Articles

Free Read: The Market that cannot make up its mind

By Osama on April 4, 2026 in Free Articles

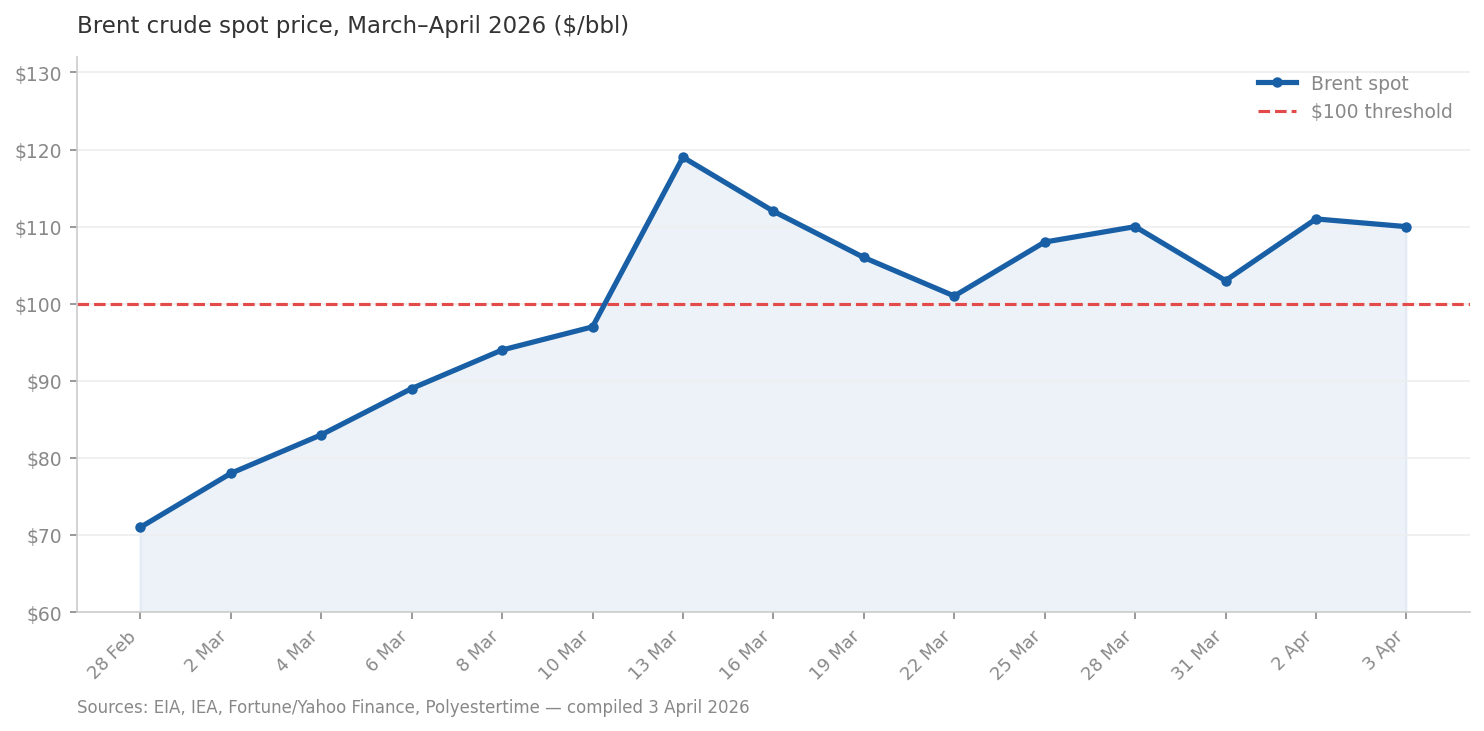

Five weeks into the most consequential oil supply disruption in living memory, the market is doing something curious: oscillating. Brent crude is trading in the $105–115 per barrel range, while WTI fluctuates between $103 and $113, reflecting a market driven primarily by geopolitical risk rather than pure fundamentals. One day optimism about a diplomatic breakthrough sends prices briefly below $100; the next, a statement from Tehran reverses all of it. Oil prices jumped approximately 5% in a single session, surpassing $106 per barrel, after markets reacted negatively to political rhetoric that dampened hopes of de-escalation. This is not a market finding equilibrium. It is a market being whipsawed between hope and reality.

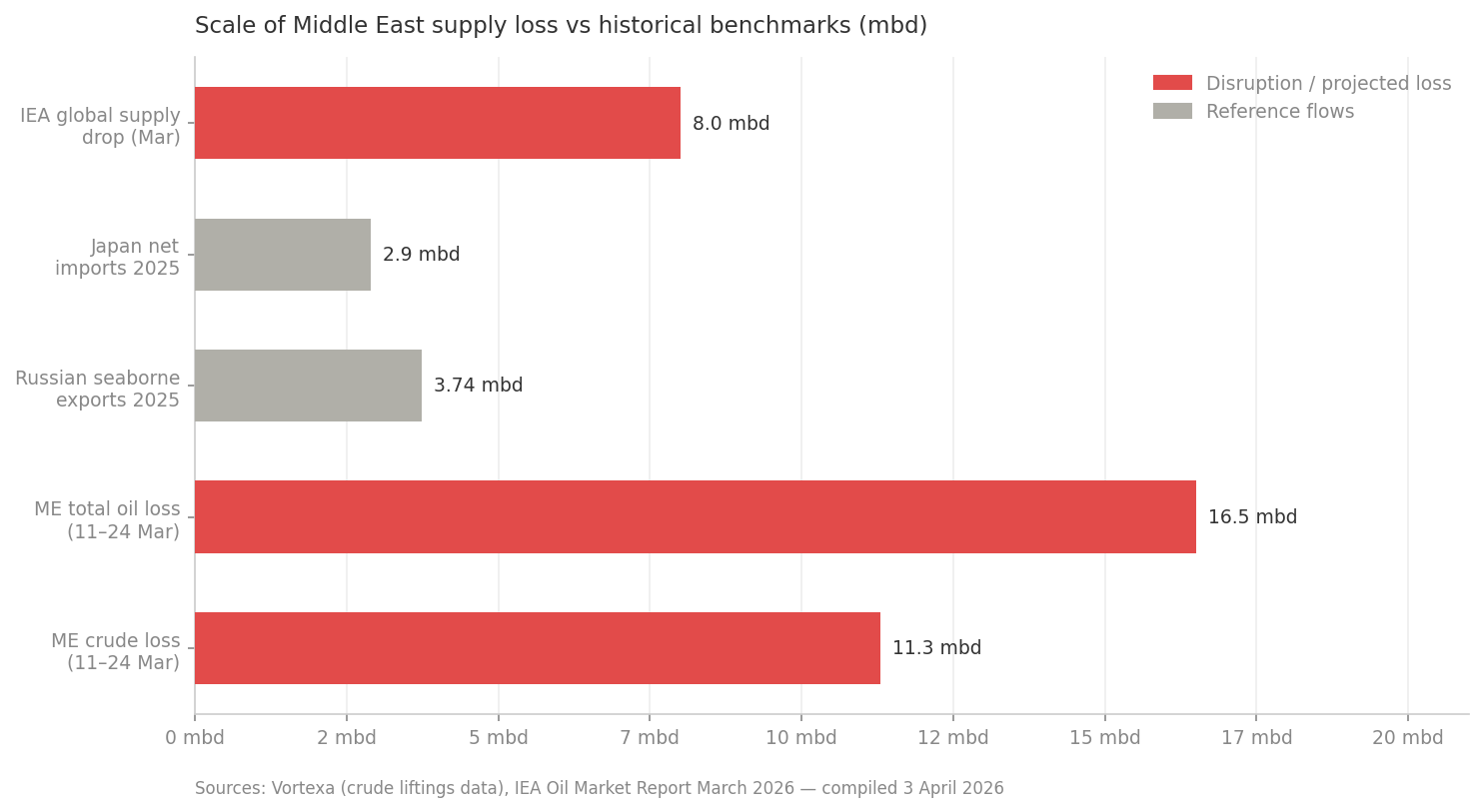

The reality, when you look at it plainly, is severe. The IEA has described this as the largest supply disruption in the history of the global oil market, with Gulf countries having cut total oil production by at least 10 million barrels per day as crude and product flows through the Strait of Hormuz plunged from around 20 mbd to a trickle. Global oil supply is projected to fall by 8 mbd in March, with curtailments in the Middle East only partly offset by higher output from non-OPEC+ producers. Strategic petroleum reserve releases from IEA member nations — a coordinated release of 400 million barrels agreed on March 11 — provide a meaningful but explicitly temporary buffer.

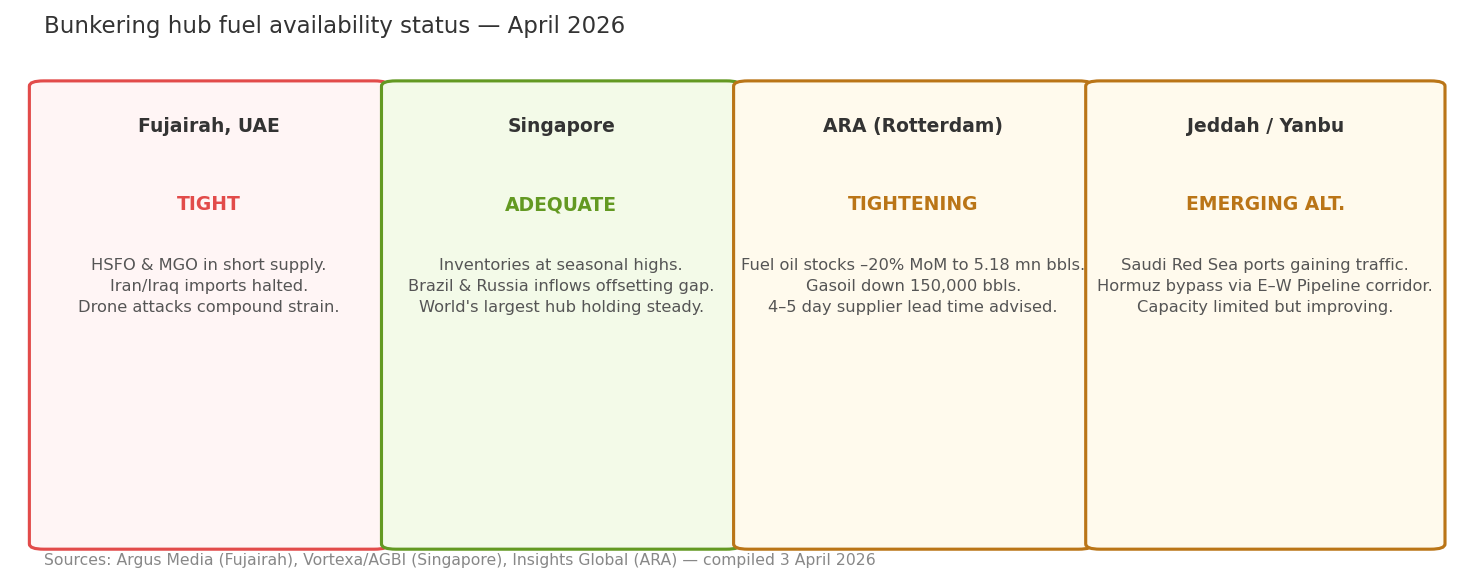

What makes this moment particularly complex for anyone managing fuel procurement is the growing divergence between where crude is priced and where physical product is actually available. The bunkering market illustrates this sharply. At Fujairah, both HSFO and MGO are in short supply, a situation compounded by the port's heavy historical dependence on HSFO imports from Iran and Iraq. Singapore, by contrast, is emerging as one of the main balancing points globally, with fuel oil arrivals from Brazil and Russia helping to offset the shortfall, keeping inventories at seasonal highs. The hub spread is widening, and that spread has real operational consequences: vessels are making longer detours to refuel, Atlantic Basin traders are redirecting cargoes eastward to capitalise on the arbitrage, and carriers are absorbing costs that BAFs were never designed to absorb at this speed.

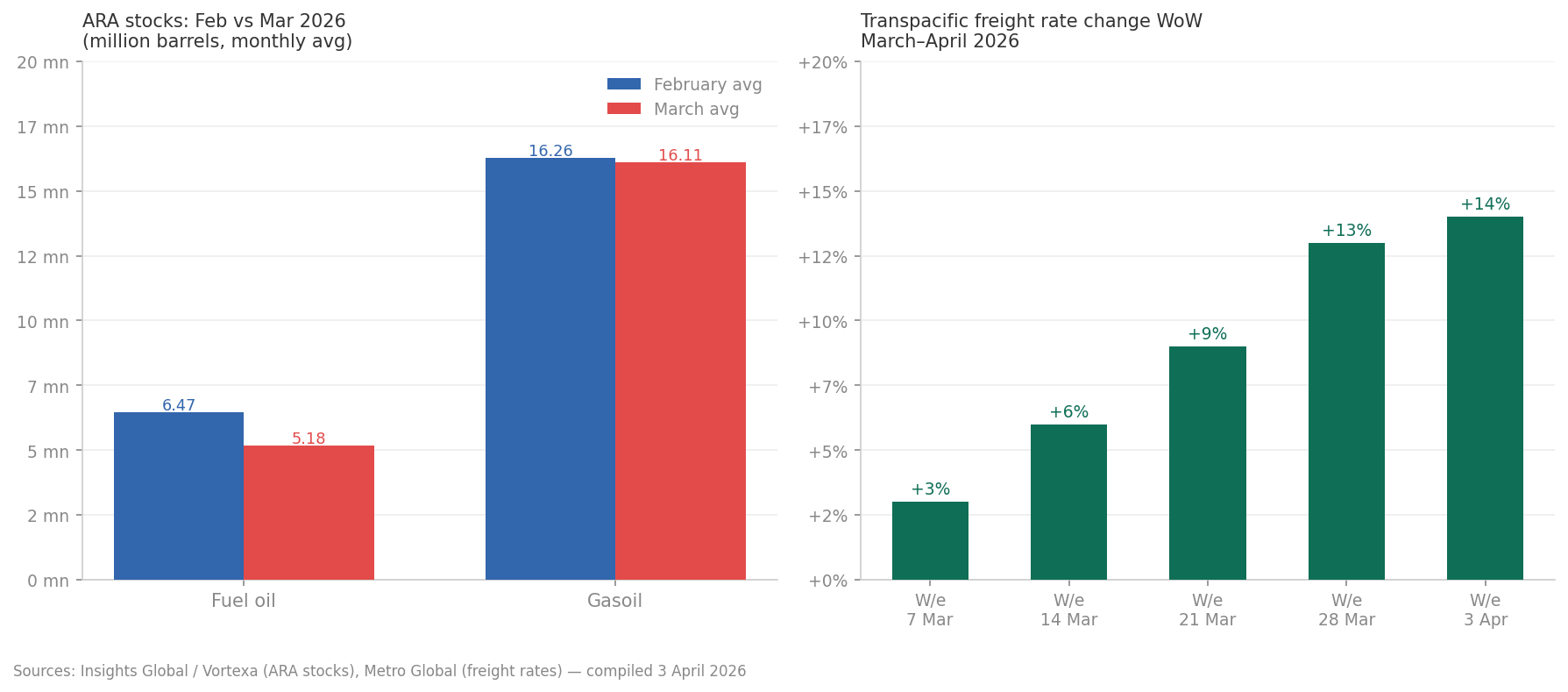

Those costs are feeding upstream into freight rates. On the transpacific, rates have increased by approximately 12–14% week-on-week, driven primarily by fuel cost escalation rather than demand strength, and analysts suggest that rates would need to rise by around 15% to fully offset current fuel cost increases. In the ARA region, the picture is also tightening. Data shows fuel oil stocks have declined 20% in March, slipping 1.29 million barrels to 5.18 million barrels on a monthly average basis, while gasoil inventories dropped 150,000 barrels to 16.11 million barrels. Imports of fuel oil into the region fell from 192,000 b/d in February to approximately 160,000 b/d in March, per Vortexa tracking. Suppliers at the ARA bunkering hub are advising buyers to plan for four to five days of lead time to secure reliable coverage — a modest operational adjustment today, but one worth taking seriously given the trajectory.

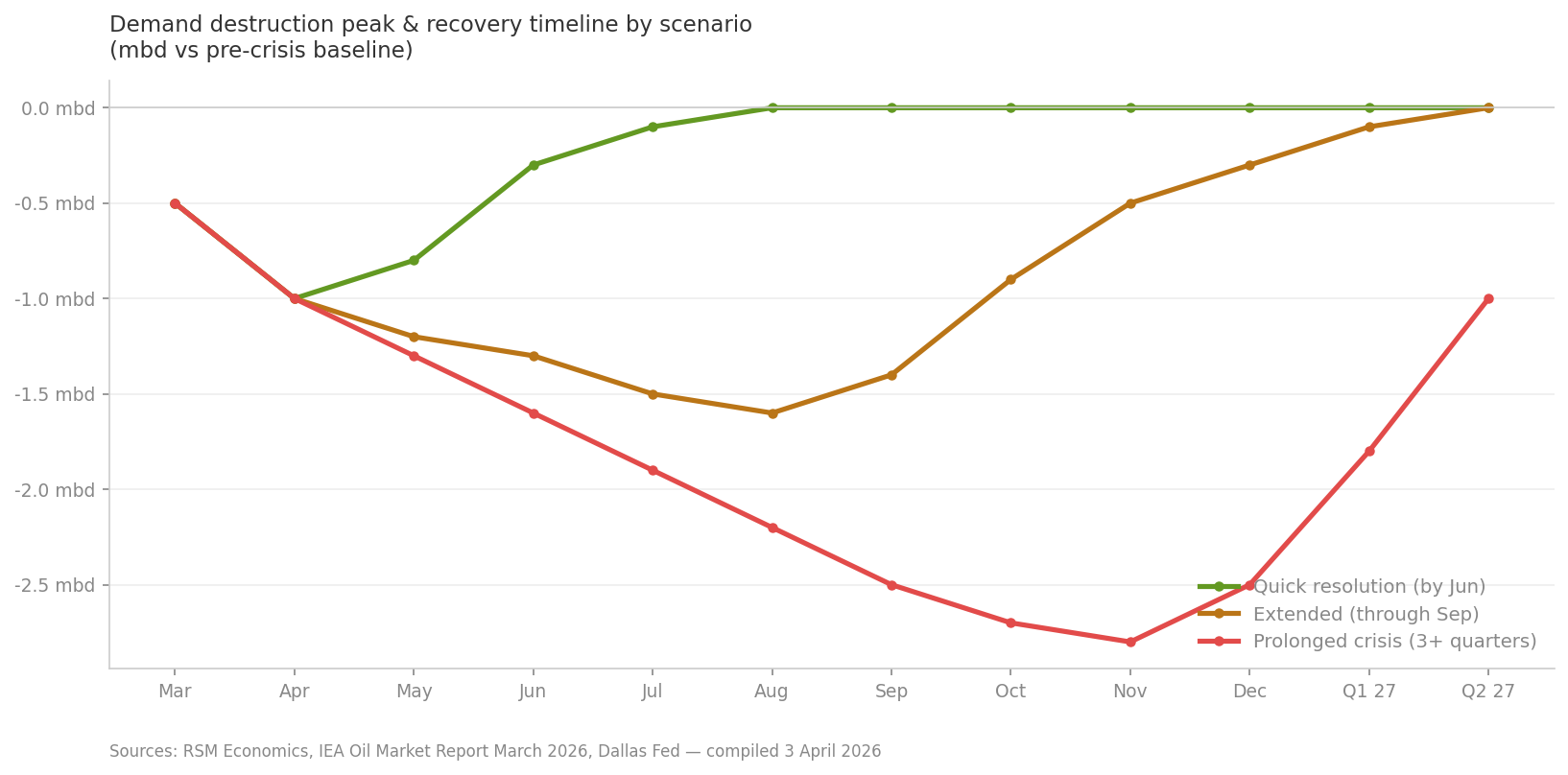

The demand side is beginning to respond as economics dictate it must. Widespread flight cancellations in the Middle East and large-scale disruptions to LPG supplies are expected to curb global oil demand by around 1 mbd during March and April compared to previous estimates, and the forecast for full-year 2026 demand growth has been revised down by 210,000 b/d to 640,000 b/d. Unless the conflict ends very soon, oil consumption will need to adjust to lower supply — perhaps much lower — and that demand destruction is now entering the equation in earnest. It means industries cutting runs, consumers reducing consumption, and economic activity contracting in ways that are slow to reverse even after supply normalises.

Material realities of the shortage will become inescapable when the last ships through the Strait finally arrive at their destinations, and that higher fuel costs will take months to fully translate into prices even where they have already hit balance sheets. The downstream effects, in other words, are still arriving. The price today is not the full story. For anyone planning fuel exposure over the next two to three months, that lag is the most important variable on the table.

Tags: