Articles

Free Read: How is Brazil balancing the global oil markets?

By Osama on May 14, 2026 in Free Articles

When Iran declared the Strait of Hormuz closed on March 4, roughly 20 percent of the world's oil supply was removed from the market in a matter of days. The International Energy Agency called it the largest supply disruption in the history of the global oil market. Commercial traffic through the strait fell to about 5 percent of its pre-war average by April, and crude prices surged past $100 per barrel for the first time in four years. Asia, which received 84 percent of crude shipments through Hormuz in 2024, absorbed the worst of the blow. The question of who could replace those barrels — and how fast — became the central problem of global energy markets almost overnight. People thought of China, may be the U.S.? But who could've thought that it will be Brazil!

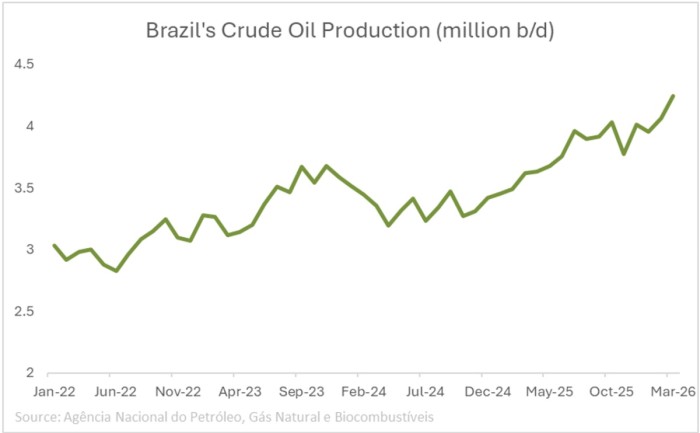

Domestic crude output in Brazil reached approximately 4.24 million barrels per day in March, up around 15 percent year-on-year, driven by new floating production vessels in the Santos Basin pre-salt fields. Petrobras, which accounts for roughly 88 percent of national output, pushed crude exports to a record 2.3 million barrels per day in March and held that level through April. The company redirected flows entirely toward Asia, cutting exports to the United States to zero by early May, with more than 60 percent of exports now going to China. Brazil's share of Chinese crude imports jumped from 10 percent in January to 18 percent in April.

The numbers from the Chinese side confirm the scale of the shift. Brazil's crude exports to China in the first quarter rose 122 percent year-on-year to 16 million metric tons, with values nearly doubling to $7.2 billion. The appeal is partly technical. Tupi and Buzios, the two key export grades, are around 28 to 30 degrees API with low sulphur content, making them a close substitute for the medium-sweet Gulf barrels that Asian refineries are configured to process. The production base keeps expanding: Petrobras brought its eighth FPSO at the Búzios field online on May 1, adding 180,000 barrels per day. The EIA forecasts Brazilian output averaging 4.0 million barrels per day for 2026.

The constraint is distance. A tanker from Brazil's Santos Basin to Chinese ports takes roughly 50 days, compared with five to seven days from the Persian Gulf. Freight costs remain central to the economics of the trade, and they place a ceiling on how much Gulf supply Brazil can realistically replace.

China, for its part, has not simply scrambled to buy everything available. It has pulled back. Chinese crude imports in April fell 20 percent year-on-year to 9.25 million barrels per day, the lowest since July 2022. State refiners were reselling crude for May loadings, cutting runs, and drawing down inventories rather than competing for expensive spot barrels. This is deliberate, enabled by preparation. The EIA estimates that China added an average of 1.1 million barrels per day to strategic inventories throughout 2025, building reserves to nearly 1.4 billion barrels by December. Analysts estimate Beijing has at least three months of import cover between commercial and strategic stocks. The government has since authorized state refiners to tap commercial reserves, giving it room to moderate import volumes without immediate economic pain.

China also leaned on Russian supply, which bypasses Hormuz entirely via overland pipelines and Pacific seaborne routes. As Anadolu Agency reported, imports of Russian ESPO crude rose significantly as Gulf maritime risks spiked. The effect of China's pullback on global markets has been tangible: physical crude premiums, which exceeded $30 per barrel above Brent in early April, collapsed to near-parity by mid-May.

The question now is what happens if the disruption persists. The April 8 ceasefire has not restored normal shipping. Iran's IRGC has rerouted traffic through its territorial waters and imposed inspections. Traffic through Hormuz in April was just 191 vessels, down from a pre-war average of 3,000 per month. The Dallas Fed has modeled the impact: a one-quarter disruption could reduce global GDP growth by 0.2 percentage points, rising to 1.3 points if it extends to three quarters.

Brazil can continue to supply incremental barrels, but it cannot replace the Gulf. Its entire export capacity is a fraction of the roughly 15 million barrels per day that normally transit Hormuz. China's strategic reserves provide a cushion, not a solution. If the strait remains functionally closed into the summer, the arithmetic tightens. The IEA's coordinated 400-million-barrel strategic reserve release buys time, but it is finite. Refiners across Asia are scheduling early maintenance and trimming runs. The longer this lasts, the less room there is to manage through inventory draws and demand destruction alone.

What is taking shape is not a temporary rerouting. It is a structural test of whether global oil markets can function with their most critical chokepoint offline. Brazil is filling part of the gap. China is managing the rest through reserves and restraint. Neither strategy is indefinitely sustainable.

Tags: