Articles

- BLOG / Articles / View

- Articles

US Frac Activity Follows the Best Rock

By Avik on June 30, 2026 in Articles

Completion Activity Continues to Expand Despite Capital Discipline

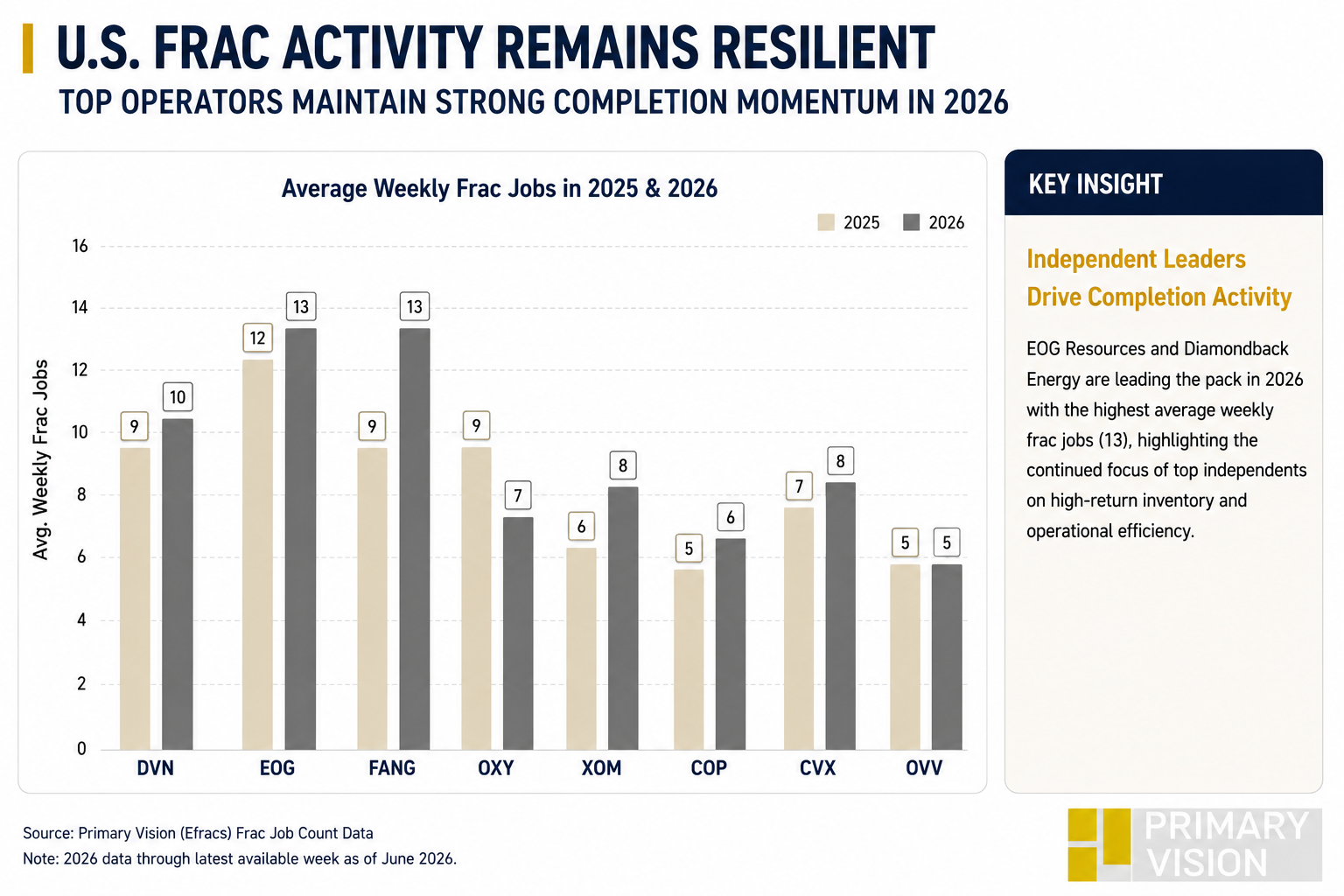

Primary Vision data show that the eight operators averaged 70 weekly frac jobs during 2026, compared with 62 jobs in 2025. EOG Resources and Diamondback Energy led the group with 13 average weekly frac jobs, while Devon averaged 10. ExxonMobil increased activity from 6 to 8 weekly jobs, Chevron from 7 to 8, and ConocoPhillips from 5 to 6. Occidental was the only major operator to reduce activity, declining from 9 to 7 weekly jobs, while Ovintiv maintained activity at 5 jobs per week.

The data indicate that operators continue protecting completion activity despite maintaining disciplined capital budgets. Rather than reducing development programs across the board, companies are selectively deploying crews within their most productive inventory. This strategy supports stable demand for pressure-pumping services while avoiding the production-growth model that characterized earlier shale cycles.

Production Growth Is Outpacing Activity Growth

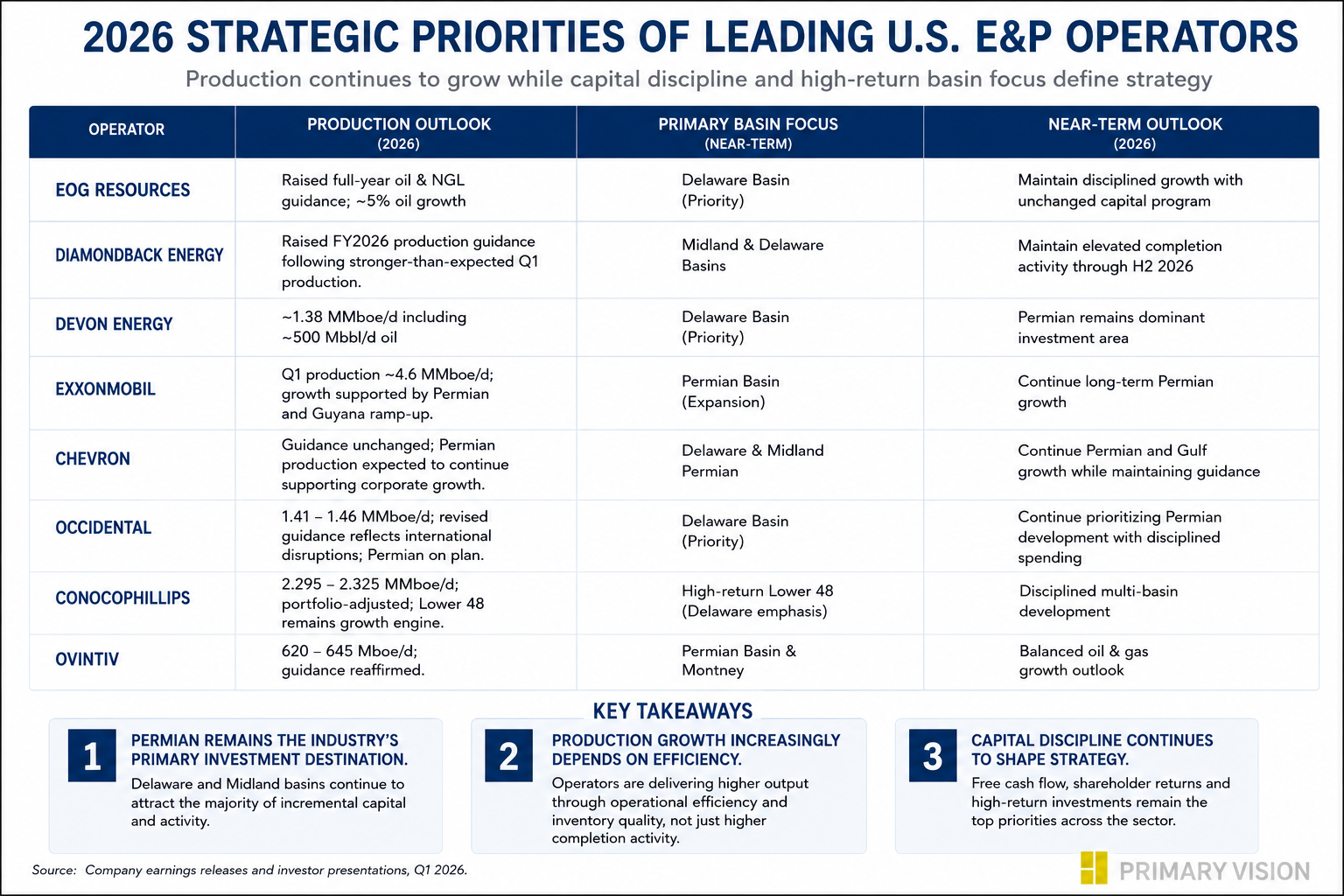

EOG continues targeting approximately 5% oil production growth while maintaining its capital program in the near term. Diamondback raised its 2026 production guidance following stronger-than-expected Q1 results, while Devon expects approximately 1.38 MMboe/d. ExxonMobil reported Q1 production of approximately 4.6 MMboe/d, supported by continued growth in the Permian and Guyana. ConocoPhillips continues guiding 2.295–

Operators are increasingly generating production growth from better wells rather than significantly higher frac activity, reinforcing the industry’s ongoing shift toward capital-efficient development.

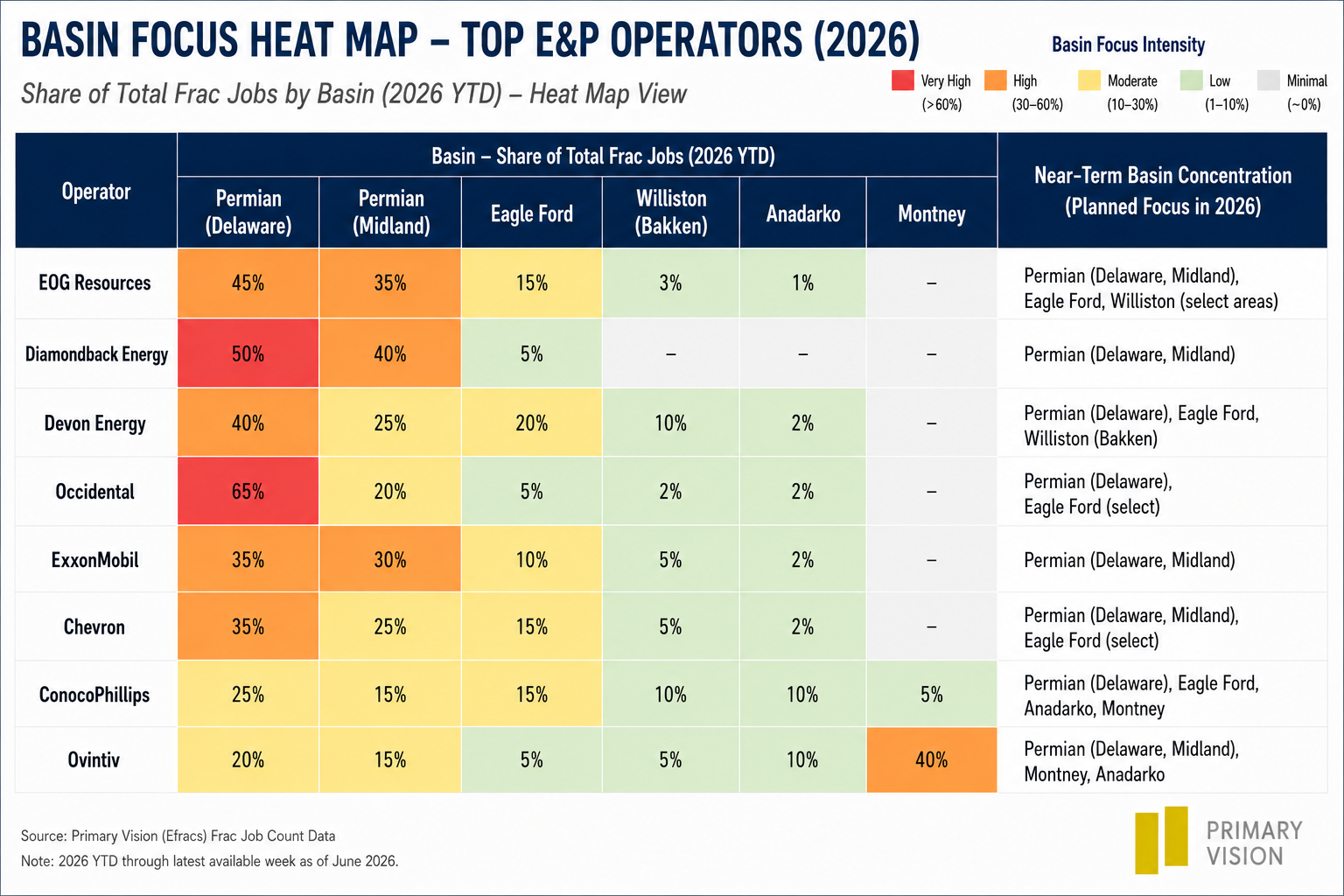

The Delaware Basin Continues to Attract Capital

Primary Vision’s basin analysis shows that the Delaware Basin remains the industry’s dominant investment destination. Diamondback allocates ~50% of its completion activity to the Delaware and another 40% to the Midland Basin. Occidental has the highest Delaware concentration at ~65%, while EOG allocates 45% to Delaware and 35% to the Midland. Devon also maintains a Delaware-focused portfolio, with ~40% of frac activity concentrated in the basin.

Outside the Permian, operators continue maintaining selective exposure to Eagle Ford, Williston, Anadarko, and Montney. ConocoPhillips and Ovintiv remain the most geographically diversified companies in the group, while Diamondback and Occidental continue concentrating investment within the Permian. The consistency between current frac activity and management guidance suggests that future investment will remain focused on premium inventory rather than broad geographic expansion.

Strategy Is Becoming More Concentrated

Production guidance and management commentary point to a common strategic direction. EOG continues to prioritize high-return liquids inventory, while Diamondback remains focused on manufacturing-scale Permian development. Devon emphasizes free cash flow generation, while Occidental and Chevron continue to highlight disciplined capital allocation. ConocoPhillips and Ovintiv continue directing incremental investment toward their highest-return unconventional assets.

The combination of resilient completion activity, concentrated basin investment and disciplined production growth suggests that operators are increasingly optimizing returns rather than maximizing output. Capital continues flowing toward the Delaware and Midland basins, while operational efficiency is becoming a larger contributor to production growth than incremental completion activity.

Outlook

Primary Vision’s data indicate that five of the eight operators increased completion activity, while most maintained or improved production guidance despite disciplined spending. The Permian Basin remains the industry’s primary investment destination, and management commentary suggests that this trend will continue through the remainder of 2026.

For oilfield service companies, the implication is constructive. Completion demand remains stable, but future opportunities are increasingly concentrated among operators with the deepest premium inventory and the strongest capital discipline. Rather than another broad shale expansion, the industry appears to be entering a phase where operational execution and inventory quality will drive activity levels.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform