Market Sentiment Tracker: Why this week is so important?

By

Osama

on April 28, 2026

in

Market Sentiment

Let me be direct with you about what this week's data is actually showing, because the surface readings are misleading if you look at them in isolation.

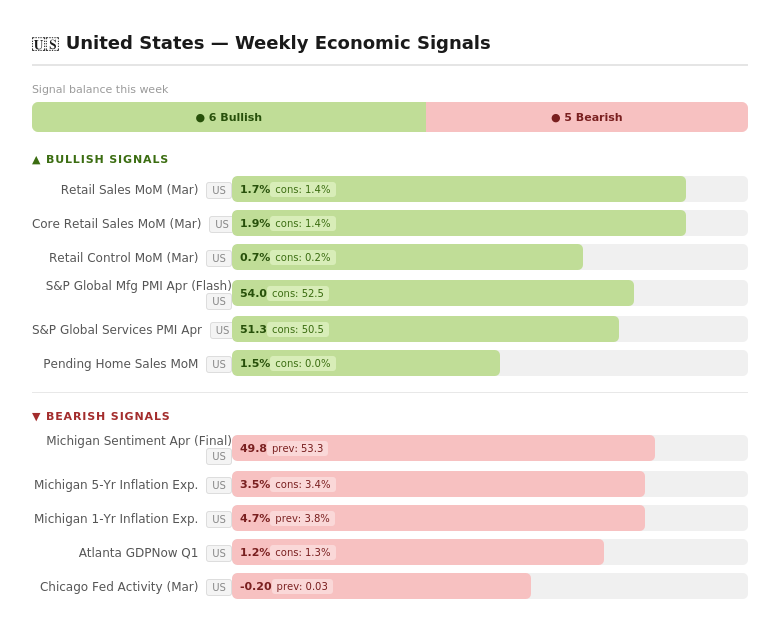

The United States spent in March. Consumers showed up. Retail sales beat, manufacturing PMI beat, services held. But by April, those same consumers were telling the Michigan survey that they expect prices to rise 4.7% over the next year, up from 3.8% the month before. That gap between what people did in March and what they believe is coming in the next twelve months is the most important signal in this entire dataset. Behaviour lags expectations. The spending you see in March retail data is yesterday's confidence. What Michigan is measuring is tomorrow's restraint.

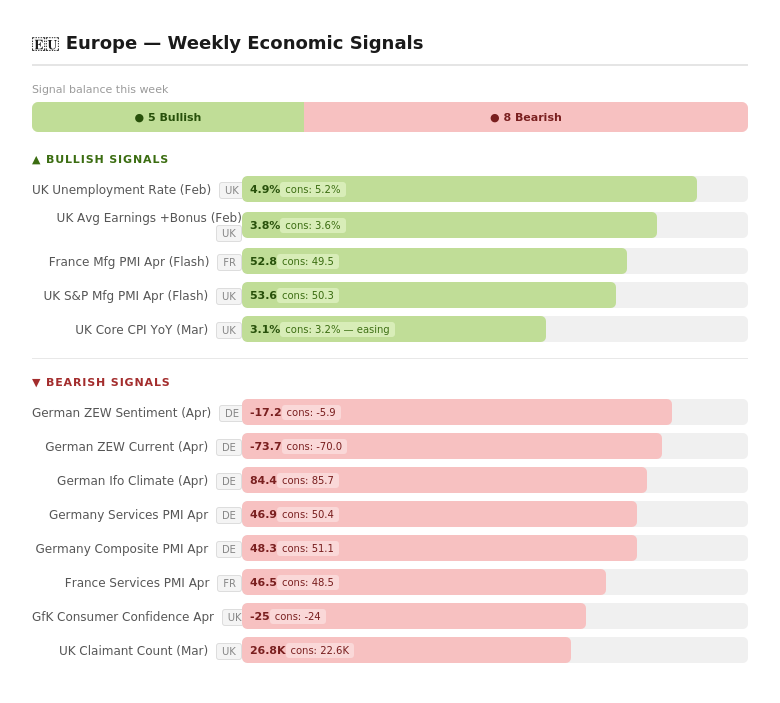

Germany is in a more honest position — it simply does not have a good story to tell right now. ZEW sentiment at -17.2 against a -5.9 consensus is worrisome. The services sector is contracting. Business climate is falling month after month. Germany built its post-war prosperity on selling manufactured goods to the world. That model is under serious pressure and nothing has replaced it yet. The UK is holding together but the claimant count trajectory is worth watching. China's FDI outflows accelerating to -7.3% tells you that foreign capital is making a quiet but consistent judgment about risk.

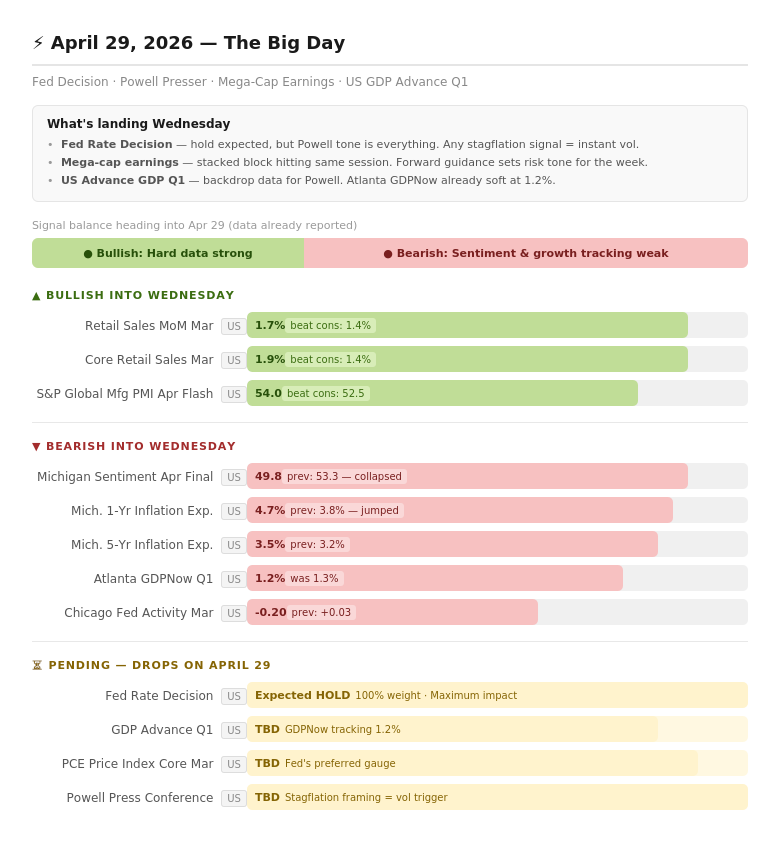

Now. Wednesday.

Understand what is actually happening on April 29. You have the advance GDP estimate for Q1, core PCE, the Fed rate decision, and Powell speaking live. In any normal week, any single one of these would dominate the conversation. They are all landing together. Start with GDP. The Atlanta Fed has been tracking Q1 at 1.2%. If that number holds, it does not just mean the economy slowed but that it was already slowing before the April sentiment collapse, before the tariff escalation uncertainty, before any of the forward-looking anxiety we are now measuring. You would be looking at an economy that entered its soft patch earlier than the headlines suggested. Now put core PCE next to that. If inflation is still running firm while growth is printing 1.2%, Jerome Powell walks into that press conference holding a textbook stagflationary signal. Not stagflation as a confirmed condition, but stagflation as the question every serious investor in that room is going to ask him whether he uses the word or not.

This is where Wednesday becomes genuinely difficult to navigate. Powell cannot cut rates into firm inflation without destroying credibility that took three years to rebuild. He cannot hold rates into weakening growth indefinitely without becoming the instrument of the slowdown. Every word in that press conference will be read as a signal about which risk he considers more dangerous. That judgment, made publicly on Wednesday, sets rate expectations for June, July, and September. Those expectations flow into every discount rate calculation in every equity model, into every corporate refinancing decision, into dollar positioning globally.

The mega-cap earnings sitting in the same session are not just a corporate story. Look at what those companies' forward guidance actually measures. Advertising revenue tells you whether small and mid-size businesses are still willing to spend on growth. Enterprise software demand tells you whether CFOs are still investing or beginning to pull back. If the guidance from those earnings is cautious, it is not a technology story. It is a leading indicator of business confidence that will show up in employment and investment data two quarters from now.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform