Articles

Free Read: Is the Oil Price Forecast Dead?

By Osama on June 4, 2026 in Free Articles

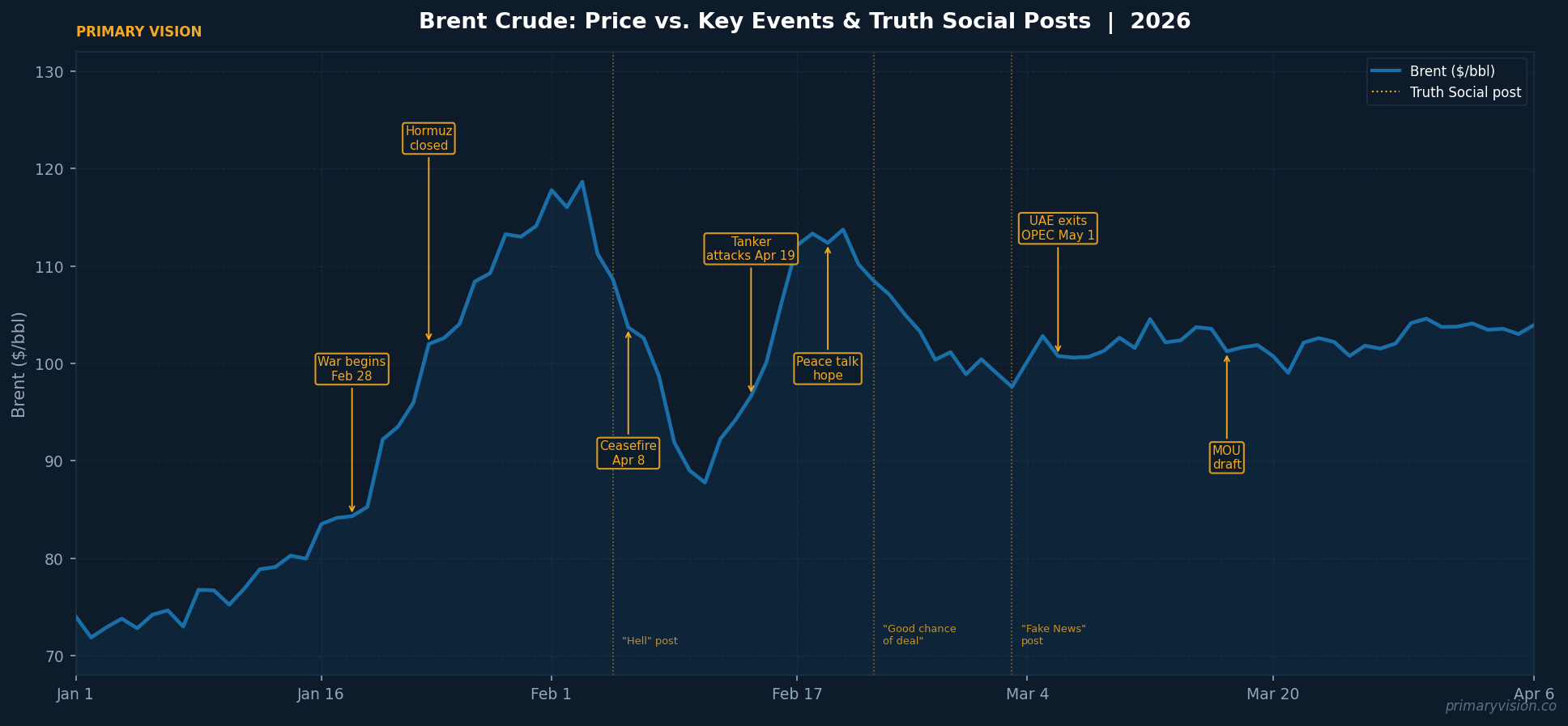

At the start of 2026, the consensus view across Wall Street and the major commodity desks was remarkably tidy: a supply glut was coming, producer discipline was fraying, and Brent would spend most of the year somewhere between $60 and $75 a barrel. The models said so. The spreadsheets agreed. The research notes went out. Then a war started, a strait closed, and a president began posting.

We are now in a world where a single Truth Social post at 7am on a Sunday — "Open the ****' Strait, you crazy b****, or you'll be living in Hell - JUST WATCH!" — moves Brent crude 1.5% before European markets even open. Where commodity analysts have dedicated screens monitoring the presidential feed in real time. Where oil and gas volatility surged roughly 300% in the conflict's opening weeks — not because supply-demand balances shifted overnight, but because the interpretive noise around a single human being became the dominant market signal.

The forecasters deserve sympathy here, not mockery. They were handed conditions that no historical model was ever trained on. The Strait of Hormuz has never been closed for this long. 10 to 11 million barrels per day have been effectively shut in for months — a supply shock that has been called the largest in the history of the global market. Add a major OPEC exit that nobody had modelled, a ceasefire brokered through Pakistan and Oman with no precedent in energy diplomacy, and a U.S. president whose stated preferred oil price — around $40 to $50 a barrel per an analysis of over 1,000 Truth Social posts — sits wildly below what the market is printing. These are not conditions that reward a tidy regression.

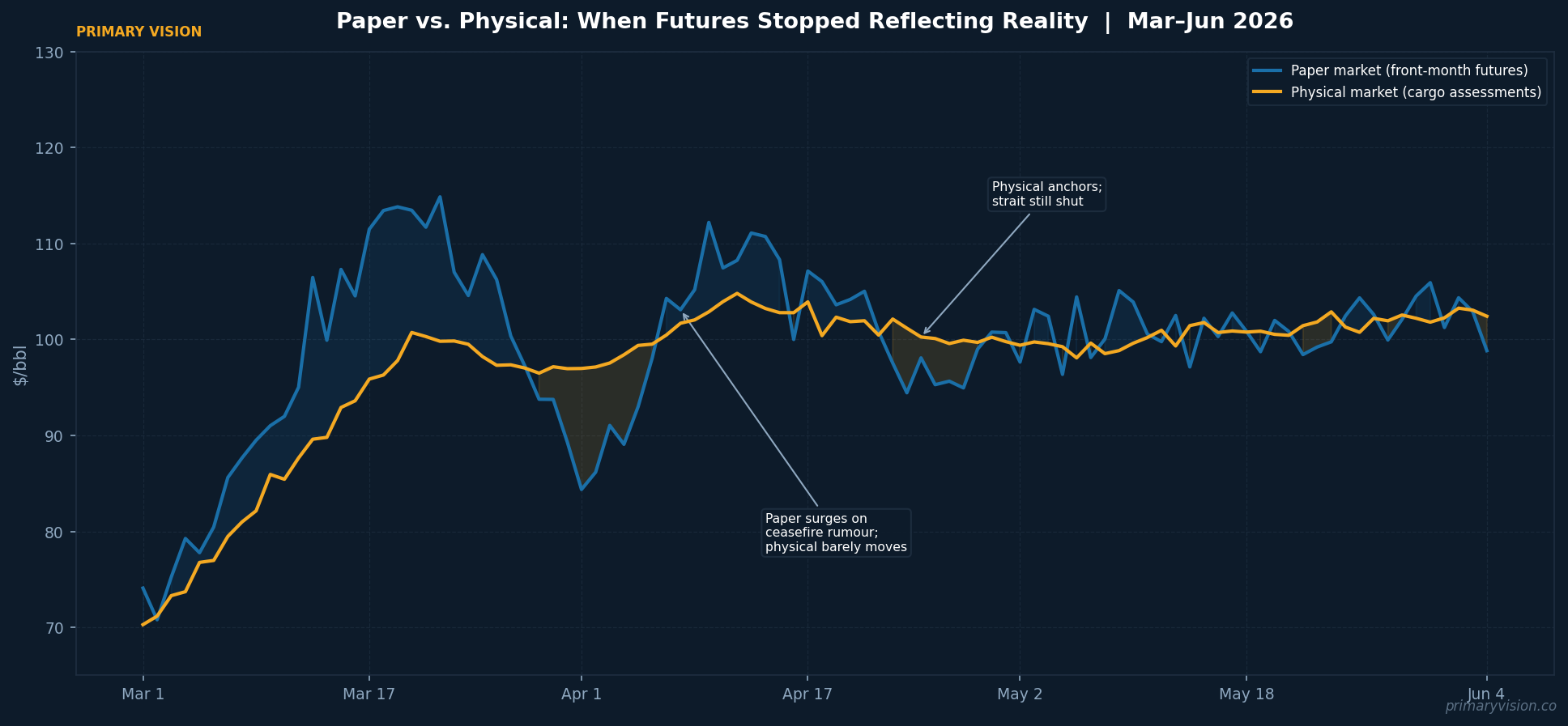

But sympathy has its limits. What the last three months have exposed is something more fundamental than a bad quarter for forecasters. The architecture of oil price prediction was always built on a marriage between the physical and paper markets — the assumption being that the two would, over time, converge. Physical barrels set the floor; futures reflected the forward view of supply and demand; and the spread between prompt and deferred contracts — the structure of the curve — told you whether the market was tight or loose. That marriage is under serious strain right now, and almost nobody is talking about it.

The paper market is being priced on geopolitical optionality. Every ceasefire rumour, every presidential post, every back-channel counter-proposal sends the front-month contract lurching. But the physical market — actual cargoes, actual refiners, actual crude grades — is telling a slower, grimmer story. Refiners in Asia are not buying and selling barrels based on what gets posted at 7am Washington time. They are managing month-long procurement cycles, absorbing the reality that certain crude grades simply cannot move through the world's most important chokepoint, and repricing their feedstock mix accordingly. The paper price swings 3% on a rumour. The physical differential barely flinches, because the physical problem hasn't changed.

This divergence matters enormously for how you read the market. When the paper market rallies on peace talk optimism, it is pricing in a future state of the world — Hormuz open, barrels flowing, inventories rebuilding. When the physical market stays anchored, it is telling you that traders moving real crude don't yet believe that future is imminent. Even in the most optimistic reopening scenario, the market is estimated to lose another billion barrels of crude production and 800 million barrels from inventories between now and November. The physical reality has a lag that no futures contract can fully capture.

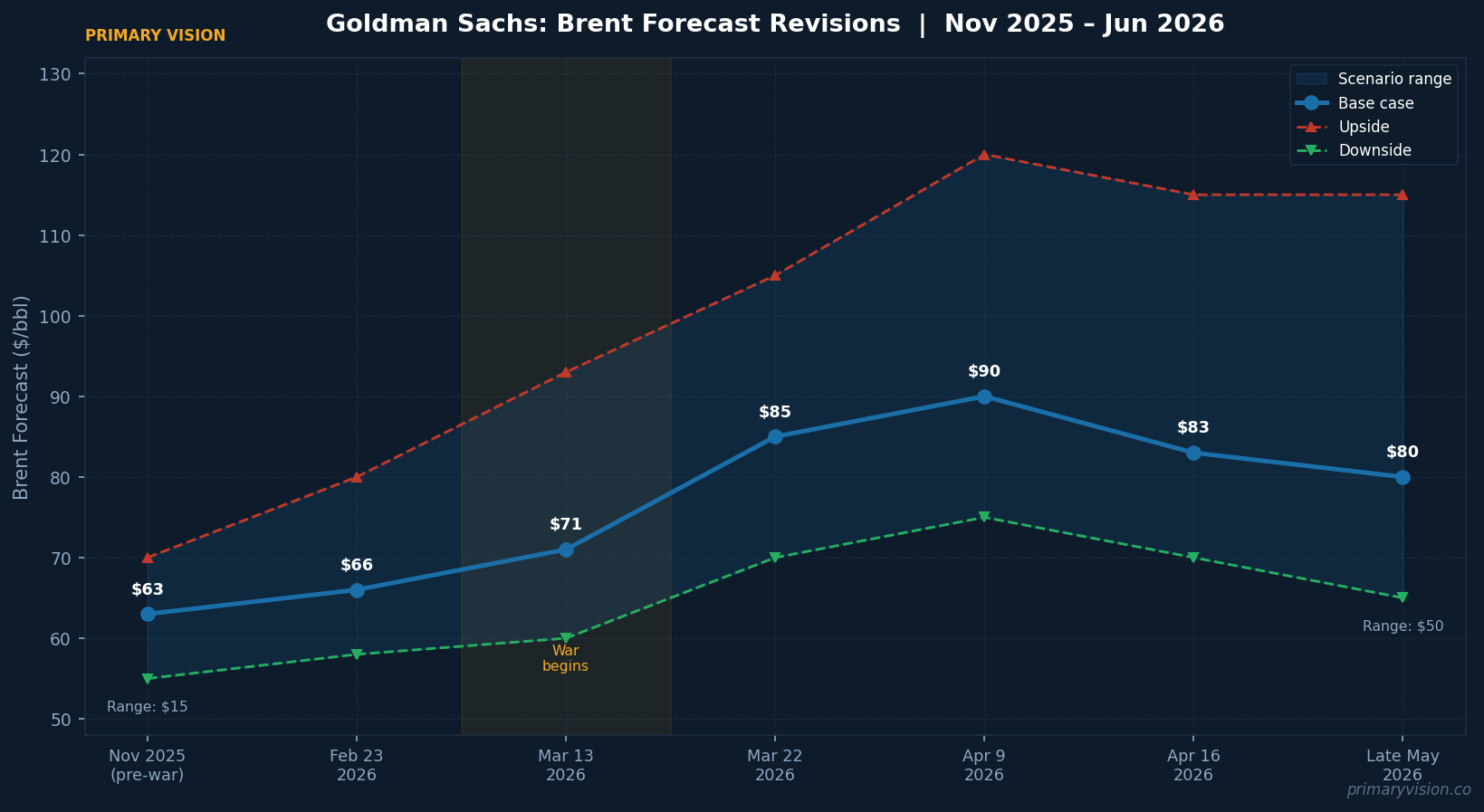

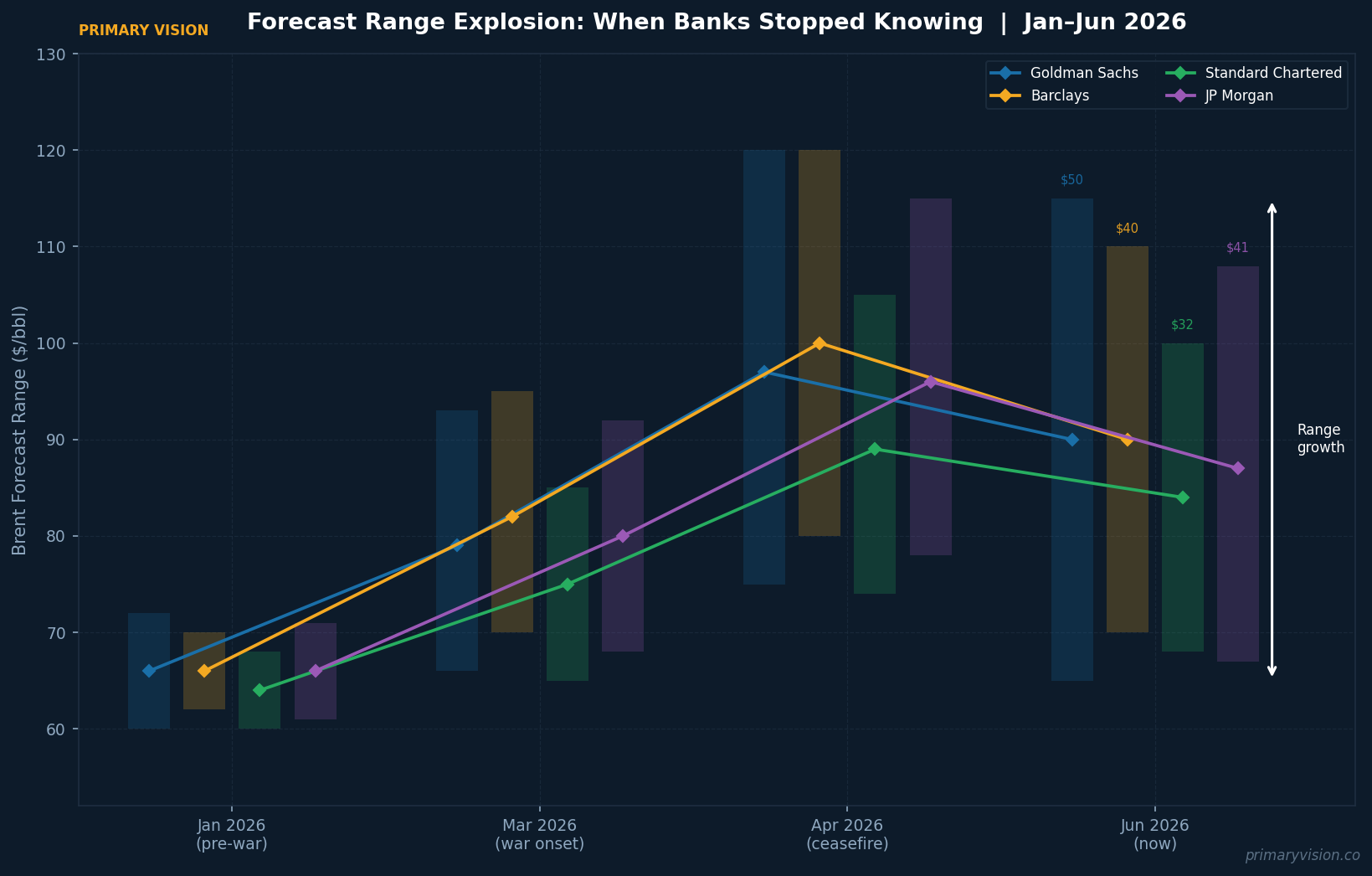

Forecasts have now been revised multiple times across the street, each revision more hedged than the last, each one attaching wider and wider scenario bands. The current range across major desks runs from $80 Brent in a smooth resolution to $120 in a renewed escalation — a $40 spread that is less a forecast than an honest admission that the distribution of outcomes has fattened beyond the point where a point estimate is meaningful. Others have followed suit. The widening scenario bands are effectively the market saying: the paper price can go anywhere depending on the next post, but nobody can tell you which post comes next.

What the industry actually needs right now is not a better price forecast. It is a clearer framework for reading the gap between paper and physical — understanding when the futures curve is pricing real barrels and when it is pricing geopolitical mood. Presidential posts drove sharp rallies multiple times this spring, but crude oil was notably less responsive each time than equities — a sign that physical market participants, burned enough times by optimistic signals that preceded nothing, began discounting the noise faster than others did. That divergence in how paper and physical traders respond to the same information is itself the most honest signal available right now.

The physical reality of oil still matters enormously. Barrels are still scarce, refineries are still scrambling, and infrastructure damage across the Gulf means even a reopening won't flip a switch. But the price on your screen at any given moment in 2026 is only partially a reflection of that physical world. The rest is a bet on what one man decides to post before breakfast — and no model built for the old market was designed to price that.

Tags: