Articles

- BLOG / Articles / View

- Articles

Monday Macro View: Can Devon's $58B Bet Deliver in today's market?

By Osama on May 11, 2026 in Market Sentiment

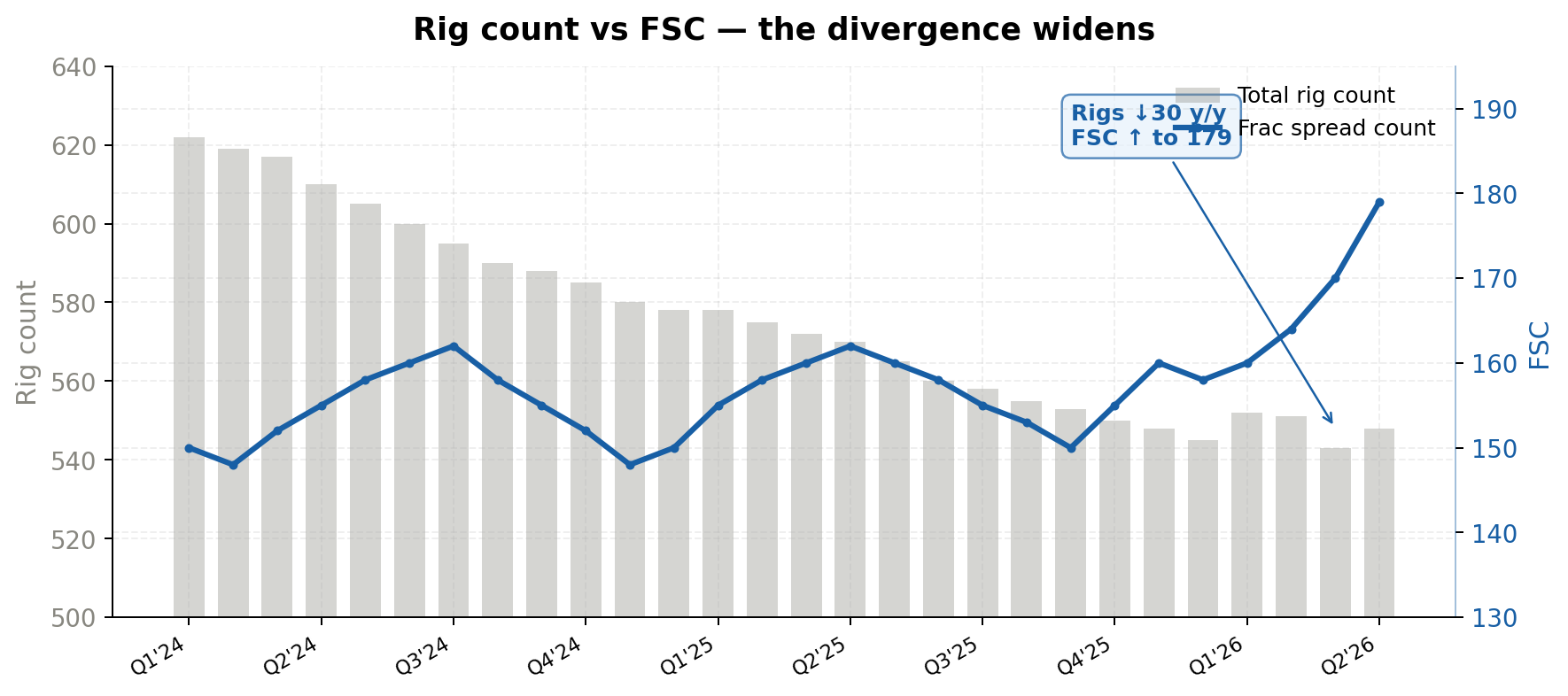

Hello everyone! Welcome to the Monday Macro View. This is an extended edition, and the data deserves the extra space. FSC rose 5 to 179, FJC added 5 to 225, and the rig count ticked up 1 to 548. That is the second consecutive week of gains across both completion metrics, and FJC now sits 18 counts above its year-ago level. The trend we flagged 60 days ago— continued gains in FSC and FJC — stil holds true. The completion side of the US upstream is pulling away from the rig count, which remains 30 units below where it stood a year ago. Efficiency gains, longer laterals, and the consolidation-driven rationalisation of drilling programmes are the obvious explanations, but they only tell part of the story. The other part is that the operators driving this activity are getting bigger.

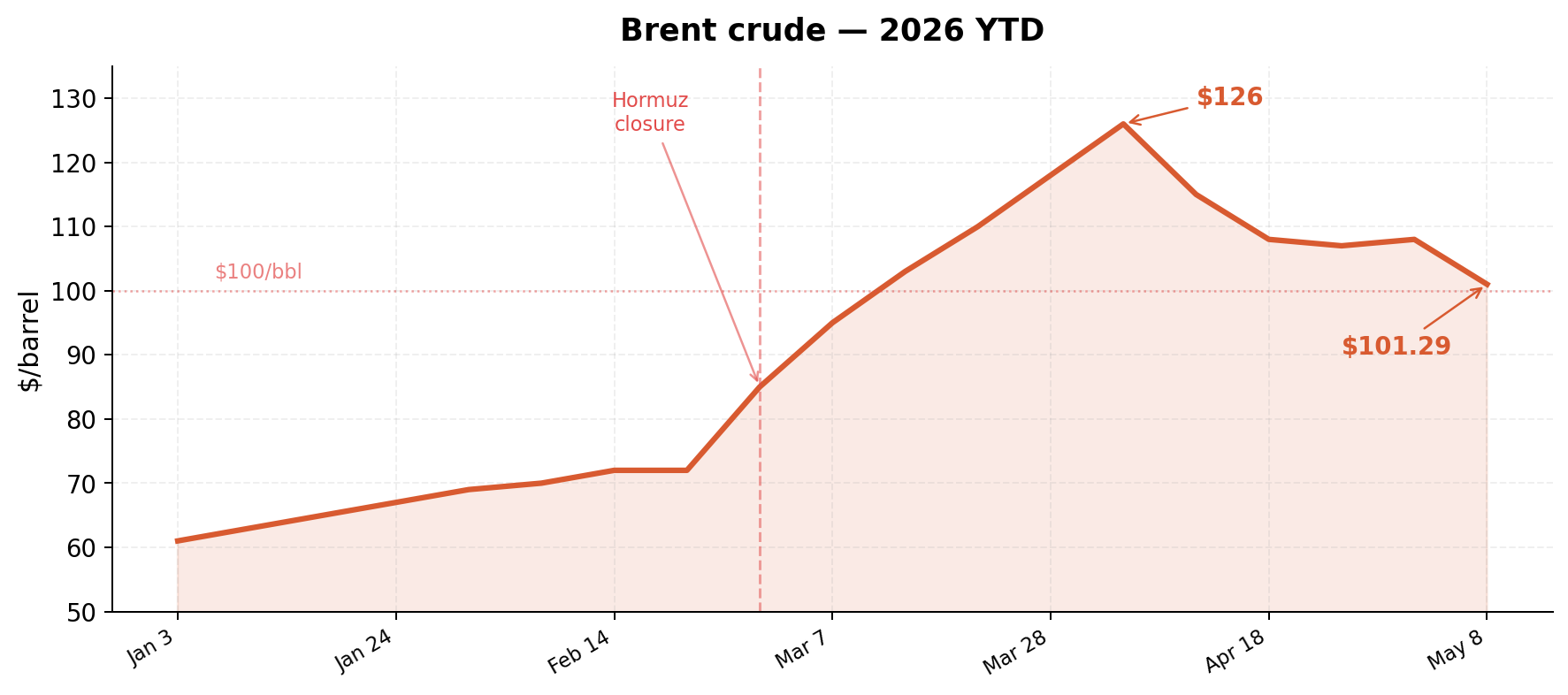

Brent traded in a jaw-dropping $12 range this week, printing $108.80 before collapsing to $96.80 intraday on Wednesday, then clawing back to close Friday at $101.29. The volatility is a direct expression of the Hormuz impasse: US and Iranian forces exchanged fire in the strait on Thursday, Iran launched missiles at the UAE on Friday, and the US struck two Iranian tankers attempting to evade its naval blockade. President Trump insists a ceasefire remains in effect. The physical market disagrees — Dated Brent is trading well above $130, and Middle Eastern grades have printed above $135, reflecting severe stress on crude buyers. The IEA says the conflict is removing roughly 14 million barrels per day from global supply. The SPR continues to bleed: 17.5 million barrels released since mid-March, part of a coordinated IEA drawdown of 400 million barrels globally. SPR stocks sit at 397.9 million barrels. Every barrel drawn today creates a procurement obligation for 2027, and the world is still pulling record US exports — total petroleum product exports hit 14.2 million bpd two weeks ago and remain near that all-time high.

Against that backdrop, the macro story of the week belongs to Devon Energy. On Wednesday, Devon and Coterra formally completed their $58 billion all-stock merger, creating what management calls a premier large-cap shale operator. The combined company retains the Devon name, trades under DVN, and is headquartered in Houston with a significant Oklahoma City presence. Former Coterra shareholders received 0.70 Devon shares per Coterra share, giving them roughly 46% of the combined entity. The deal is anchored by a leading position in the economic core of the Delaware Basin, with expanded operations across the Anadarko, Eagle Ford, Marcellus, and Rockies. Devon is targeting $1 billion in annual pre-tax synergies by end of 2027. CEO Clay Gaspar described it as a defining moment. The market was less euphoric — DVN fell 8.6% on the day of close while peers were roughly flat, suggesting the deal premium is now fully priced and investors want execution proof.

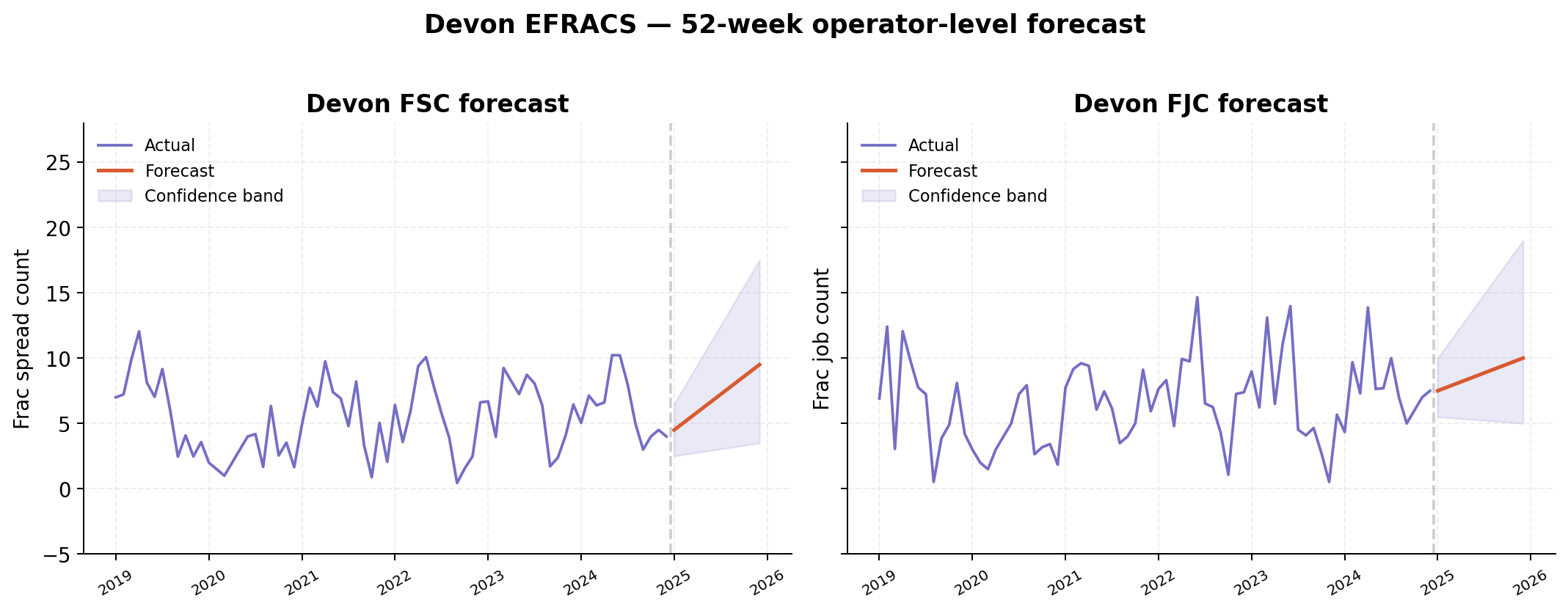

This is where Primary Vision's EFRACS platform earns its keep. Our operator-level data shows Devon's standalone frac spread count currently running at approximately 4–5 spreads, with the 52-week EFRACS forecast projecting a steady ramp toward 8–10 spreads. Devon's frac job count tells a similar story: current activity around 7–8 jobs trending toward 9–10 over the forecast horizon, with a wide confidence interval (roughly 3–18) reflecting the uncertainty inherent in any post-merger integration. The wide confidence band is itself informative — it captures the optionality Devon now holds. With Coterra's Marcellus gas assets folded in, the combined entity can toggle capital between oil-weighted Delaware completions and gas-weighted Appalachian programmes depending on the commodity price signal. Coterra suspended all Marcellus drilling and completion activity in August 2024 amid weak gas prices, then announced plans in February 2025 to restart two rigs and distribute frac activity through the year. The merger changes that calculus entirely: Devon's balance sheet and Delaware cash flow can accelerate the Marcellus ramp if Henry Hub cooperates. Our EFRACS data will begin reflecting the combined entity's completion footprint in coming weeks, and we expect the merged Devon to register as one of the larger operator-level completion programmes in our dataset.

The Devon–Coterra close also puts the rig-count-versus-completion-count divergence into sharper relief. Baker Hughes reported 548 total rigs for the week ending May 8 — up 1 on the week but 30 below year-ago levels. Oil rigs account for 75% of the total at 410 units, down 57 year-over-year. Gas rigs, by contrast, have risen 21 year-over-year to 129, reflecting the structural pull of global LNG demand. Yet US crude production sits at 13.573 million bpd, within 289,000 bpd of the all-time record. The industry is doing more with less drilling iron, and the consolidation wave, Devon–Coterra, Diamondback–Endeavor, the steady accretion of Permian acreage into fewer, larger operators, is a core reason why. Larger operators run longer laterals, optimise pad sequences, and deploy completion capital more efficiently. The result is a US upstream that is structurally more productive per but increasingly sensitive to completion-side bottlenecks. That is why our FSC and FJC data matter more today than at any point since the shale revolution began.

Readers should watch three things. First, service pricing: Halliburton called North America the 'early innings of a recovery' but RPC said last week it won't reactivate stacked frac fleets at current rates. If completion activity keeps climbing and pumpers refuse to bring idle capacity back, day rates move higher. Second, the EIA now projects US crude slipping from 13.5 million bpd to 13.3 million by year-end — the first extended decline forecast since the shale renaissance began. Third, Hormuz: Iran's response to the latest US proposal was shared with Trump on Monday and he said "he didn't like it". Any reopening reshuffles the global barrel count overnight. The trend in completions remains higher, but the questions around it are getting harder. More next Monday.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform