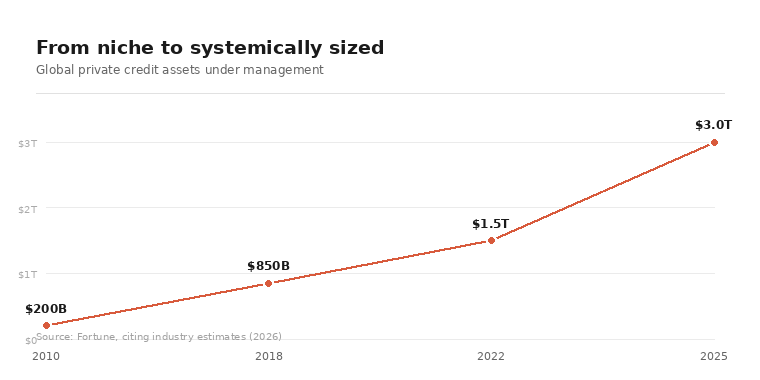

Private credit is a three trillion dollar market that runs on a quiet promise: the loans inside it are priced fairly even though almost nobody can see them trade, and investors who put money in can get a meaningful piece of it back whenever they ask. Both halves of that promise are being tested right now, in the same few weeks, and neither is holding up cleanly.

Start with the pricing half. In September 2025, Tricolor Holdings, a subprime car lender, and First Brands, an auto parts company, collapsed within a month of each other — Tricolor amid allegations of pledging the same collateral to multiple lenders, First Brands owing roughly ten billion dollars with missing funds still being traced. Debt from both sat in private credit portfolios marked near full value right up until it wasn't: First Brands' top loans eventually settled around a third of face value, Tricolor's lower tranches at twelve cents on the dollar. JPMorgan took a $170 million hit, UBS disclosed over $500 million of exposure, Jefferies flagged $715 million it later called questionable. What that really showed wasn't two bad borrowers — it was how long a loan can sit priced like nothing's wrong in a market where the price is whatever the manager holding it says it is.

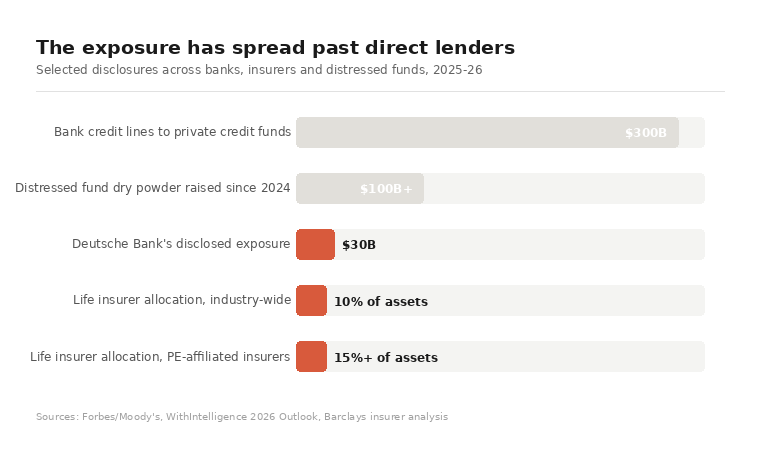

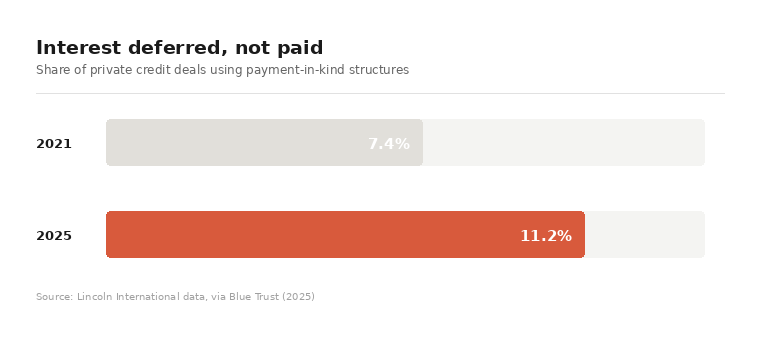

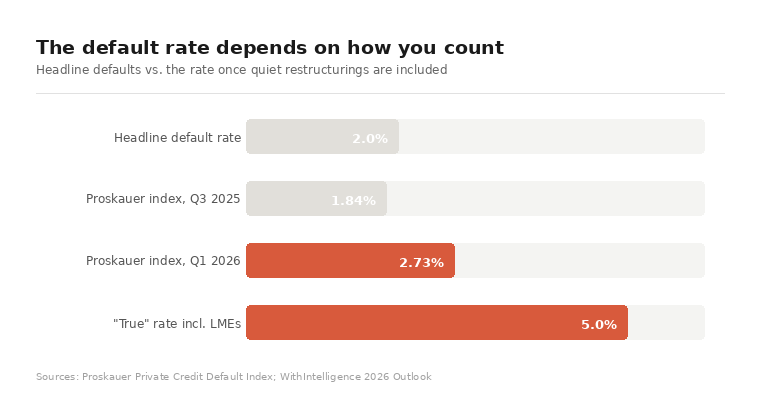

The quieter signals point the same direction. Payment-in-kind loans, interest paid in more debt instead of cash, have nearly doubled since 2021, from 7.4 percent of deals to over 11. Headline defaults look tame under two percent, but once quiet restructurings are counted, one estimate puts the real rate near five, and by April, Fitch had the U.S. private credit default rate hitting a record 6 percent. Deutsche Bank has disclosed $30 billion of exposure, life insurers have pushed past ten percent of assets industry-wide. And recently, HSBC, Europe's biggest bank, pulled back from riskier private credit lending entirely, after a $400 million hit tied to a loan that fed into a now-collapsed UK mortgage lender. A bank walking away from a trade it was chasing months earlier is a different kind of signal than a fund quietly marking down a loan.

Now the second half of the promise — getting money back out — is cracking too, and this is the part landing in real time. Investors asked private credit funds for $15.6 billion back in the second quarter, a third straight quarterly increase, and got just $5.9 billion — 38 percent of what was asked, down from 53 percent the quarter before. That leaves a $9.7 billion backlog, the largest on record. Blue Owl's flagship fund saw 19 percent of its shares up for redemption, with 14 points of that unmet; Apollo and Ares weren't far behind at 16 and 14 percent requested. Meanwhile new money coming in has collapsed to around $500 million in May, down 75 percent since January — the fuel these funds need to keep lending is drying up at the exact moment investors are trying to leave.

None of this alone proves the industry is coming apart, and people close to it have reasonable arguments for why it won't. But here's where it turns genuinely worrying: these funds can legally cap redemptions at 5 percent a quarter, which is the only thing standing between a bad quarter and a forced fire sale. If inflows stay near zero through the back half of the year while requests keep climbing the way they have for three straight quarters, fund managers run out of room to keep gating politely — they either breach the cap and sell assets into a market with no real buyers, or they freeze redemptions outright, which is precisely the loss-of-confidence spiral the industry has spent a decade insisting couldn't happen here. That's the scenario to watch, not the one that's already occurred — and the people furthest from the lending decision, insurance policyholders and retail savers in these funds, are still the ones with the least way of seeing it arrive.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform