Market Sentiment Tracker: Are we seeing demand destruction?

By

Osama

on June 9, 2026

in

Market Sentiment

Demand destruction is not a headline; it is a sequence. New orders roll over first, hiring softens next, credit availability tightens, and only then does the consumer stop spending because cash flow, confidence, or financing has broken. This week’s data does not show that sequence everywhere. It shows a U.S. economy still absorbing pressure, a European economy where demand damage is becoming easier to see, and a China signal that is encouraging but too narrow to call a full recovery.

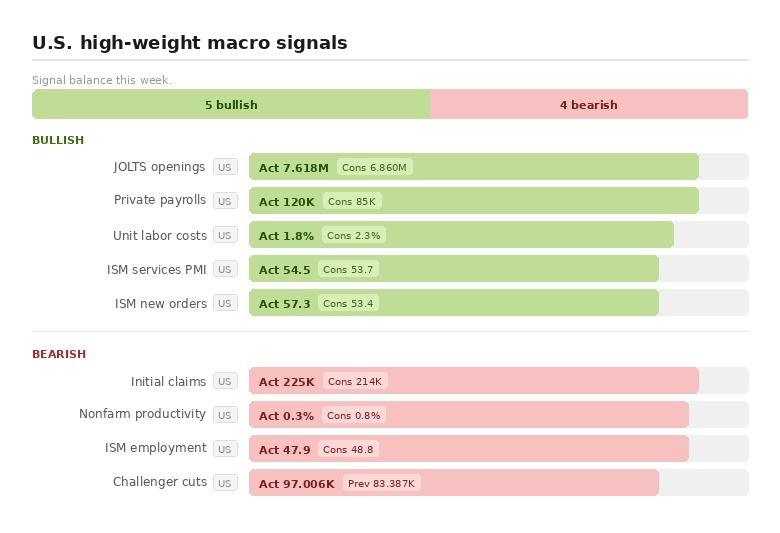

In the U.S., the most important point is that final demand has not cracked. The ISM services headline at 54.5 matters, but the cleaner demand tell is new orders at 57.3 versus 53.4 expected. That is not what demand destruction looks like. Factory orders at 4.8% also argue that businesses are still placing orders, not freezing activity. Labor is sending the same mixed message. JOLTS openings at 7.618 million and private payrolls at 120,000 came in better than expected, so the income engine is still running.

The stress is not in demand yet; it is in the labor edge. Initial claims at 225,000, Challenger job cuts at 97,006, and ISM employment at 47.9 are the small tells to watch. This is how an economy moves from “slower” to “dangerous”: firms stop adding labor before consumers stop spending. For now, strong new orders are still offsetting softer employment. If new orders slips toward 50 while claims keep rising, the U.S. demand story changes quickly. The second test is wages: average hourly earnings at 0.3% were steady, not collapsing, which keeps the consumer from losing the paycheck support that normally breaks late.

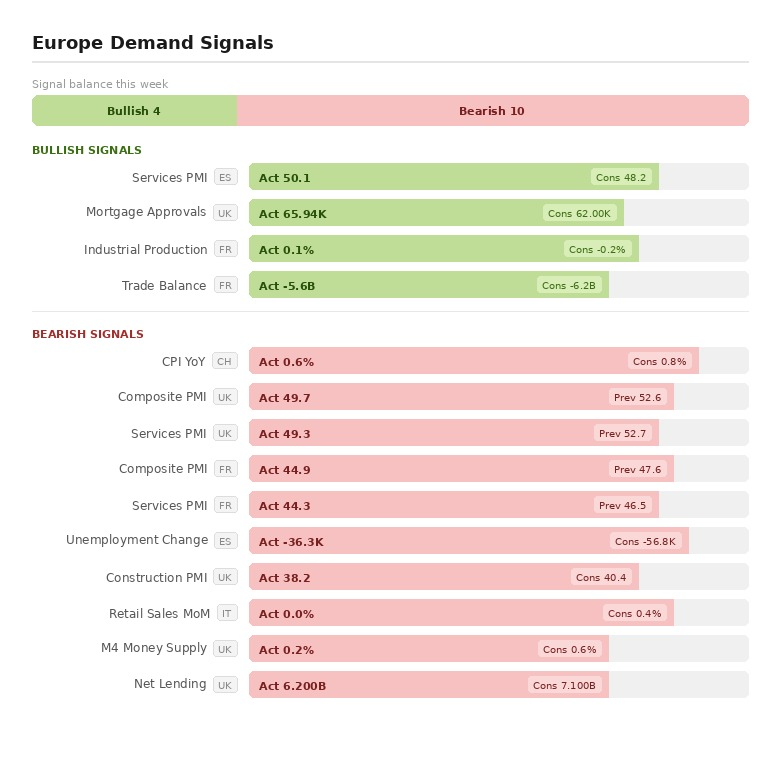

Europe is different. Here, the problem is not one bad print; it is the shape of the data. The U.K. composite PMI slipped to 49.7 from 52.6, while U.K. services fell to 49.3 from 52.7. France is already deeper in contraction, with services at 44.3 and composite at 44.9. Germany’s services PMI at 48.1 is still below 50, even after improving from the prior month. That matters because services are where domestic demand, wages, and discretionary spending usually show up.

Credit is the second warning. U.K. M4 money supply missed badly, net lending missed, and Italy’s retail sales were flat against a 0.4% consensus. Those are not dramatic numbers individually, but together they describe a demand environment losing oxygen. Spain and parts of France offered offsets, including Spanish services back above 50 and French trade less weak than expected. But offsets are not leadership. Europe is the region where demand destruction is no longer theoretical; it is visible in PMIs, credit, and retail softness.

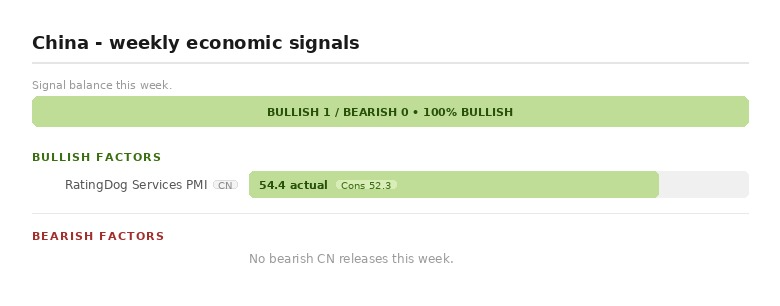

China gives the opposite signal, but with less confirmation. The RatingDog services PMI at 54.4 versus 52.3 expected is a clean positive. It says services demand is expanding, and expanding faster than expected. That argues against current demand destruction. The issue is breadth. One strong services print is not enough unless it pulls through into retail sales, imports, employment, and property-linked activity.

So the answer is no, not broad global demand destruction. The U.S. is slowing at the labor margin but still demand-positive. China’s services pulse is healthy but under-confirmed. Europe is where the damage is most advanced. The tiny factors to watch now are simple: new orders, employment sub-indexes, claims, lending, retail sales, and imports. When those move down together, demand destruction is here. Right now, they are split.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform