Articles

Free Read: Iran’s Oil Reset: What Comes Back, How Fast, and Where the Barrels Go

By Osama on June 16, 2026 in Free Articles

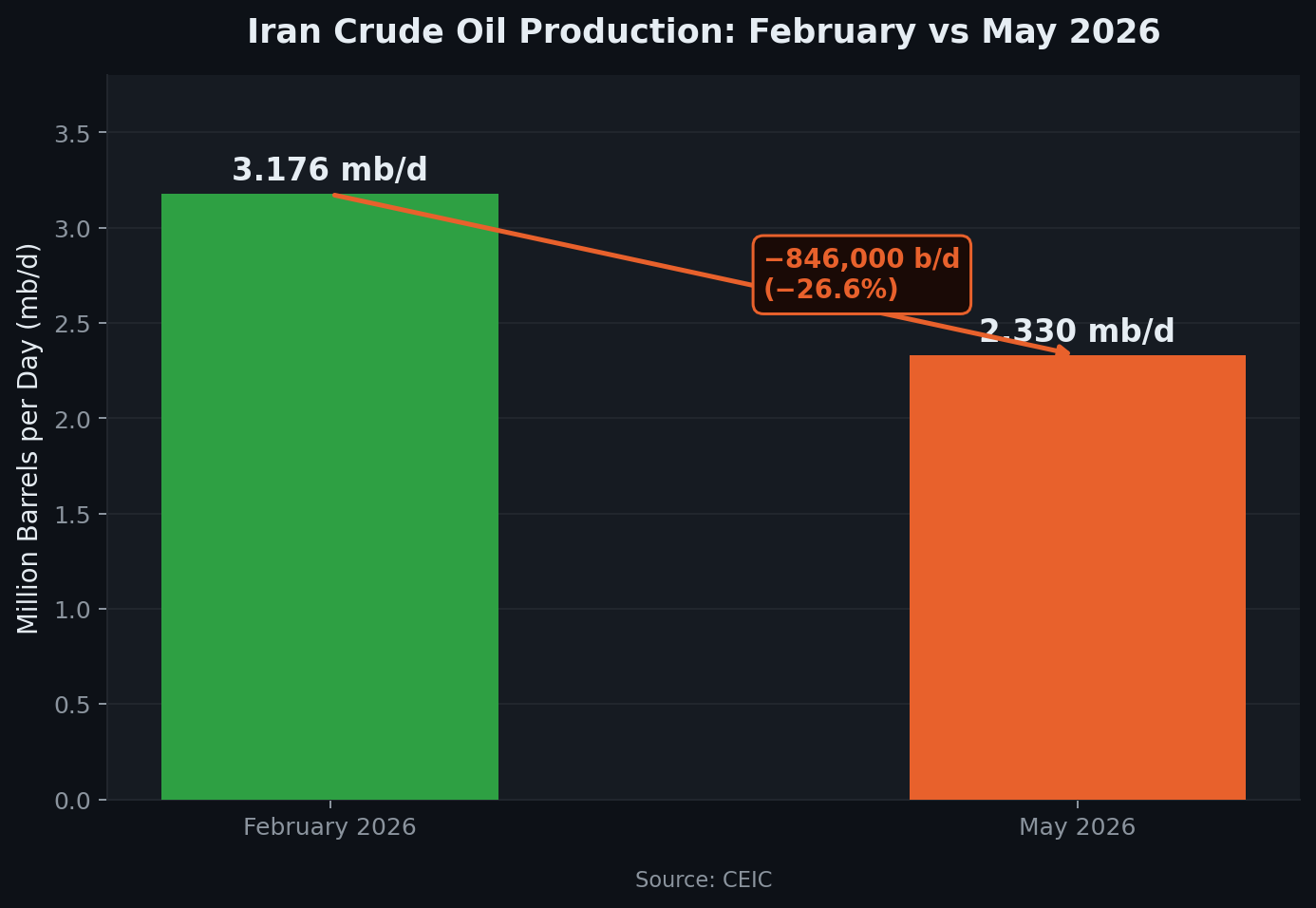

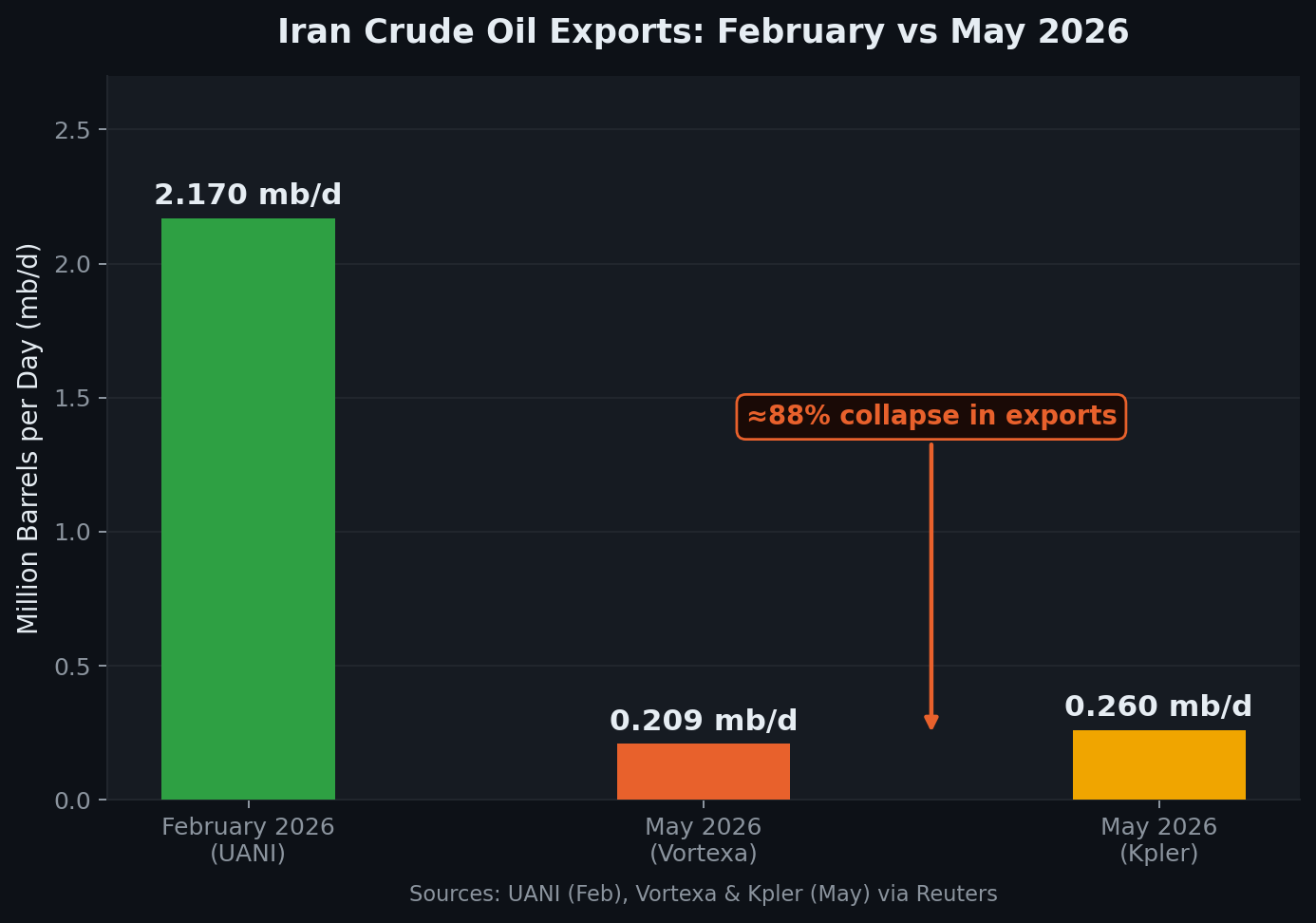

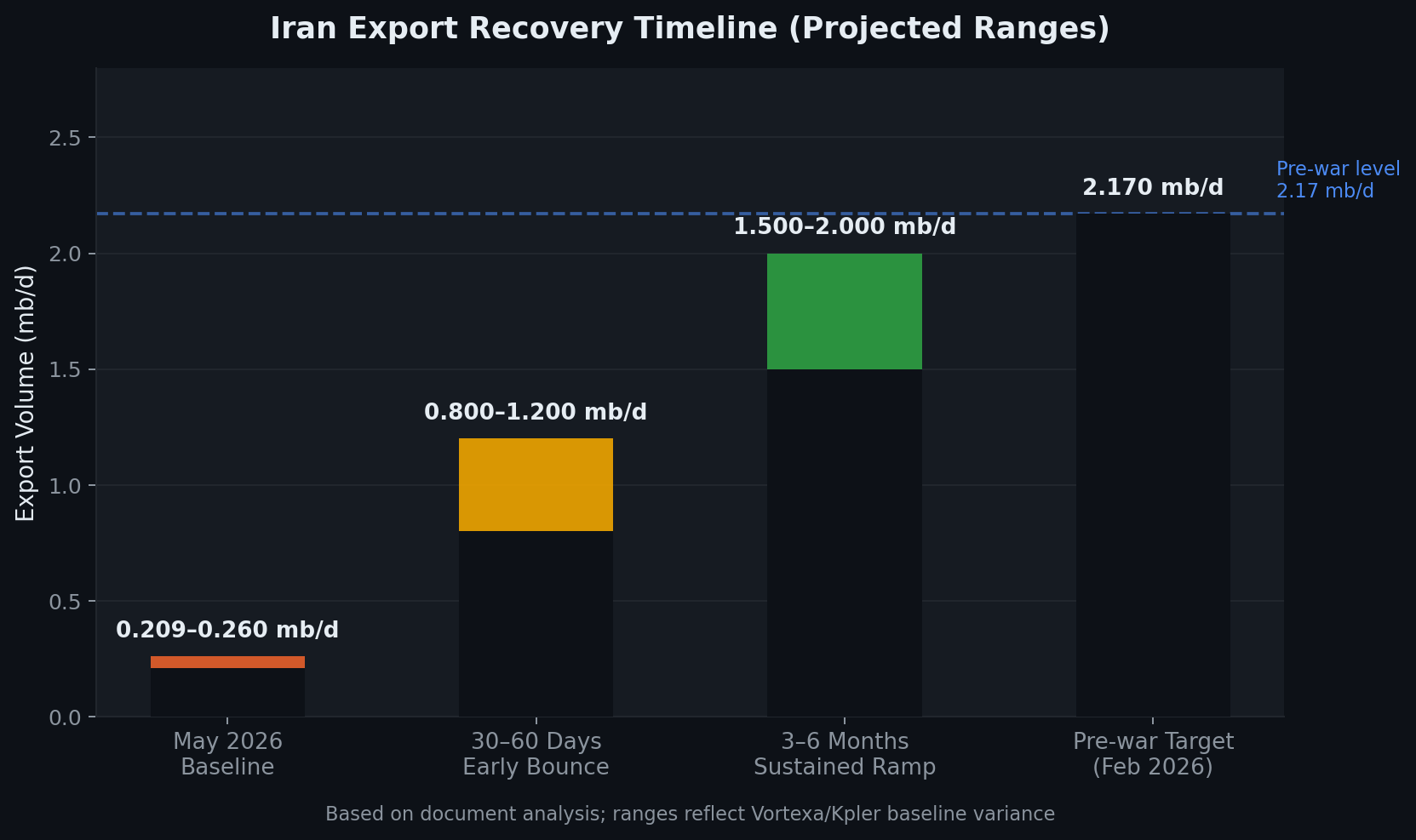

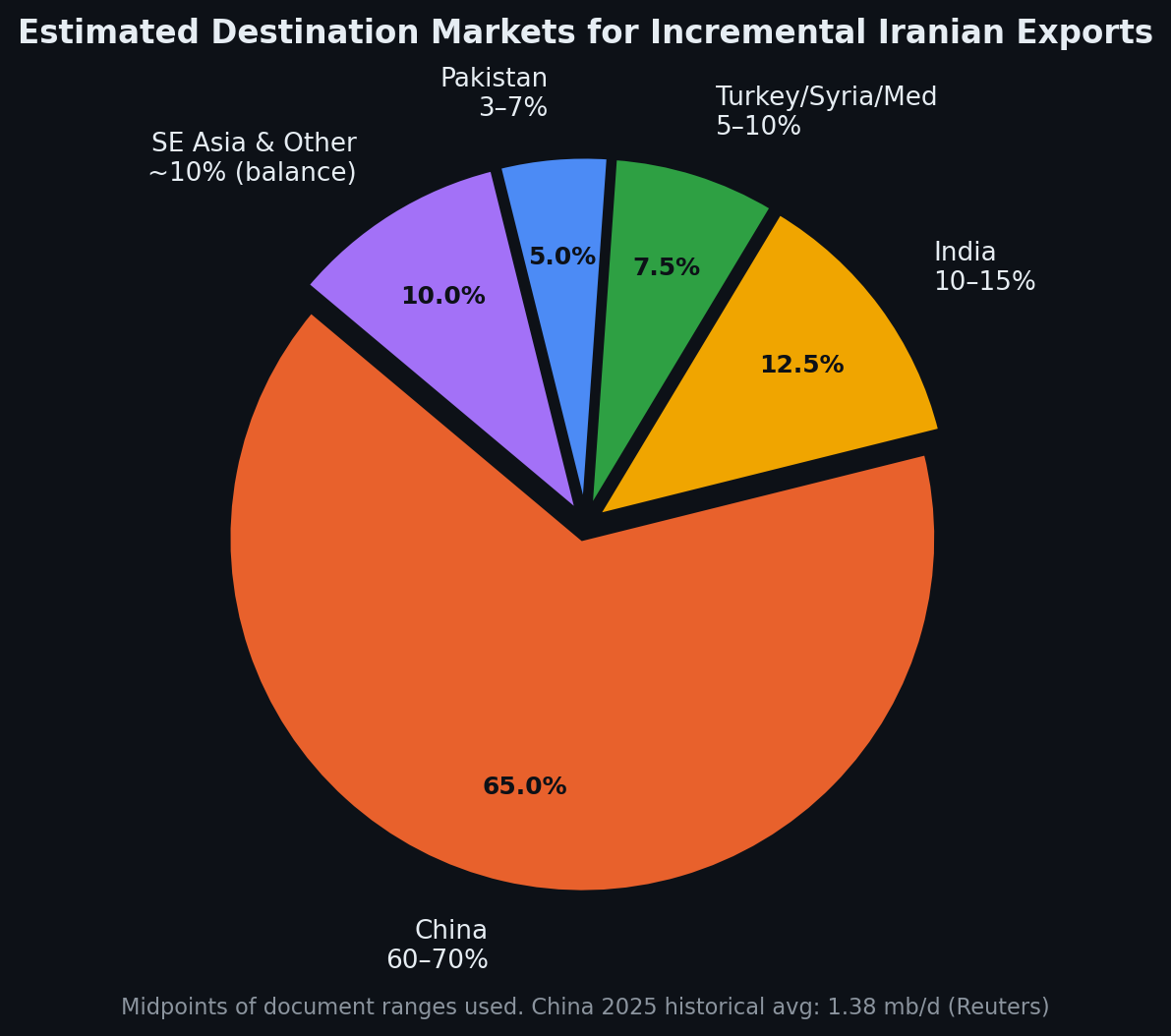

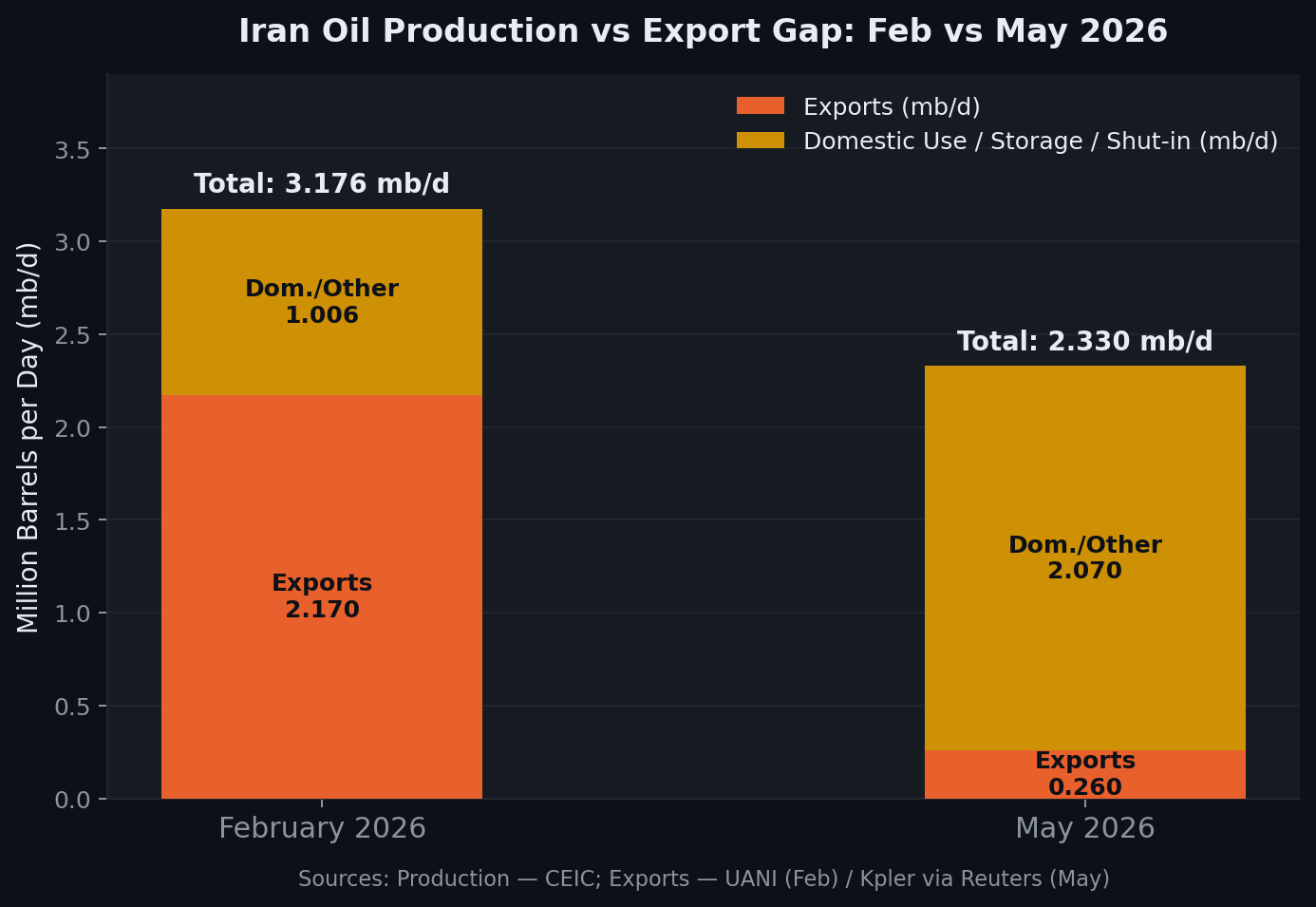

Production fell 26.6%: 3.176 mb/d in February 2026 to 2.330 mb/d in May, a loss of 846,000 b/d. Exports fell about 88%: around 2.17 mb/d in February to 209,000-260,000 b/d in May. Ramp-up is uneven: output can recover faster than sustained exports; 1-3 months for partial production recovery, 3-6 months for exports above 1.5 mb/d. Likely markets: China 60-70%, India 10-15%, Turkey/Syria/Mediterranean 5-10%, Pakistan 3-7%, with the balance in Southeast Asia or blended routes. |

The U.S. decision to allow Iran to sell oil again changes the market conversation, but it does not mean Iranian crude immediately returns to pre-war levels. Iran has to restore production, clear export bottlenecks, bring buyers back, secure ships and insurance, and prove that its main export system can work reliably.

Start with the production baseline. Iran was producing 3.176 million barrels per day in February 2026, according to CEIC. By May, output had fallen to 2.330 mb/d. That is a fall of 846,000 b/d, or 26.6%. The drop is large, but it does not suggest the entire upstream system was destroyed. It suggests a combination of facility damage, export disruption, storage pressure and forced shut-ins. Exports tell the sharper story. In February 2026, UANI tracked 60.7 million barrels of Iranian physical oil exports, equal to about 2.17 mb/d. By May, Reuters reported exports at only 209,000 b/d on Vortexa numbers and 260,000 b/d on Kpler numbers. Using 260,000 b/d, exports fell by roughly 1.91 mb/d, or about 88%. That is the real shock: Iran did not just lose production; it lost access to the water.

The first barrels can come back faster than the full system. If oil already in storage or on tankers can move, exports can bounce quickly in the first 30 to 60 days. A realistic early range is 800,000 b/d to 1.2 mb/d. But holding exports above 1.5 mb/d is harder. That likely takes three to six months because buyers need payment channels, insurers need clarity, tankers need safe routing, and Iran needs its export terminals operating smoothly.

Kharg Island is the main facility to watch. Kharg is defined as accounting for nearly all of Iran’s average crude export volume before the war. Axios later reported that U.S. strikes had targeted Kharg and noted that the island handles about 90% of Iran’s crude exports. That makes it the single most important choke point. If Kharg’s berths, loading arms, storage tanks, power systems and pipeline links are functional, Iran can ramp exports faster. If those systems need heavy repair, the recovery shifts from weeks to months. The damage assessment should be split into three buckets. First, export infrastructure: Kharg Island was the highest-value target because it determines how much crude can physically leave Iran. Second, field and pipeline infrastructure: if wells were shut in rather than damaged, output can return quickly; if pipelines, gathering systems or power supply were hit, production recovery slows. Third, gas and refining infrastructure: South Pars, Asaluyeh and refinery-linked assets matter because gas supports domestic power, petrochemicals, refinery runs and oilfield operations. Even if crude wells are ready, weak gas or power supply can delay the broader energy recovery.

The dark fleet will not disappear overnight. Iran has relied for years on older tankers, opaque ownership, ship-to-ship transfers, AIS gaps, reflagging and blending to move crude, mainly into China. If sanctions relief becomes real and durable, legitimate shipping should gradually replace part of that system. But during the transition, Iran may still use dark-fleet logistics to clear stranded barrels and keep trade moving while normal banking and insurance channels reopen.

China remains the first market. The country bought more than 80% of Iran’s shipped oil in 2025 and averaged 1.38 mb/d of Iranian crude. That history matters. Chinese refiners know the grades, the discounts and the trading routes. If Iranian oil returns at scale, China could take 60% to 70% of incremental flows. India is the second market to watch. If U.S. relief is clear enough for banks, insurers and refiners, India could take 10% to 15% of returning Iranian barrels. Southeast Asia may take part of the rest through direct or blended routes. Pakistan should be included, but the near-term volume is likely smaller. A practical range is 3% to 7% of incremental Iranian exports. Pakistan has strong energy-import needs and geographic logic, but it also needs payment channels, refinery compatibility, government clearance and confidence that U.S. permission will last. Arab News has highlighted Pakistan’s exposure to imported energy and Hormuz-linked flows, while World Bank WITS data shows its fuel imports are still anchored in suppliers such as the UAE, Saudi Arabia, Qatar, Kuwait and Singapore.

The clean assessment is this: Iran can recover part of production within one to three months, possibly moving back toward 2.8 to 2.9 mb/d if shut-ins are reversible. Returning to the February level of 3.176 mb/d may take three to six months if export and power systems are mostly intact. Exports can jump faster from storage, but sustained exports above 1.5 mb/d depend on Kharg, tankers, insurance, banking and buyer confidence all moving at the same time.

The market has already reacted to the announcement. Oil fell sharply after hopes grew that Iranian exports and Hormuz flows could resume/have resumed. But the physical market will move more slowly. Policy can reopen the door. Terminals, tankers, banks and buyers decide how much oil actually comes through it.

Tags: