Articles

- BLOG / Articles / View

- Articles

SLB's Perspective in Q1 2026: KEY Takeaways

By Avik on May 18, 2026 in Articles

The Market Outlook

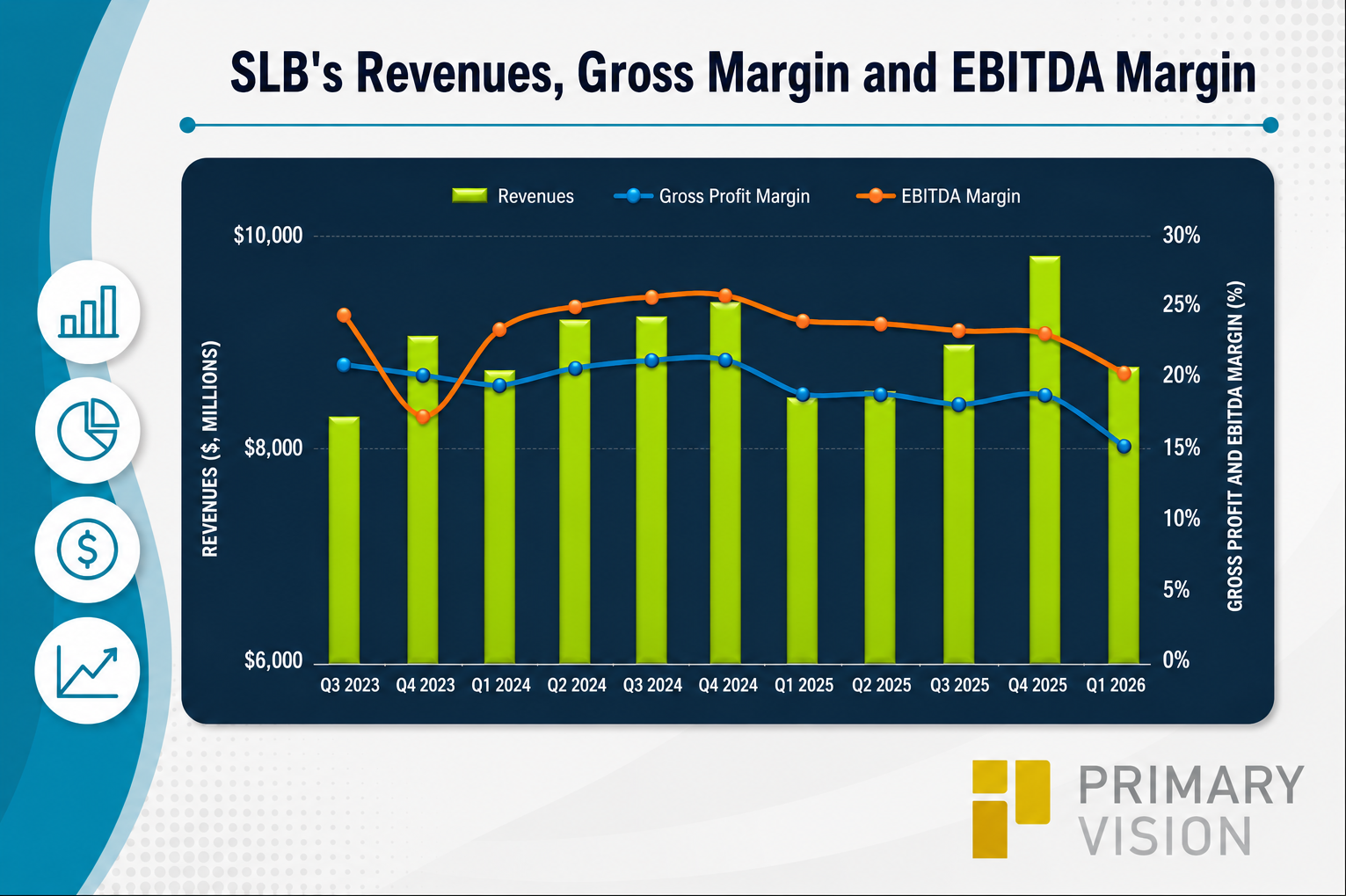

We have already discussed SLB's (SLB) Q1 2026 financial performance in our recent article. Here is an outline of the macro energy environment and the company’s strategies in a changing scenario. Oil prices are expected to remain above pre-conflict levels due to significant supply disruptions. Energy security concerns will drive increased investment in domestic production and inventory rebuilding. This should support a constructive environment for upstream activity over the coming years. In the near term, recovery will be gradual and uneven across regions, led by efforts to restore Middle East production capacity.

Short-cycle activity is expected to strengthen first, particularly in North America and Latin America. Well intervention work should also increase as operators seek quick production gains. At the same time, long-cycle offshore and deepwater projects are likely to gain momentum, supporting higher FID approvals and exploration activity.

Digital and Data Center Push

SLB completed the ChampionX acquisition in July 2025, which strengthened its capabilities in production chemicals and artificial lift. SLB’s digital and AI business is gaining momentum and driving long-term differentiation. AI and data are embedded across workflows to improve performance across the full reservoir life cycle. Adoption is increasing as agentic AI use cases expand and prove value in the field.

Digital is expected to become a key growth driver, both standalone and across the broader portfolio. Data centers are emerging as a new opportunity, supported by SLB’s engineering and execution capabilities. Although early-stage, this segment shows strong demand and potential to become a meaningful earnings contributor.

Challenges

Q1 was impacted by severe Middle East disruptions, leading to shutdowns and reduced activity.

Operational suspensions were most pronounced in Qatar and Iraq, with broader regional impacts from offshore disruptions. Unfavorable activity mix and higher costs, particularly in OneSubsea, further pressured results. Production Systems and Digital segments grew year-over-year, supported by strong demand and the ChampionX acquisition. However, Reservoir Performance and Well Construction declined, mainly due to the impact of the conflict.

SLB's Guidance

SLB expects Q2 visibility to remain limited due to ongoing geopolitical uncertainty in the Middle East.

Higher procurement and logistics costs are expected to continue impacting performance.

Under a base scenario, Middle East declines could be offset by mid- to high single-digit growth in other international markets.

North America revenue is expected to remain flat sequentially. Digital and Production Systems are expected to grow, while Reservoir Performance and Well Construction may decline. SLB expects free cash flow to build through the year, with the majority generated in the second half, alongside full-year capital investments of about $2.5 billion. The company plans to return over $4 billion to shareholders in 2026, including at least $2.4 billion in share buybacks.

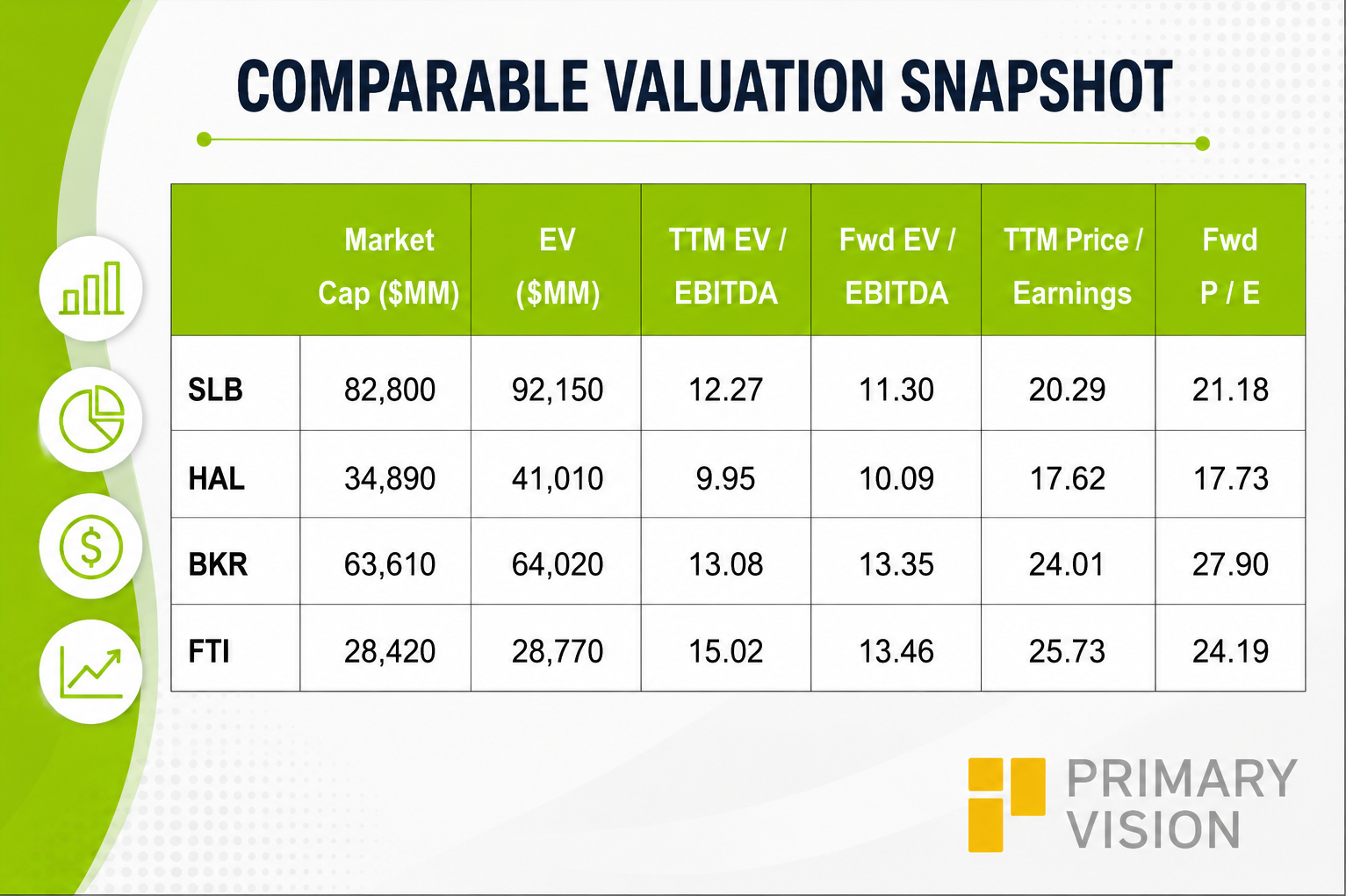

Relative Valuation

SLB is currently trading at an EV/EBITDA multiple of 12.3x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 1.3x. The current multiple falls short of its five-year average EV/EBITDA multiple of 11.7x.

SLB's forward EV/EBITDA multiple versus the adjusted current EV/EBITDA is expected to contract more steeply than its peers because the company's EBITDA is expected to increase more sharply than its peers in the next four quarters. This typically results in a higher EV/EBITDA multiple than its peers. The stock's EV/EBITDA multiple is similar to its peers' (HAL, BKR, and FTI) average. So, the stock appears slightly undervalued compared to its peers.

Final Commentary

SLB’s management holds the view that the macro outlook is improving, with higher oil prices and energy security driving stronger upstream investment. Near-term recovery will be uneven, but short-cycle activity should rebound first, followed by offshore growth. SLB is strengthening its positioning through digital, AI, and the ChampionX acquisition, with data centers emerging as a new growth avenue.

However, Middle East disruptions and higher costs continue to pressure near-term performance and visibility. Overall, I believe SLB remains well-positioned for gradual recovery, supported by strong cash flow generation and shareholder returns. The stock appears undervalued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform