Articles

- BLOG / Articles / View

- Articles

Free Read: What Happens to Oil If the Peace Talks Fail?

By Osama on April 16, 2026 in Market Sentiment

WTI crude stood at approximately $91.91 per barrel on April 16, having gained 0.68% on the day but down roughly 4.5% over the past month from recent highs. Brent is trading near $94.89, essentially flat after a week of volatility that briefly pushed prices toward $100. What these numbers represent is a market held in suspension between the largest supply disruption in its modern history and the possibility — credible but fragile — that diplomacy may begin to resolve it.

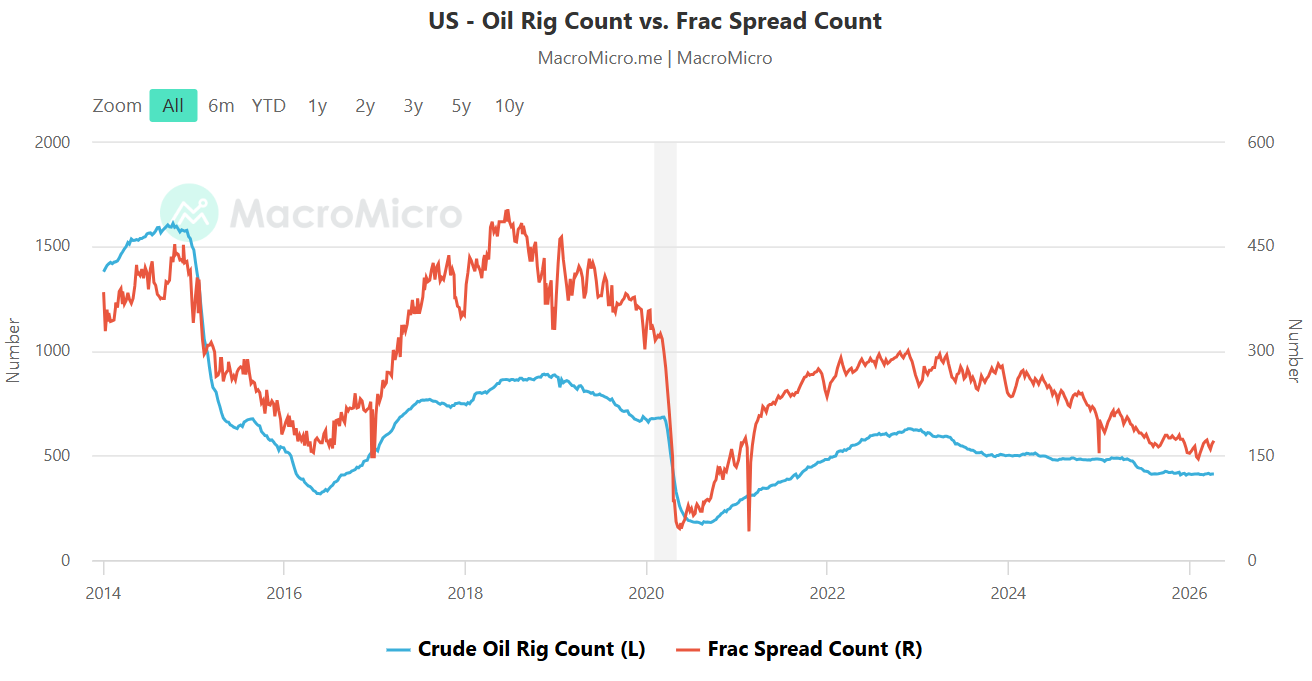

The most recent Primary Vision Frac Spread Count for the week of April 10 came in at 171 active frac crews, continuing its stellar recovery. US operators have materially accelerated completions. A frac spread count that holds steady rather than surges is a signal of structural consistency in the domestic upstream.

On the other hand, United States from becoming a significant beneficiary of the supply shock. US petroleum exports accelerated by 0.6 million barrels per day in March compared with a year earlier, as the conflict triggered a worldwide scramble for replacement crude and fuels. Crude exports slipped 0.3 million b/d year-on-year, more than offset by a surge of 0.9 million b/d in refined products. US crude exports have averaged 4.7 million b/d so far in April, up from 4.0 million b/d a year ago — at or near a record high. LNG facilities are running at near-peak capacity, pushing almost 18 billion cubic feet per day, approaching the December 2025 record. The destruction of Qatari export capacity has widened the Henry Hub-to-Asia spread to levels US exporters have not seen in years.

The underlying cause is straightforward. Global oil supply fell by 10.1 million barrels per day in March — the largest single disruption in the history of the market. Strait of Hormuz shipments, which exceeded 20 million b/d before the conflict, averaged only 3.8 million b/d in early April. Physical spot benchmarks surged to near $150 per barrel at the peak, far above futures prices, reflecting the acute scarcity of deliverable barrels. That physical-futures disconnect has narrowed on ceasefire optimism but has not closed.

The diplomatic calendar now carries unusual weight. Pakistani Field Marshal Asim Munir arrived in Tehran on April 15 carrying a message from Washington, accompanied by Interior Minister Mohsin Naqvi. The White House indicated it felt encouraged and that Pakistan would likely host a second round of direct talks. Iran's Foreign Minister Araghchi stated after the meeting that Tehran remains committed to peace and stability — language that keeps a process alive without committing to its resolution. Vice President Vance had characterized the American position from the first Islamabad round as Washington's final and best offer, with Iran's posture on nuclear enrichment remaining the unresolved core issue.

The price decline from the $99–100 range on April 13–14 to the current $91–95 reflects a partial unwinding of the war premium as the ceasefire held and diplomacy resumed. The market is now pricing the probability that the Islamabad framework can be reconstructed.

If talks fail, the consequences would not be linear. Shipping experts observe that even a full reopening of the strait would not quickly normalize flows, because tanker operators and insurers require durable security assurances before re-entering the Gulf. A collapsed negotiation provides none. The approximately 200-300 laden tankers waiting inside the Gulf would remain stranded, the Atlantic Basin crude premium would reassert itself, and the physical-futures disconnect could re-emerge with force.

The secondary consequences would fall hardest on Asia. China accounts for 37.7% of all crude flowing through the strait; Asian economies collectively receive 89.2% of Hormuz flows. A failure of second-round diplomacy would force Beijing to either deepen Russian import dependency or draw down strategic reserves at a pace markets would read as unsustainable. A Chinese demand contraction triggered by unaffordable oil would reduce global consumption volumes and eventually pull prices lower even as the supply shock persisted — elevated prices coexisting with falling throughput and compressed refiner margins worldwide.

The Ras Laffan LNG plant in Qatar, responsible for approximately 20% of global LNG production, has sustained missile damage that QatarEnergy warned could take up to five years to repair. A failure of negotiations means reconstruction cannot begin while the security environment remains active. Five years of reduced Qatari LNG capacity, with US facilities already near their physical ceiling, produces a structural global gas deficit that outlasts the conflict itself by years.

The frac spread count will be the metric to watch through all of this. Operators moving materially above 171 would signal conviction that the supply gap persists long enough to justify capital commitment. A count that stagnates signals skepticism about price durability or production capacity. Primary Vision's weekly data, read in sequence over the next four to six weeks, will be more informative than any single headline out of Islamabad or Tehran. The next round of US-Iran talks is the most consequential near-term variable in global energy supply. At 171 frac spreads and $91 WTI, the market is waiting to find out what happens next.

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform