Articles

Free Read: The Islamabad Gamble: Game Theory and Oil Markets

By Osama on April 23, 2026 in Free Articles

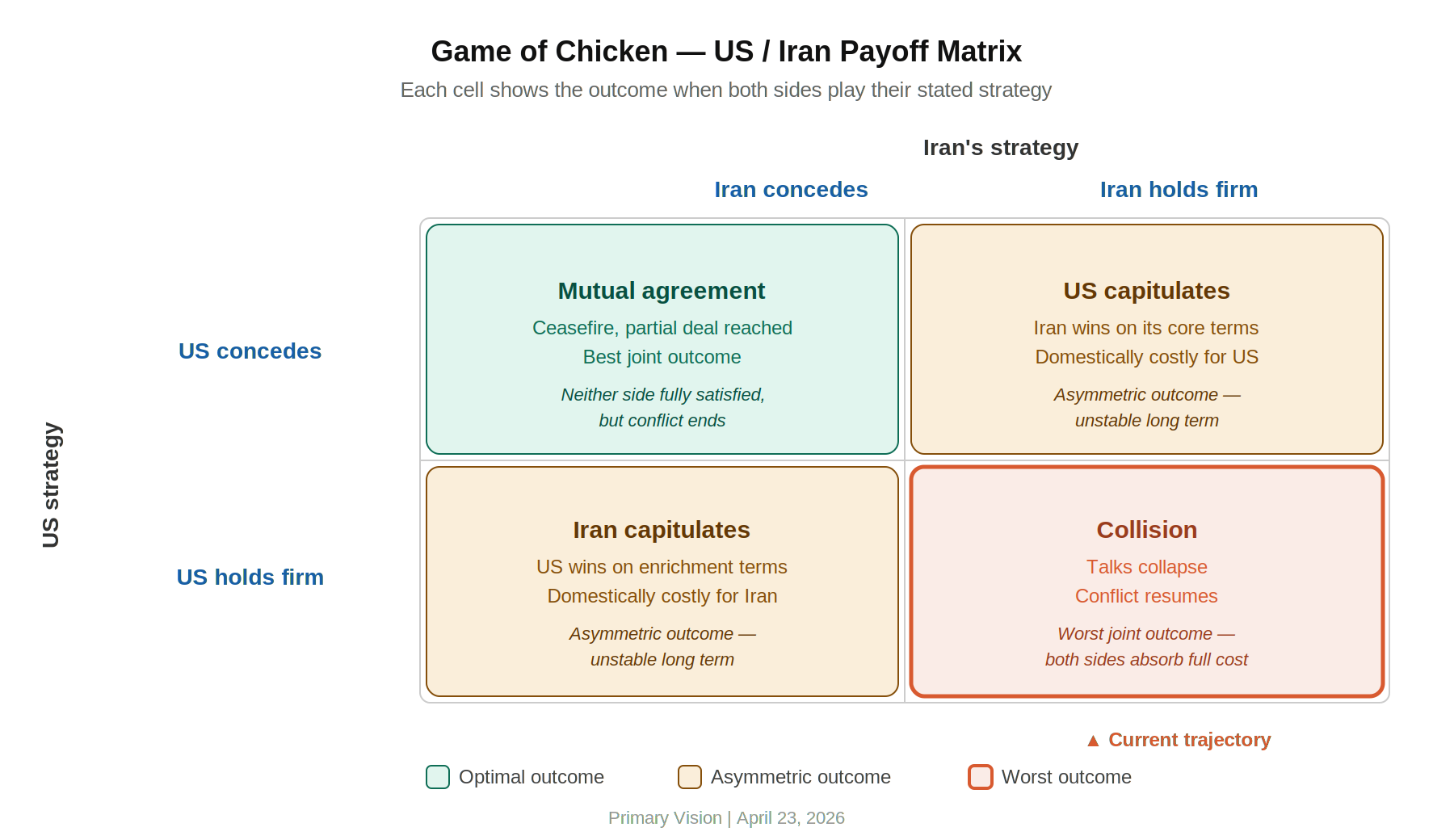

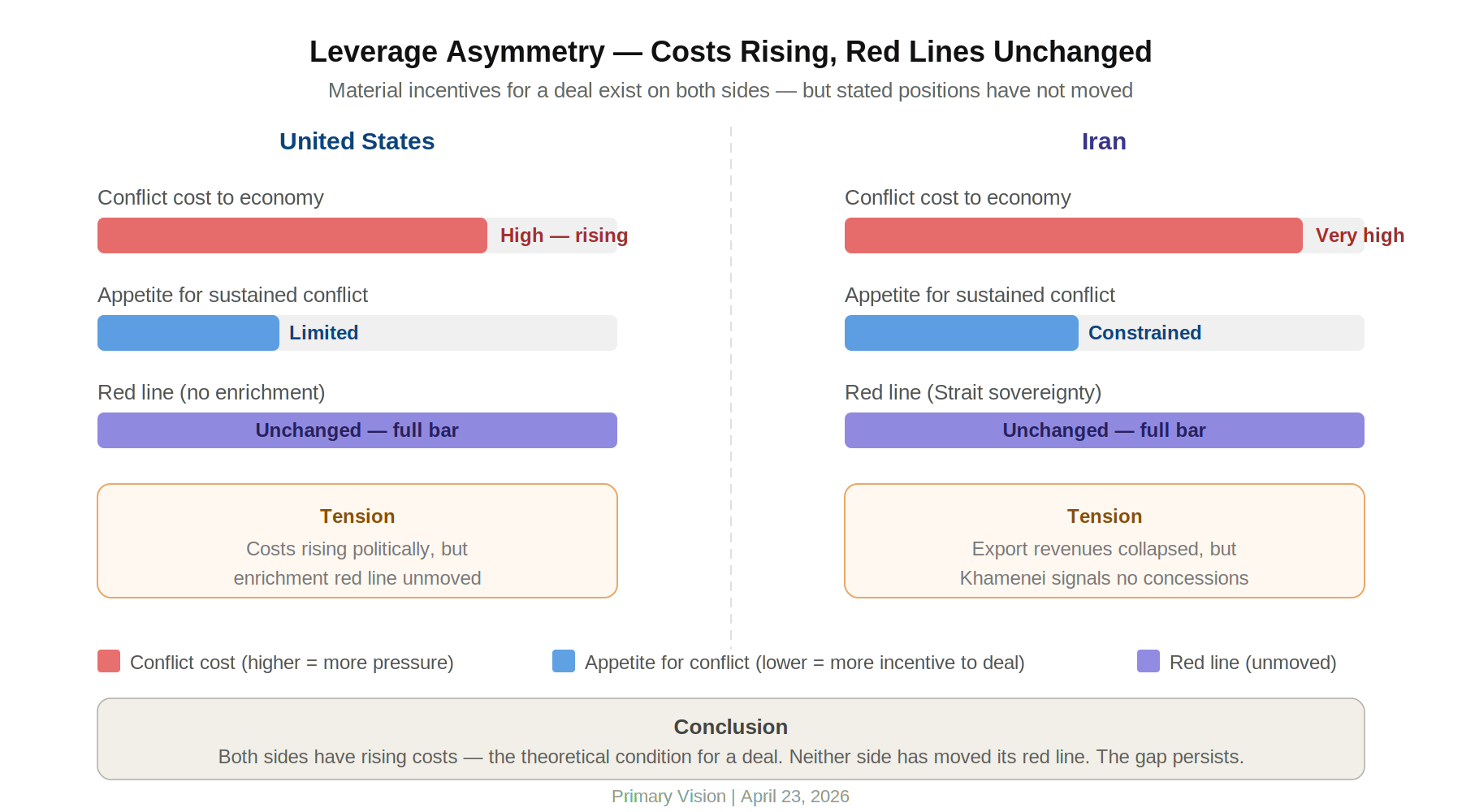

The second round of US-Iran negotiations in Islamabad may happen this weekend, opening up against a backdrop that has materially worsened since the first round concluded on April 12. Twenty-one hours of talks produced no agreement on Iran's nuclear program or control of the Strait of Hormuz. That outcome follows a predictable logic in bargaining theory: parties reach agreement when the cost of continued conflict exceeds the cost of concession. Both delegations currently believe the other side faces greater pressure. Until that calculation changes, structural resolution is unlikely.

Washington's position rests on a firm red line against Iranian enrichment. Tehran's position holds that its missile program and sovereign claims over the Strait are not subject to negotiation. Neither of these positions is a tactical opening offer — both reflect underlying security doctrines that domestic political actors on each side have publicly committed to. The naval seizure of an Iranian-flagged vessel on April 20, which Tehran described as armed piracy, added an additional grievance just as delegations were preparing to reconvene. It narrowed the space for the Iranian delegation to enter the second round with flexibility.

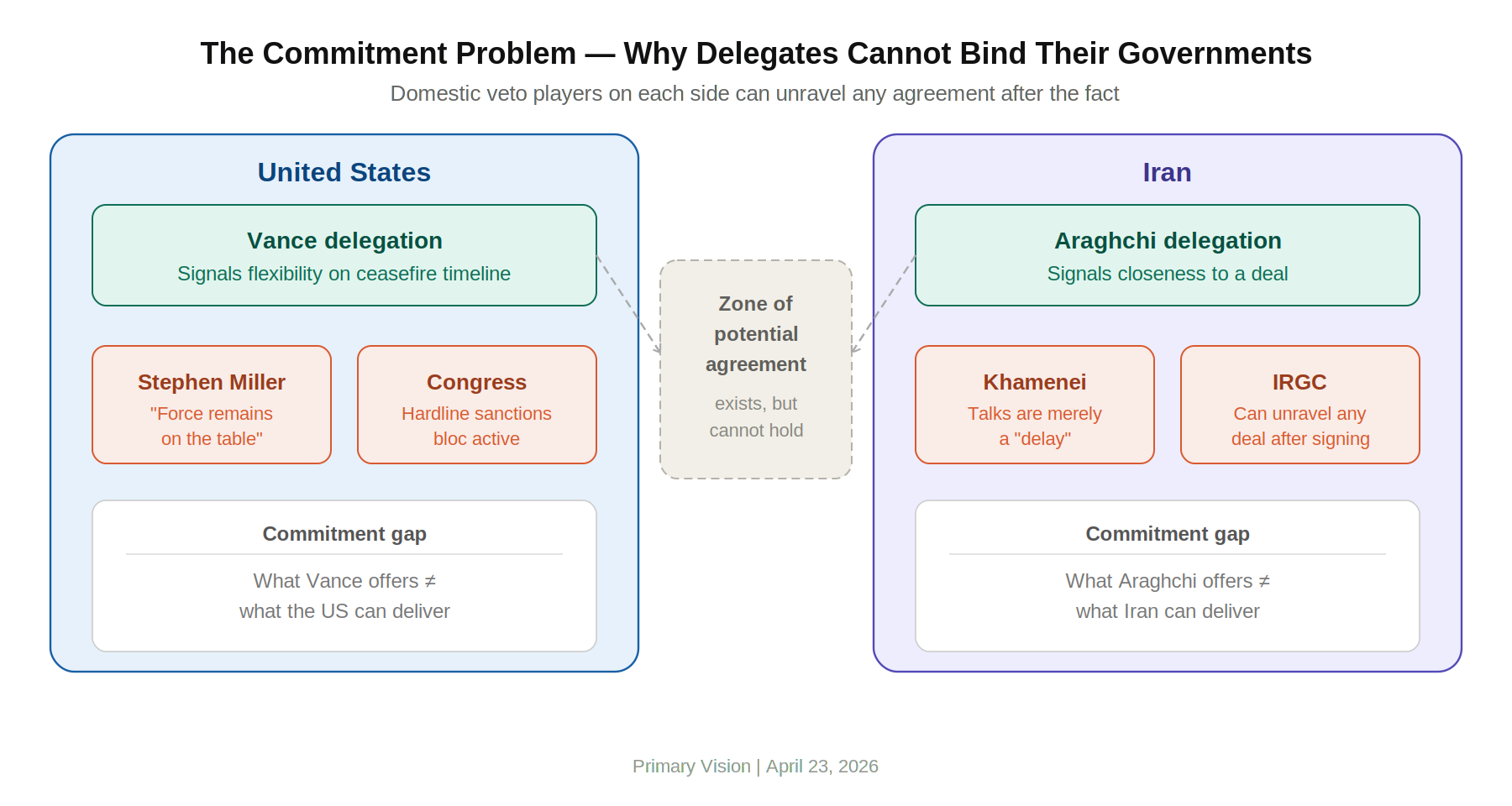

What makes this negotiation difficult to resolve in a single session is a commitment problem. Iran's foreign minister Araghchi has stated that the sides were close before the US changed its terms. Vice President Vance has said Iran moved toward the US position but not sufficiently. Both accounts can be accurate simultaneously, which is characteristic of a coordination problem rather than a zero-sum dispute. The difficulty is that Khamenei has publicly framed the talks as a delay, not a negotiation, signaling that the supreme leadership has not authorized meaningful concessions. On the US side, Stephen Miller's continued reference to military options runs counter to any signal of negotiating flexibility. When both governments send internally contradictory signals, the other side rationally discounts any offer as non-binding.

The oil market context in this regard is not a secondary variable, it defines the material costs each side is absorbing and therefore the incentive structure of the negotiation itself. Before the conflict began on February 28, the global market was on a trajectory toward surplus. The EIA's pre-conflict forecast placed Brent crude on a path toward $58 per barrel across 2026. That buffer has since been drawn down at a rate with no modern parallel.

Global supply fell by 10.1 million barrels per day in March as the Strait closure took effect, with OPEC+ output dropping 9.4 million barrels per day month-on-month. The IEA's April report recorded a single-month inventory draw of 85 million barrels, with stocks outside the Middle East Gulf declining by 205 million barrels — a rate of approximately 6.6 million barrels per day. Goldman Sachs estimates that total global oil draws, including refined products held in non-OECD storage, reached 10.9 million barrels per day in April — the steepest monthly draw on record since 2017. Cumulative supply losses since the start of the conflict are estimated at 474 million barrels. At the current rate of depletion, analysts across multiple institutions are tracking a path toward all-time record low inventories by late April or early May.

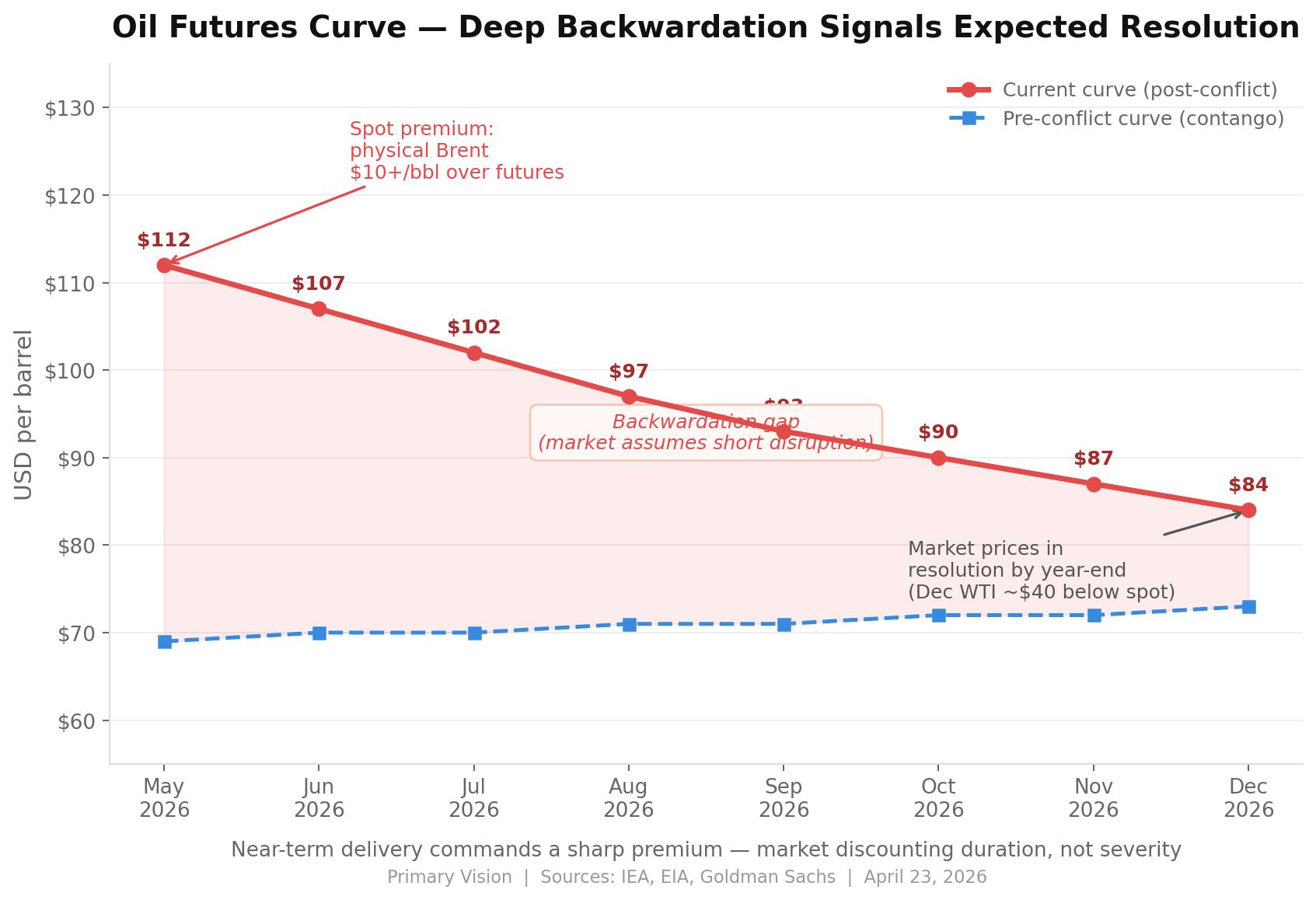

The oil futures market has responded in a way that itself carries analytical weight. The market is in deep backwardation: spot prices are significantly higher than forward prices, with December 2026 WTI contracts trading as much as $40 below near-term delivery contracts. Analysts at CME Group and CNBC interpret this structure as the market pricing in a short-lived disruption — an expectation that Hormuz flows will normalize within months. Goldman Sachs attributes the moderation in spot prices since the ceasefire to a shift from panic buying in March to active destocking in April, with Asian refiners, including Chinese buyers, re-offering cargoes they had recently secured.

Both delegations face genuine material costs from continued conflict. The Trump administration has acknowledged that the war has increased costs for American households, making it politically difficult to sustain. Iran's oil export revenues — approximately 1.9 million barrels per day before the conflict — are now severely constrained, and sanctions relief remains an explicit Iranian demand. These shared costs create the theoretical conditions for a deal. The obstacle is not the absence of incentive but the absence of a credible mechanism to implement and sustain any agreement once reached. A memorandum of understanding on a ceasefire extension — the outcome analysts consider most realistic — would provide temporary relief to both oil markets and diplomatic calendars. It would not resolve the underlying disputes over enrichment, Hormuz sovereignty, or sanctions sequencing. Whether delegations can accept that limited outcome, rather than arriving expecting the other side to have fundamentally changed its position, is the operative question. The oil market, drawing down its buffers daily, is operating on the assumption that they can.

Tags: