Articles

Free Read: Is there an oil supply glut or shortage?

By Osama on July 8, 2026 in Free Articles

There's a debate going on right now over whether oil is oversupplied or undersupplied, and both sides are pointing at real numbers while reaching opposite conclusions. So I went and pulled the data myself.

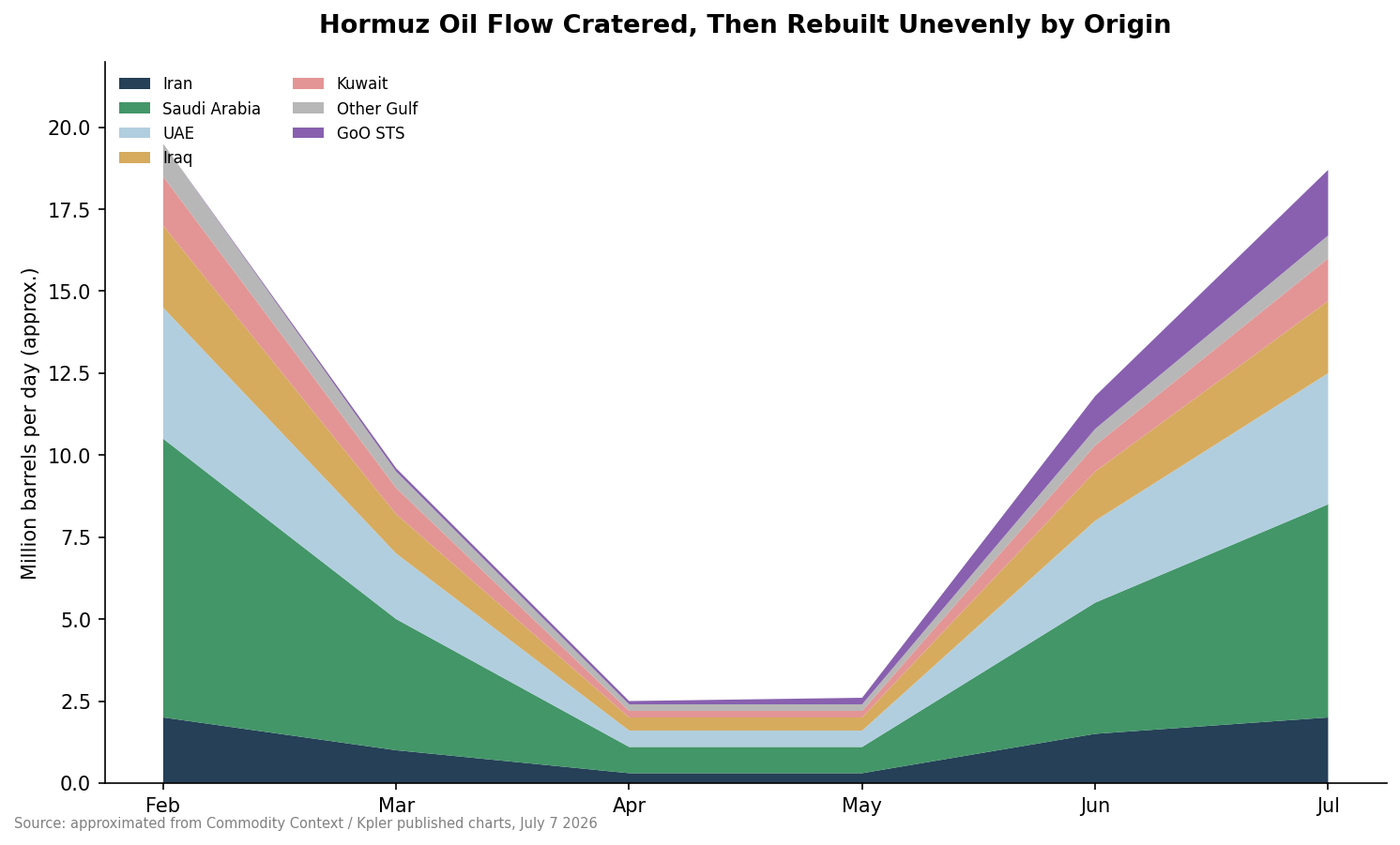

Start with what's actually moving through the strait. Tanker traffic through Hormuz used to run 49 vessels a day before the war. Through the worst of the fighting it fell to near zero, and even now, three weeks into the ceasefire, it's only running around 15 a day, with a single day in early July dropping to eight ships, the slowest stretch in two weeks. The oil itself tells the same story. Flows peaked above 20 million barrels a day in February, collapsed to roughly 2.5 million by April, and have since climbed back to somewhere in the 10 to 14 million range, with a growing share now moving through ship to ship transfers in the Gulf of Oman, a workaround that barely existed before the war and is now one of the larger pieces of the flow.

That recovery is already looking shaky. On day 20 of the ceasefire, the IRGC put a missile into a Qatari owned LNG tanker inside the strait, on the same corridor near Oman that Iran's navy had days earlier said it didn't recognize as legitimate. Washington responded by reimposing the oil sanctions it had lifted under the June ceasefire deal, and Brent moved up 3% to $76 while US crude cleared $70 for the first time since June 30. This doesn't cut off Iran's oil entirely. Iran is still sitting on tens of millions of barrels in floating storage, and it can still move and sell that oil. What changes is the terms: buyers now have to work around the US financial system, pay in yuan or through barter arrangements rather than dollars, and typically demand a discount for taking on that risk. So the sanctions snapback doesn't stop Iranian exports, it makes every barrel worth less to Tehran and harder to finance.

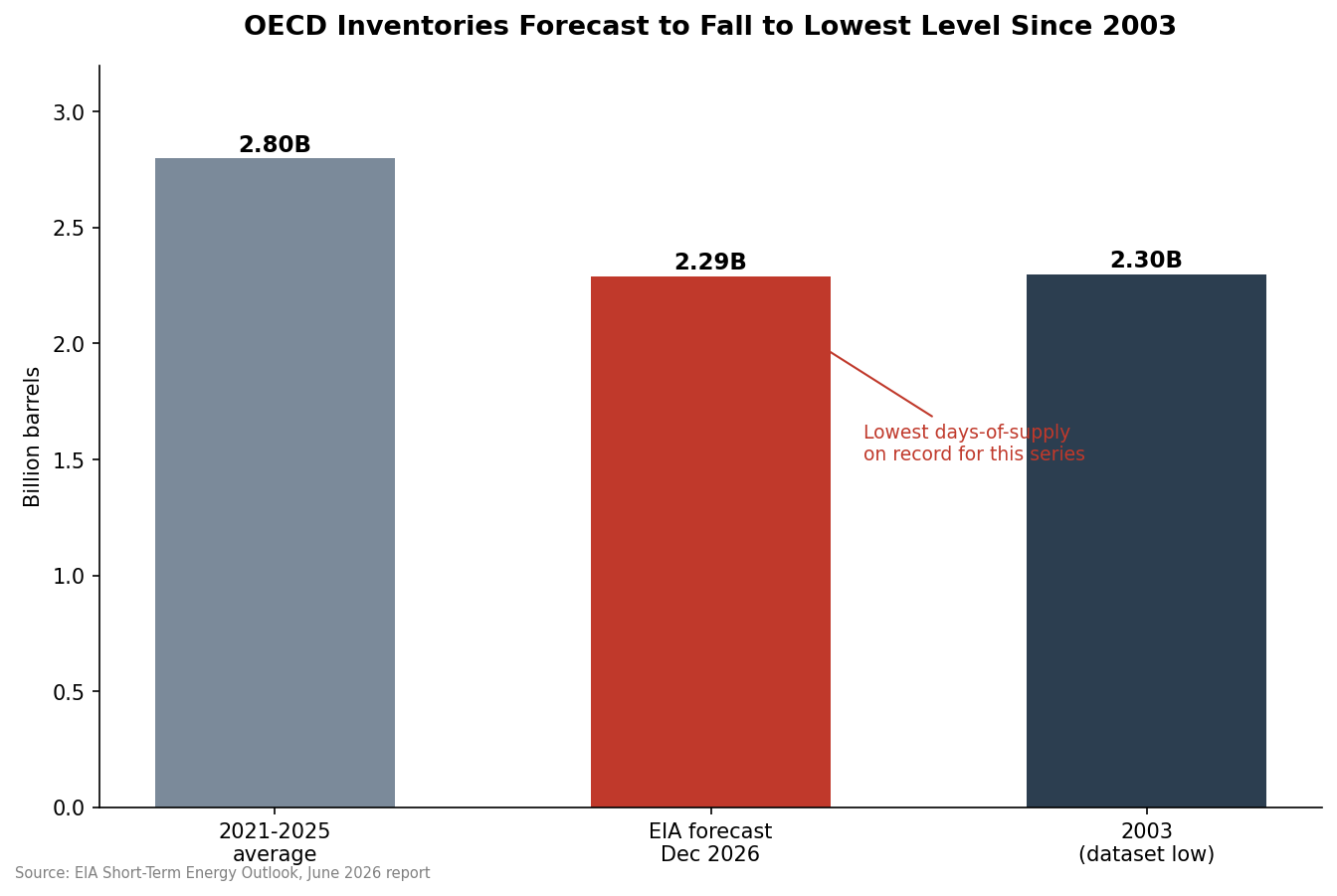

The near term picture is still one of real, measurable tightness. The EIA's recent outlook has OECD inventories falling to just under 2.3 billion barrels by year end, the lowest level since the dataset begins in 2003, and below the five year average of 2.8 billion. The IEA's numbers show a similar drawdown from a different angle: global observed stocks have been falling by an average of 3.8 million barrels a day since the war began, with OECD government held inventories at their lowest since December 1990. That's the case for tightness, and it's the residue of a nearly closed strait that three weeks of partial reopening hasn't undone yet.

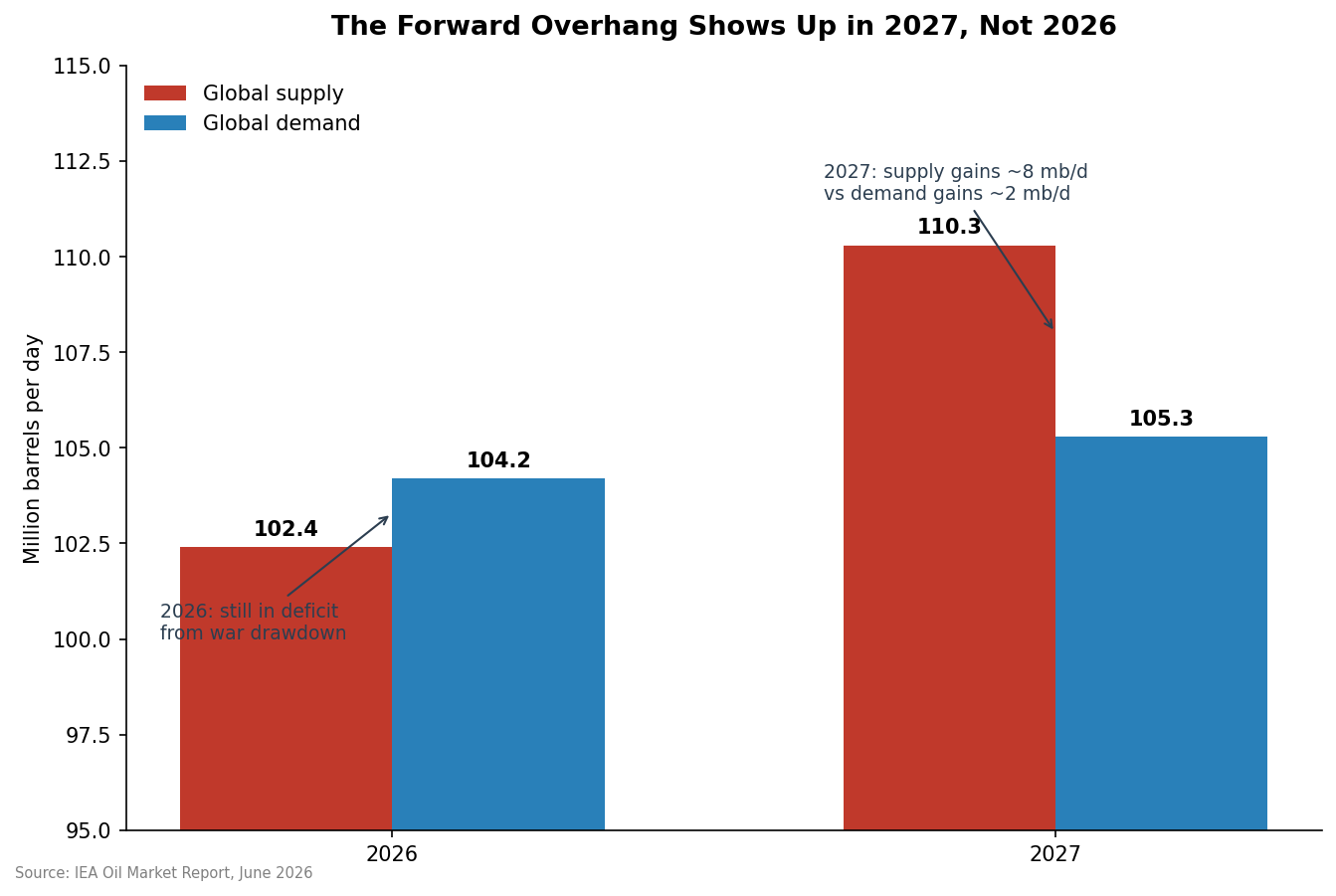

The glut argument sits about a year further out. The IEA's first look at 2027 has demand rising a modest 2 million barrels a day to 105.3 million, against supply climbing by roughly 8 million barrels a day to 110 million as Gulf producers normalize and OPEC+ finishes unwinding its cuts. That gap is what the market is leaning against, and it's large enough that managed money has pushed short positioning above 40%, the third highest reading in fifteen years, even with the strait still contested. It isn't a bet that oil is oversupplied right now. It's a bet that if the ceasefire holds, the market gets flooded with barrels next year.

Not everyone thinks that glut shows up on schedule. Some analysts point out that the usual signs of a real glut, like forward curves falling into contango or tankers sitting idle with nowhere to go, aren't showing up the way they did in 2015 or 2020, and that freight markets are still acting like supply security is the bigger worry, not surplus. That tension is what the crack spread is telling you in one line: refiners are still paying up for physical barrels today, while the futures market keeps pricing in a flood that gets pushed back a little further each time the IRGC decides the ceasefire's fine print doesn't apply to it.