Articles

Free Read: How long can China balance the markets?

By Osama on May 28, 2026 in Free Articles

Three months into the worst disruption to global oil flows since the 1970s, and the market still can't decide what to feel. Brent crude traded at roughly $96 per barrel this morning, up modestly on the day after fresh US strikes on Iranian missile sites renewed fears of another escalation in the Strait of Hormuz. Prices have fallen more than 16% in May from their mid-month highs, driven by fitful optimism around a US-Iran memorandum of understanding that President Trump described as "largely negotiated" last week. Yet each step toward diplomacy has been followed by military action, and this week was no exception. Iran's IRGC claimed it struck a US airbase on Thursday morning, and the two sides continue to exchange fire even as negotiators work through competing draft proposals on Hormuz governance and nuclear enrichment. The result is a price that oscillates around $95–100 rather than collapsing or spiking, held in place by two opposing forces: the prospect of a deal and the reality that the Strait remains largely closed.

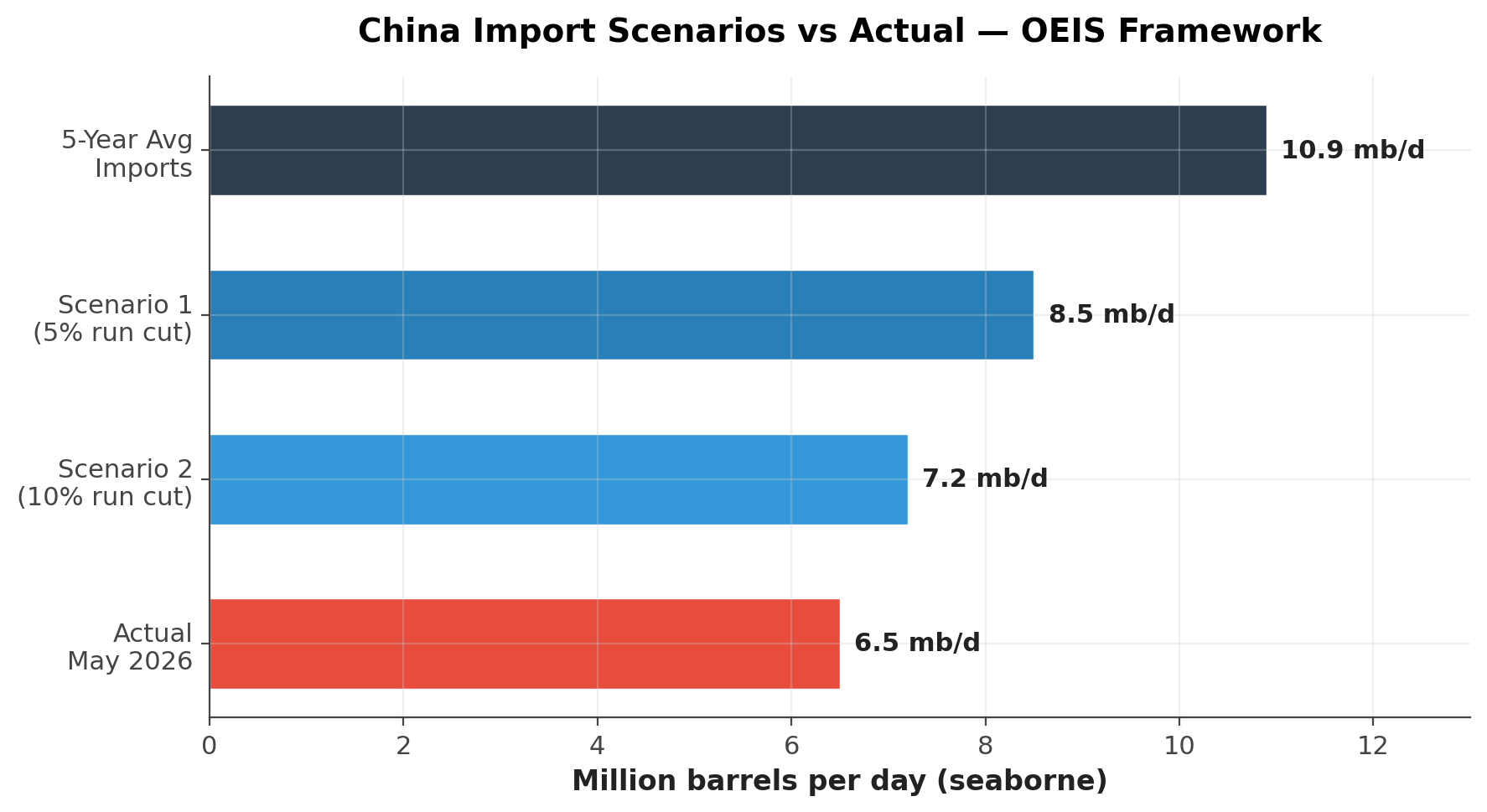

The standout development of recent weeks is China's dramatic reduction in crude imports. From a five-year average of around 11 million barrels per day (mb/d), seaborne imports fell to roughly 9.3 mb/d in April and are expected to drop further to around 6.5–6.8 mb/d in May, the lowest level in nearly a decade. Beijing has not panicked. Rather than chasing expensive spot barrels, China is drawing down the enormous commercial stockpiles it accumulated throughout 2025, when it added an estimated 1.1 mb/d to strategic inventories at prices near $60. Refinery runs have been cut by around 5%, crude throughput is down to roughly 13.5 mb/d, and Beijing has shifted refinery yields toward transport fuels at the expense of petrochemical feedstocks. A new Oxford Institute for Energy Studies paper published this week estimates that with 5–10% run cuts, China could sustain seaborne imports as low as 7.2–8.5 mb/d for a few months. However, as analyst Anton Likhodedov has pointed out, the scale of inventory withdrawal may be underestimated. His calculations suggest that 2025 stockpiling could have been as high as 1.1–1.4 mb/d using conservative baselines, and closer to 1.8–2 mb/d under certain scenarios, which would imply a larger import requirement once stocks are depleted. China's coal-to-chemicals sector, which the OEIS paper notes displaces around 1 mb/d of oil use, was running at high operating rates in Q1 and is unlikely to have provided more than a few hundred thousand barrels per day of additional substitution since the war began.

The question is how long China can sustain this posture. Mercuria's CEO Marco Dunand told the FT Commodities Summit in late April that the timeline for China's return as a major buyer was roughly three weeks, which would place it around mid-May. Onshore crude stocks have already begun trending lower, falling to around 1,232 million barrels as of late May from historic highs. Kpler's analysis frames this as a latent risk: the market's relative calm is partly a function of China's absence, and its return would inject demand back into a system already under structural stress.

Global inventories tell the broader story. The IEA's May Oil Market Report recorded draws of 129 million barrels in March and 117 million barrels in April, amounting to a combined 4 mb/d drawdown. On-land stocks in OECD countries plummeted by 146 million barrels in April alone. The US EIA expects global inventories to fall by an average of 8.5 mb/d in Q2 2026, a rate described as fundamentally unsustainable. Strategic petroleum reserves released by IEA member nations since March have bought time, but the buffers are finite. The EIA projects Brent averaging around $106 in May and June before easing to $89 in Q4 if Hormuz gradually reopens, though that assumption is far from certain.

The supply side has adapted with remarkable speed. Atlantic Basin crude exports have risen 3.5 mb/d since February, with the United States, Brazil, Canada, Kazakhstan, and Venezuela all pushing volumes higher. Russia's crude exports have also increased as repeated strikes on its refineries freed up domestic supply. Non-OPEC+ production growth forecasts for 2026 have been revised up by 600 kb/d since January. Yet even this cannot offset the full scale of the disruption. Gulf state production remains roughly 14.4 mb/d below pre-war levels, and global oil demand is expected to contract by 420 kb/d year-on-year in 2026, a figure that reflects both the price shock and weakening economic conditions.

The market is pricing in a resolution that has not yet arrived. Two non-Iranian supertankers crossed Hormuz on Tuesday for the first time in a week, and Iran's IRGC claimed 25 vessels transited in one 24-hour period, though CNN could not verify this. If a deal materialises and Hormuz traffic normalises over the summer, prices could fall substantially. If it does not, and China is forced back into the market while inventories continue to drain, the conditions exist for a sharp repricing. For now, the apparent stability in oil prices reflects not confidence but a series of temporary offsets, each of which has a limited shelf life.

Tags: