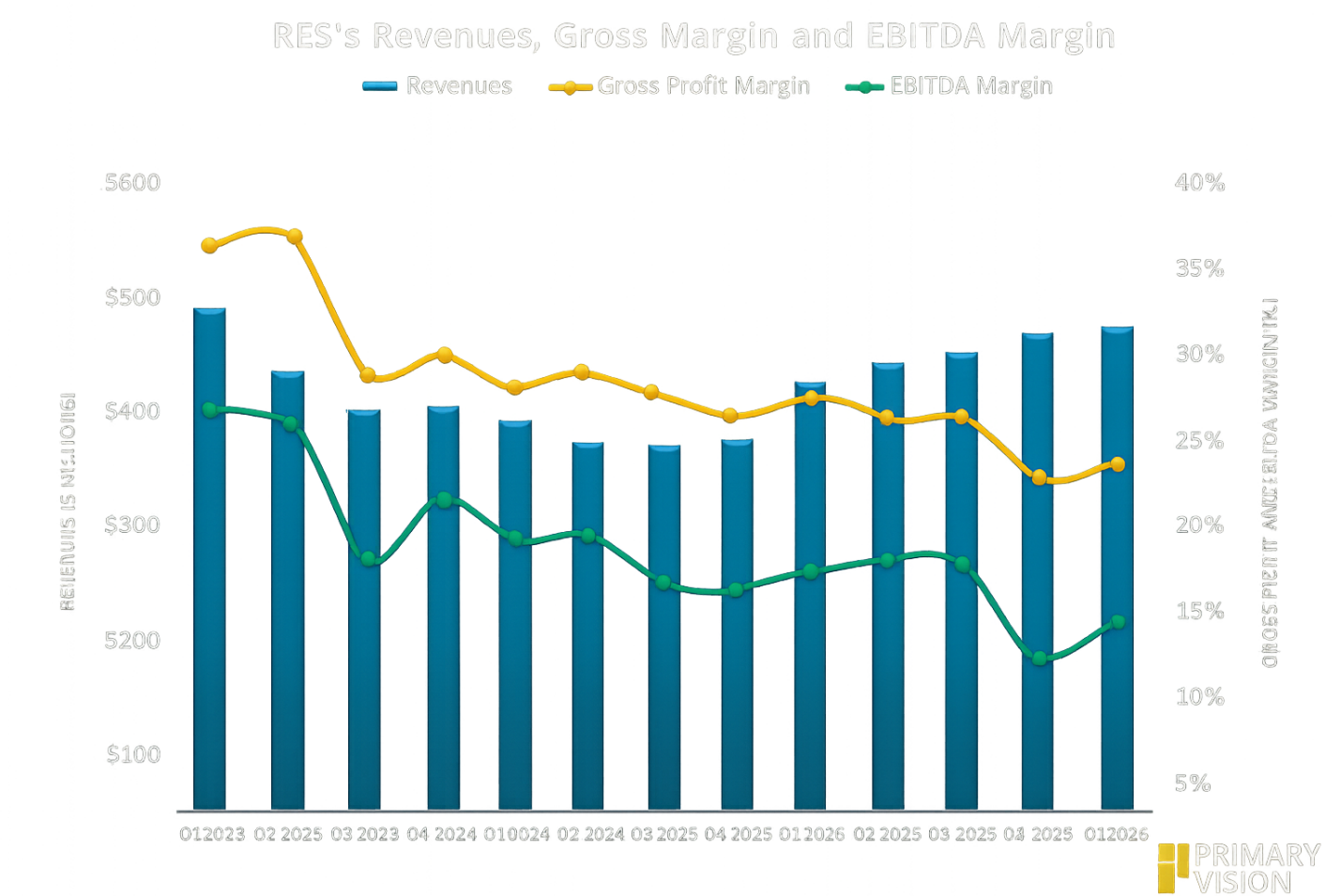

RES’s Q1 results improved sequentially across most service lines despite weather disruptions early in the quarter, with activity strengthening as the quarter progressed. Thru Tubing Solutions’ downhole tools revenue increased 11% sequentially, supported by double-digit growth across most geographic regions. Management attributed the performance to its expanding portfolio of proprietary completion technologies and continued new product introductions.

Relative Valuation

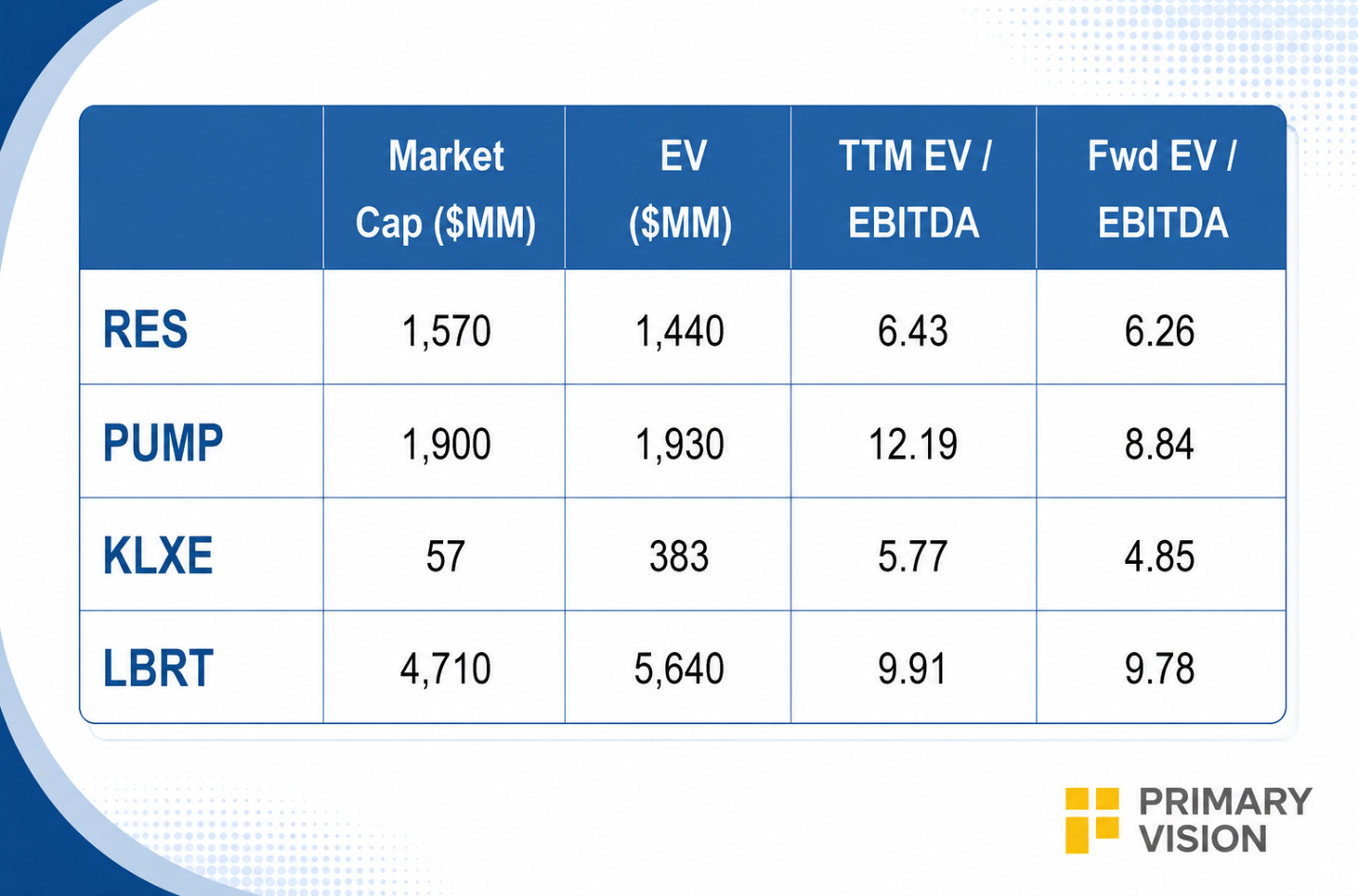

RES is currently trading at an EV/EBITDA multiple of 6.4x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 6.3x. The current multiple is significantly lower than its five-year average EV/EBITDA multiple of 12.5x.

RES's forward EV/EBITDA multiple is expected to contract less steeply than its peers. This implies that the company's EBITDA is expected to increase less sharply than its peers in the next four quarters. This typically results in a lower EV/EBITDA multiple. The stock's EV/EBITDA multiple is lower than its peers' (PUMP, KLXE, and LBRT) average of 9.3x. So, the stock appears reasonably valued compared to its peers.

Final Commentary

RPC’s pressure pumping outlook remains cautious. Management sees recent oil price strength and easing pricing pressure as incrementally positive, although operator spending discipline and New Mexico gas takeaway constraints continue to limit activity recovery. Instead of adding idle capacity, the company is prioritizing pricing improvement and utilization gains on existing active fleets.

Meanwhile, Thru Tubing Solutions continues to emerge as a key growth driver through accelerating the adoption of its Metal Max all-metal power section technology. RES’s Q1 performance also reflected growing momentum in proprietary downhole tools. The stock appears reasonably valued compared to its peers.