Articles

Free Read: What's Keeping Oil Prices Low?

By Osama on July 1, 2026 in Free Articles

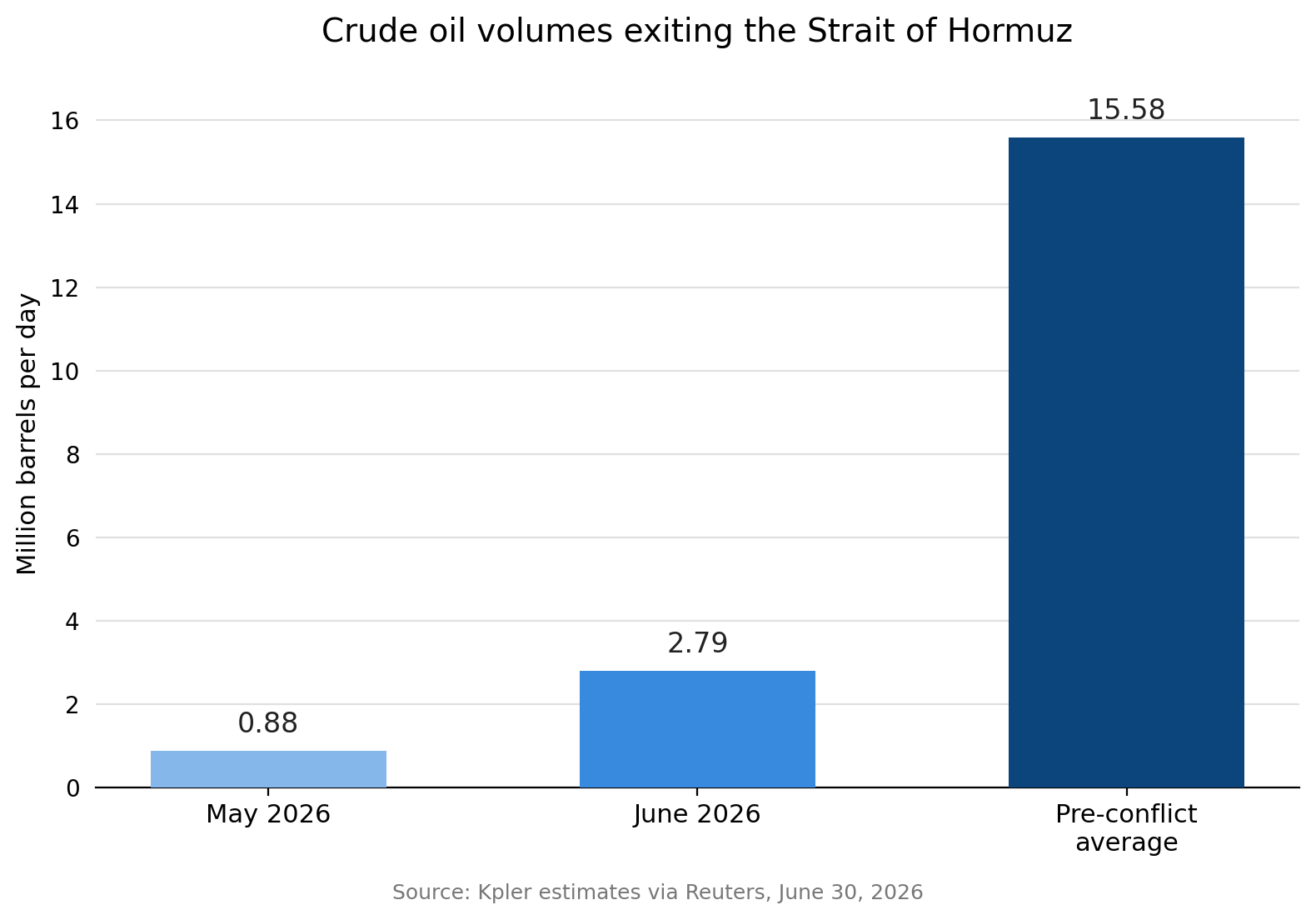

The question worth asking in the room is not whether the Strait of Hormuz risk has disappeared. It clearly has not. Tanker movements are still far below normal, insurers and shipowners are still treating the waterway as a live security risk, and Asia is still not receiving crude the way it did before the war. Kpler estimates that crude volumes exiting Hormuz rose to 2.79 million bpd in June from 881,000 bpd in May, but that is still far below the pre-conflict average of 15.58 million bpd. The better question, then, is this: why is the market not paying more for that risk? I think the market is decidedly looking towards the medium term future and determining prices accordingly. The market's thought process is that may be the finding the next barrel moving forward is going to be far easier than the previous 100 days. I break down the reason for not seeing higher oil prices below.

The first reason is supply restoration. The speed of the Gulf recovery has changed the psychology of the market. Kuwait is the clearest example. After disruption earlier in the conflict, Kuwait Petroleum Corp was already offering crude for July delivery after lifting force majeure and announcing plans to ramp up output. Earlier, KPC had said Kuwait could recover 70% of output within six to eight weeks of Hormuz reopening. That does not mean Kuwait is fully normal. It means the market has stopped pricing Kuwait as a long-duration outage. The UAE has been even more important because it proved something bigger: Hormuz disruption does not automatically equal total Gulf immobilisation. UAE crude and condensate exports averaged around 3.7 million bpd in June, a record level, while Abu Dhabi crude loadings reached about 4 million bpd. This is why the price action looks counterintuitive. The tanker count can still be ugly, but the market is watching barrels, not only ships.

The second reason is sentiment. Oil prices trade the balance, but they also trade the expected direction of the balance. Brent is trading near $72 a barrel and WTI to roughly $69.12. Positioning data backs up the mood: CFTC figures show managed money's short position in crude climbed to around 97,400 contracts in the week to June 9, up close to 12% from the prior week — traders adding bearish bets even as the physical disruption was still unwinding. That combination is telling. A market convinced escalation was the base case would not be piling into shorts; it would be paying up for protection against further supply loss. Instead, the positioning and the price both point the same way: traders betting the worst of the disruption is behind them. The market does not need normality to turn bearish. It only needs evidence that the next month will look better than the last one. Once traders believe shipping routes will keep reopening, stranded cargoes will move, and Gulf supply will keep returning, the fear premium deflates even while present conditions remain fragile.

The third reason is China. The market has been given an accidental shock absorber by the world’s largest crude importer. China’s seaborne crude arrivals were forecast at just 5.80 million bpd in June, down from 6.80 million bpd in May. That is roughly half the 11.39 million bpd average seen in the three months before the conflict. So the number being discussed near 5–6 million bpd is not total Chinese crude demand. It is seaborne arrivals — and that distinction matters. China has not stopped needing oil. It has postponed buying. Earlier figures showed May imports at 7.79 million bpd, down from an 11.85 million bpd first-quarter average. But refiners did not absorb the shock only by emptying tanks. They also cut refinery runs, with throughput falling by around 2.29 million bpd versus the first quarter. In plain terms, China absorbed the shock by doing less, not simply by drawing more.

That is why oil has struggled to rally. If the largest crude buyer is absent at the same time Gulf supply is coming back faster than expected, the market will not trade Hormuz disruption in isolation. It will trade the net result: more supply confidence, less immediate Chinese buying, and a diplomatic path that keeps de-escalation alive.

But this is also where the next risk sits. China cannot keep imports this low indefinitely without either reducing activity further, drawing stocks harder, or returning to the market. Recent analysis argues that China may have learned to live with less fuel for a period, but that does not remove the need to replenish. If prices stabilise and refiners see better margins, Chinese buying can return. And because cargoes bought now shape August and September balances, the market’s calm today can become tighter later.

So the bearishness in oil is logical, but not necessarily permanent. It rests on three assumptions: Gulf supply keeps returning faster than feared, diplomacy keeps de-escalation alive, and China does not rush back into the market all at once. If those assumptions hold, crude can remain heavy even with Hormuz traffic below normal. But if Chinese buying recovers before tanker confidence and Gulf flows fully normalise, the market will have to reprice again.

This is why the current price action should not be read as proof that the Hormuz risk is over. It should be read as a repricing of sequence. Supply is returning first, sentiment has turned second, and Chinese demand has not yet returned in force. For now, that order is bearish. If the order changes, so will the price. Oil is not rising because the market is no longer trading the headline of disruption. It is trading the path out of it.

Tags: