Articles

How Will the Middle East Conflict’s Impact on Fertilizer Markets Shape Our Future?

By Mark on March 16, 2026 in Free Articles

Geopolitics can often change market dynamics rapidly and without any real warning. One of my favorite geopolitical quotes captures this: "There are decades where nothing happens; and there are weeks where decades happen." The current conflict in the Middle East is shining a bright light on just how vulnerable the global markets are to broad shortfalls. The market and global news have been showing us the issues in relation to oil and gas, but they are forgetting about one of the most important markets: fertilizer! Over the past several years, C6 has been highlighting how the fertilizer markets are changing because farmers are having to shift their nutrient blends—this has been driven by soil degradation, crop mix, and cost.

For years, we have been sounding the alarm on fertilizer cost and availability. They are a MASSIVE part of global energy infrastructure—and just as much downstream components of O&G as petrochemicals! The fertilizer markets were already balancing on a knife’s edge following the invasion of Russia into Ukraine. That conflict has increased the cost of natural gas into European ammonia facilities, stranded urea and potash behind sanctions and embargoes, and pulled crop volumes off the water. Now the current issues with shipping insurance and the Strait of Hormuz are just adding to an already struggling market.

This is why Sultech is so important. They can provide a diversified fertilizer option that delivers vital sulphates to the plant from areas that can avoid chokepoints—all at significant discount to the incumbent options, and while not being synthetic!

There is a push to help ease the pressure on farmers with President Trump making the following announcement: “The Trump administration authorized Venezuela to sell fertilizers and other petrochemicals to US companies, further loosening sanctions just as the Iran war tightens global supplies of critical crop nutrients.”[1] This is a great sound bite, but it doesn’t change the dynamics of the market.

- Venezuela fertilizer was already being sold in Latin America (largely Brazil and Colombia) at a discount

- Venezuela exported nearly 400,000 metric tons of urea to Brazil in 2025, according to UN Comtrade data. Smaller volumes also went to Colombia and Chile in recent years.

- Now Venezuela will be able to sell urea at market price, so this just takes away cheap urea to Latin America without increasing total market volume.

Venezuela has nameplate capacity around 3.3M tons per year, but due to mismanagement and poorly maintained equipment, the facilities can only create a fraction of that total today.

The market doesn’t have a “magic bullet” to deliver more volume into the fertilizer world. For example, even if Profertil (Venezuelan Urea Company) was producing at full capacity, it would still only be 250k tons a month . . . or a drop in the bucket versus current supply that has been impaired by the Middle East conflict.

It’s important to put into perspective just how impactful the current issues are in the Middle East and provide color on just how long this could impact markets.

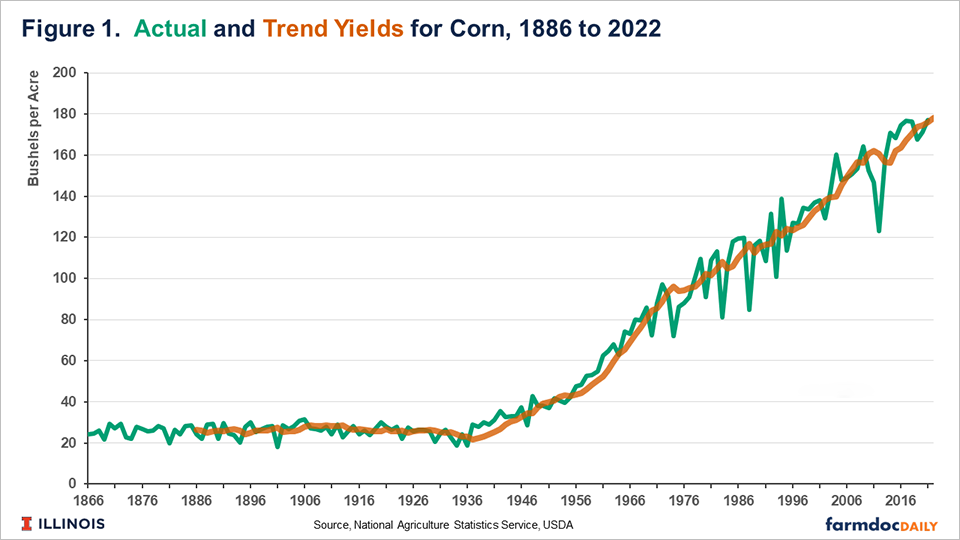

A farmer relies on four macro nutrients for a successful crop: Nitrogen (N), Phosphate (P), Potassium (Potash-K), and Sulphates (S). Nitrogen is a vital nutrient for yield that is delivered by way of urea. Modern civilization was built on the back of the Haber-Bosch process that delivered synthetic nitrogen to farmers at a fraction of the cost. The pivot in the chart gives you a clear indication of when the Haber-Bosch process was broadly adopted.

Everything was fairly stable from 1866-1936, and the key shift was the introduction of cheap nitrogen. Without the breakthrough, we would be facing crop yields that never would have supported the current world population. We’ve benefited from automation, improved seed genetics, and crop rotations, but none of those improvements impacted the market like synthetic fertilizer.

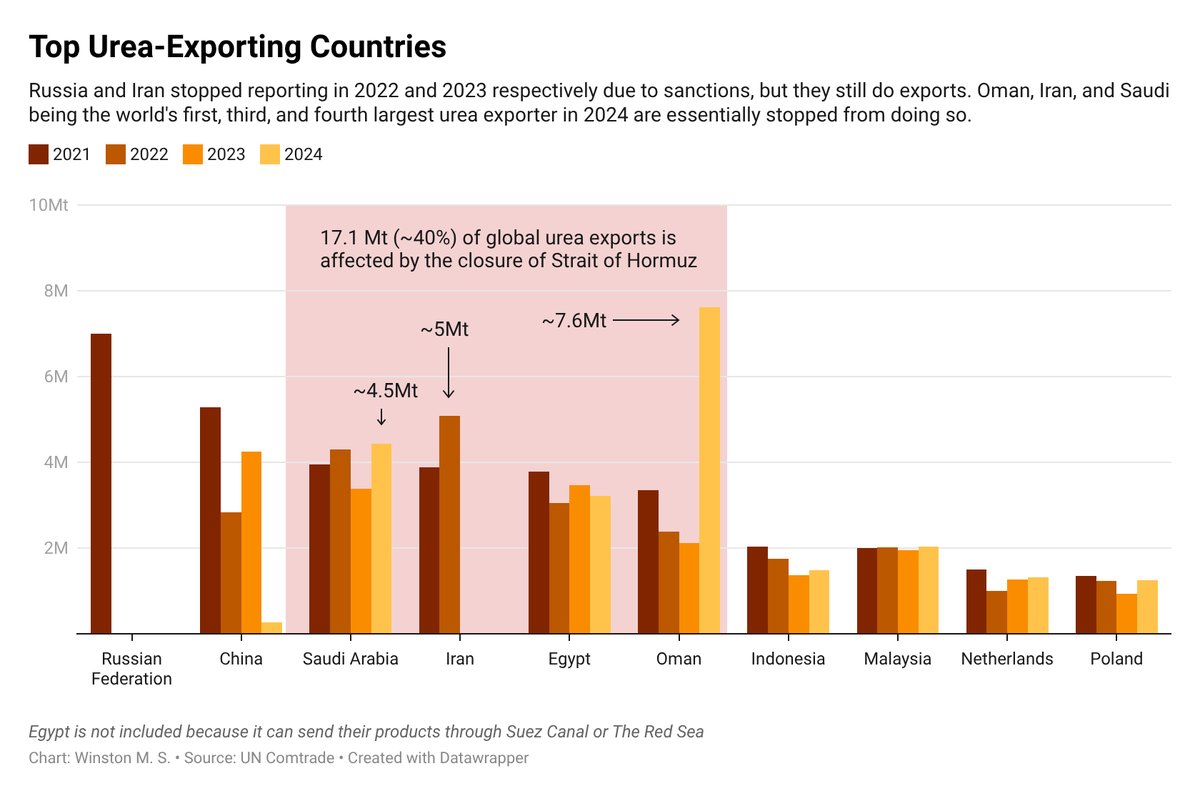

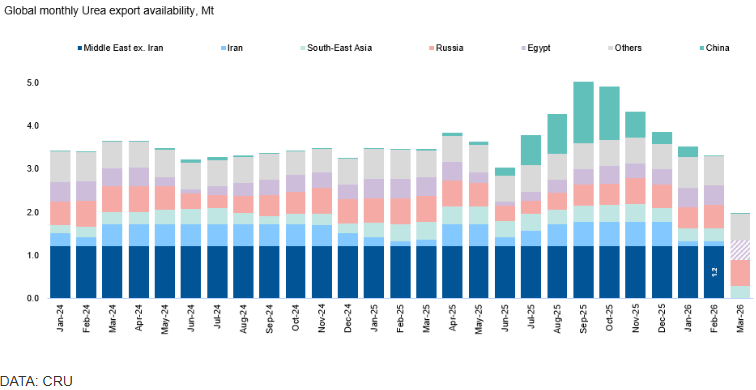

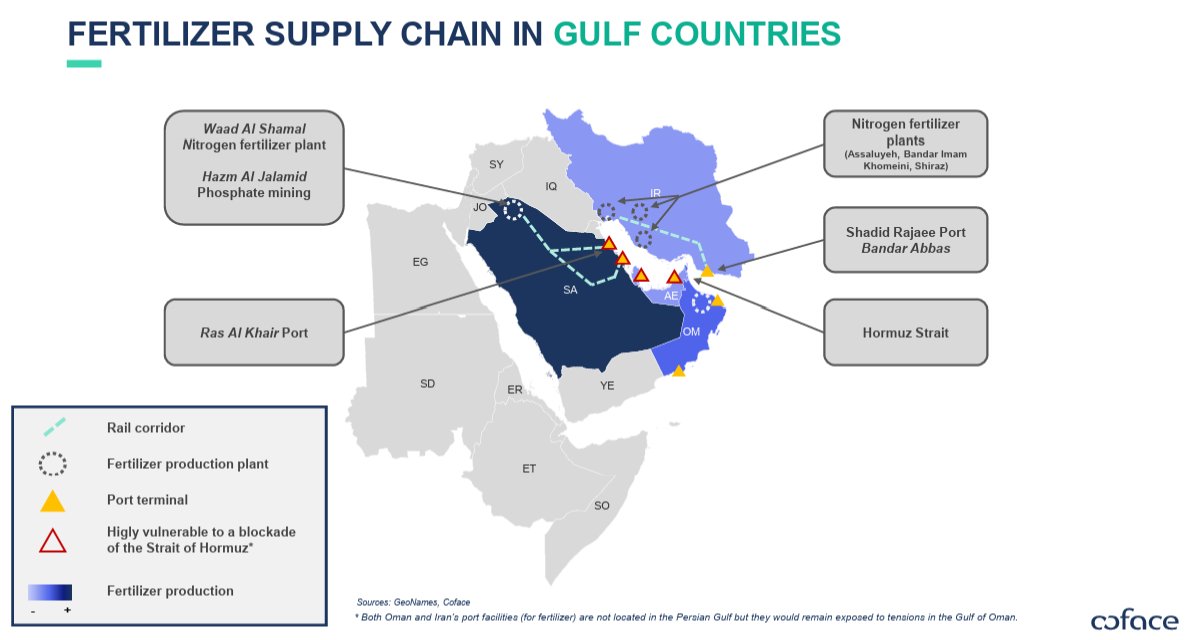

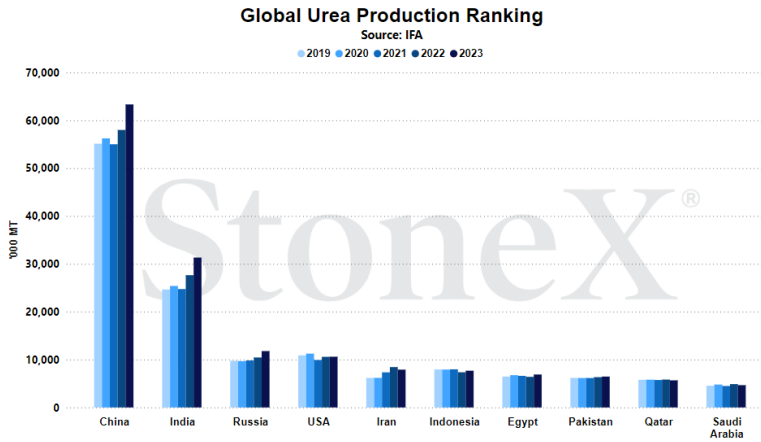

Geopolitical turmoil has been redrawing these shipping volumes over the past decade, and it’s likely to get much worse over the next few quarters. Russia was once a huge source of fertilizer to the global market, with urea and potash among some of the biggest components. Following the invasion of Ukraine and sanctions, Russia’s 7M tons per year of urea was pulled from the market. Iran was already restricted from broad exports due to sanctions, but now with the Strait of Hormuz shutdown, Saudi Arabia and UAE are added to this list.

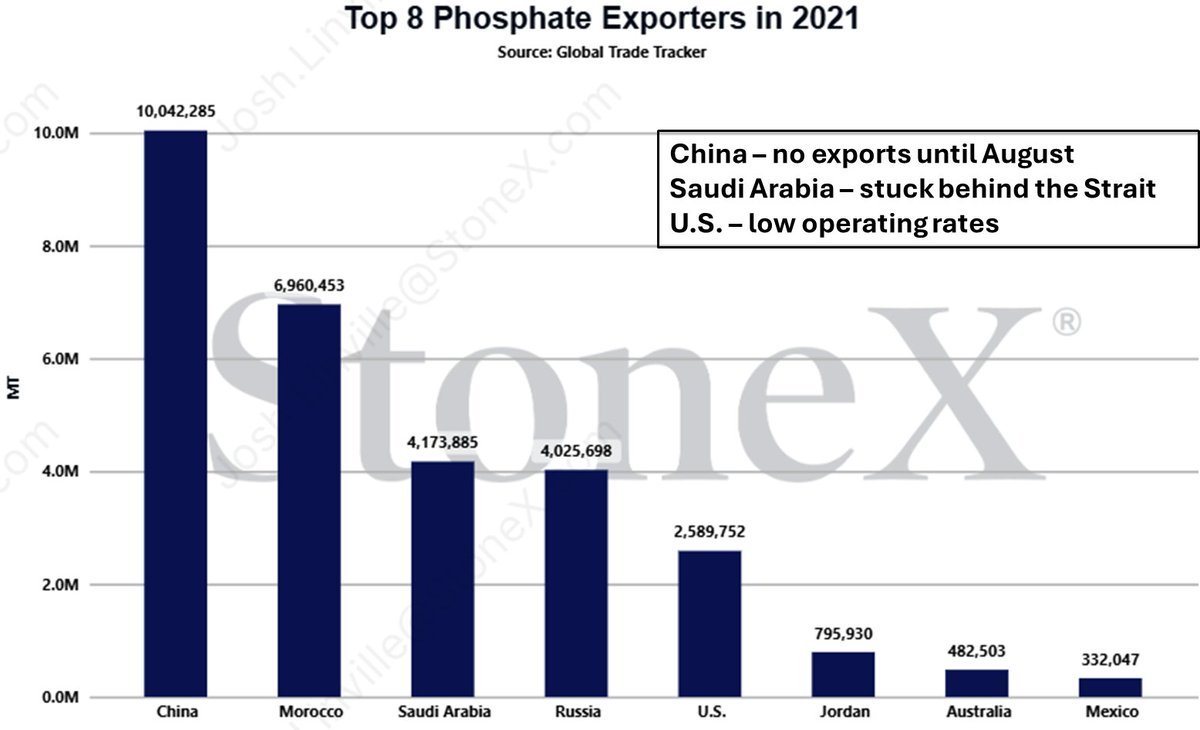

While the Middle East is a massive urea (N) producer, it also provides vital phosphate to the market. India, U.S., Brazil, and Australia rely heavily on this region for crop nutrients and in volumes that will be near impossible to replace. All of these fertilizers have to be moved by ship, and freight costs are hitting record highs.

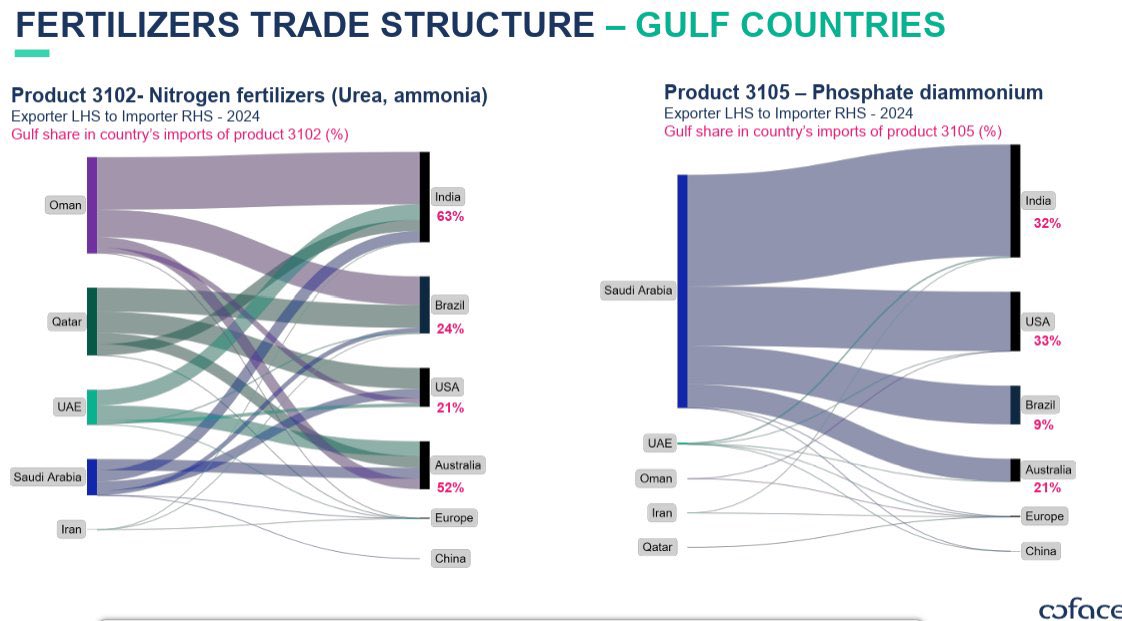

This doesn’t just go for fertilizer—grains are also not trading because of transportation costs. The below chart is a great way to break down flows between countries for nitrogen and phosphate.

While volumes are stuck, there will also be countries that “block” the export of a vital nutrient, which we’ve already seen out of China. Countries will focus on ensuring their own farmers have enough product and will likely horde volumes. This will really get the price of fertilizers going given the amount of urea exports available as represented in the chart.

I think it’s important to put these numbers into perspective with an example:

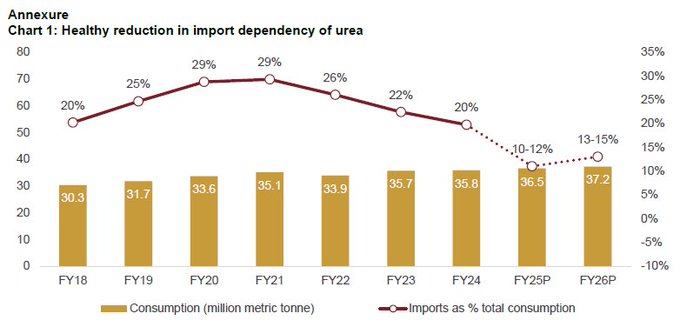

India consumes ~35–36M tons of urea annually, far above domestic production capacity of roughly 28–29M tons. This is what forces regular imports even though India is already one of the world’s largest producers of urea. But their internal production of urea is fed from the LNG that comes from the Middle East. Out of the 27M tons of LNG India imported last year, almost 19M came from the Middle East region, which puts a significant amount of their local production under pressure.

When we shift to supply, I use this chart to help provide color on where volumes can originate. Oman will likely be able to maintain some semblance of capacity, but Egypt had to shutter capacity last year driven by Israel shutting in natural gas production. The counter attacks from Iran could lead to broad disruptions that will reverberate through the system for months—if not several quarters—once missiles stop flying.

It’s important to highlight that turning these major facilities off and on isn’t like flipping a light switch. These are large facilities with their own complexities and intricate nuances that delay restarts. A lot of repairs that were made at the time of operation are fine while the facility is operational but may not withstand the stress of a restart. If the machinery isn’t turned off properly, there could be caking, clogged nozzles, or gear boxes filled with dust that hardened—the issues are endless on a restart. Once the missiles and drones stop flying, companies will need to clear storage while also bringing facilities back online. The hiccups on the restart will create another layer of delays across the board.

The current fears around availability are causing other countries to pause or “gate” exports of vital plant nutrients. China was already delaying exports until August, and they’ve now put an indefinite hold on all exports. The U.S. has some room for expansion after running at about 60% utilization rates, but it pales in comparison to what needs to be replaced. There will also likely be protective barriers put in place on our exports to ensure the U.S. farms have access to product.

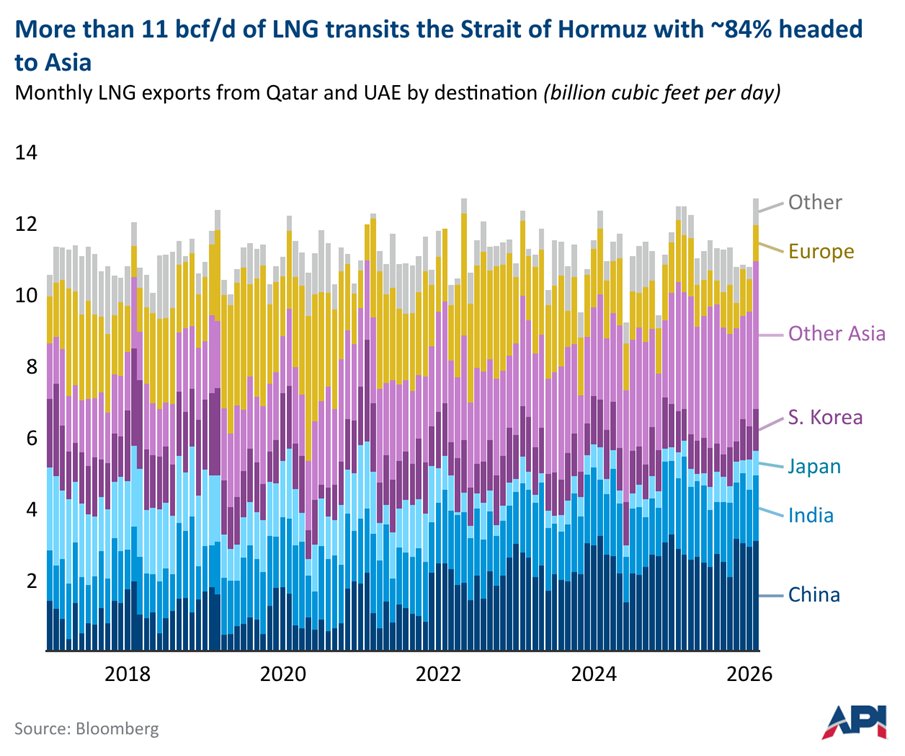

The key ingredient for the production of nitrogen is natural gas, and a large part of Asia and Europe source this important hydrocarbon from the Middle East. An estimated amount of 11BCF a day transits the Strait of Hormuz, with about 84% heading into the Asian markets. A growing number of shipments that were heading to Europe over the last week have changed course and are now sailing to Asia—the highest bidder.

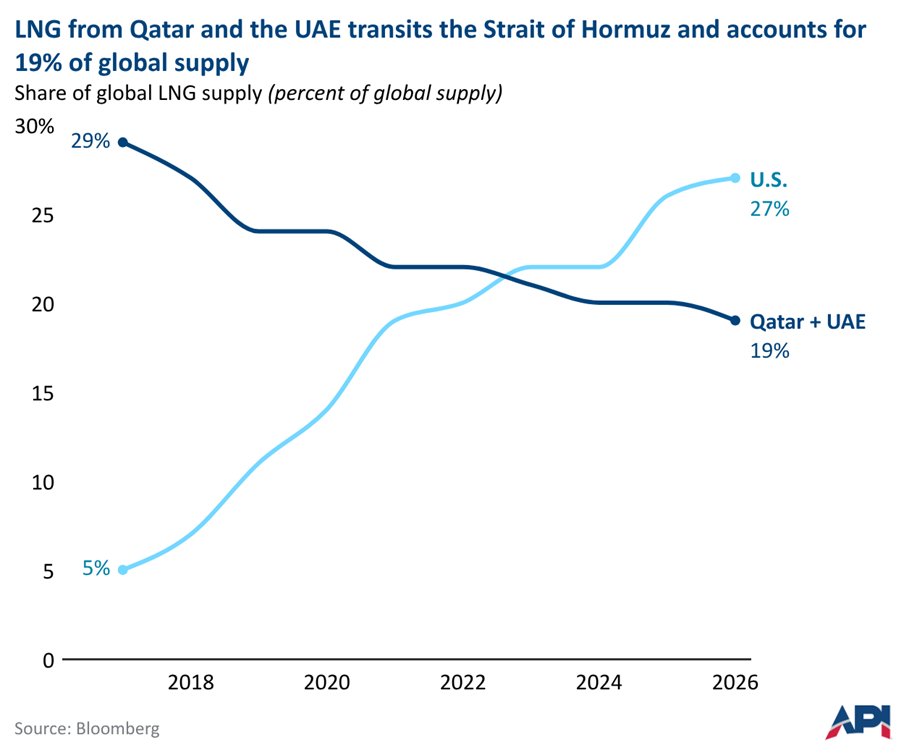

The U.S. has increased LNG production over the years, but Qatar and UAE were key sellers into the market. They are also a huge part of the expansion plan aimed to fill the growing demand expected over the next decade.

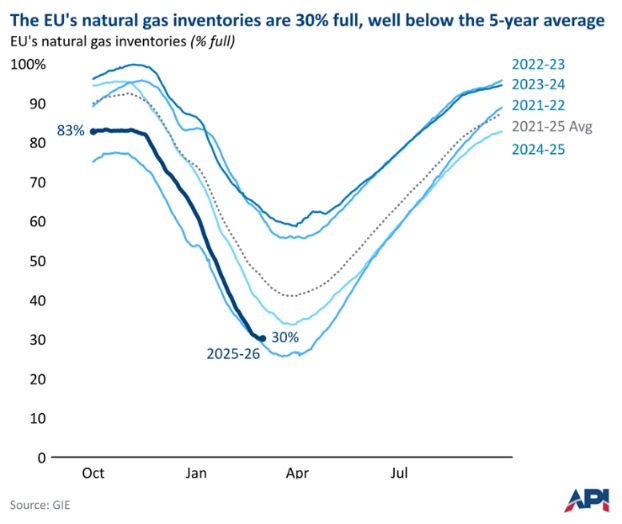

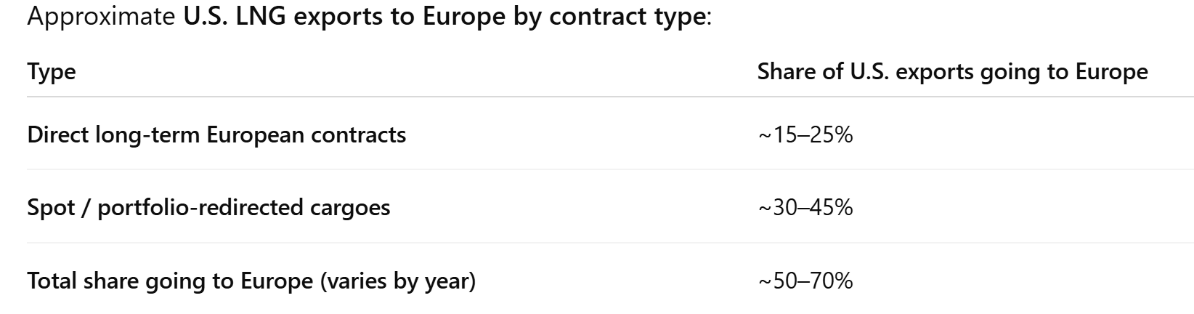

The U.S. sends a large part of their LNG to Europe, but unless it’s contracted, volumes can change direction and flow to the highest bidder. Driven by this year’s cold winter, Europe finds itself with depressed storage levels that only make the current situation worse. European natural gas inventories are currently ~30% full and near the bottom of the five-year range as the end of the heating season nears.

Europe only secured about 20%–25% of U.S. LNG on long-term offtake, with a large part of it being sold through spot or short-term contracts. This enables the U.S. to sell to the highest bidder, which will be Asia for the forseeable future.

One of the biggest losers will be the EU because they rely heavily on imports, especially since Russian gas flow fell significantly. Europe was already severely impacted following the Russian-Ukraine conflict, and now they are even more impacted given a large part of Middle East diesel and fertilizer flows into their markets. “Slovakia’s largest fertilizer producer said it’s curbing ammonia output after natural gas prices surged, in another sign that the Middle East conflict is starting to hit the industry in Europe.”[2]

Natural gas cannot be easily stored unless it’s kept in a salt cavern, so while countries may have oil and refined product storage measured in months, the same can’t be said about natural gas. So while China and India aren’t in the cross hairs, their LNG supply is directly impacted. Almost 84% of Qatar LNG flows into Asia, with over 26% flowing to China and 19% to India, so these countries will now be in direct competition with spot cargoes that normally flow into Europe. Everyone is going to compete on price and the highest bidder always wins. This will take supply from regions while driving up the price of goods around the world.

Sulphur is also a pivotal input for sulphuric acid, to make everything from petrochemicals to fertilizer to processed mined ore. About 47% of the world’s supply of sulphur originates in the Middle East, as well as 43% of urea, 27% of ammonia, and 24% of phosphate. Sultech provides a solution for the market by delivering sulphates to the soil WITHOUT the need for sulphuric acid. The company ships the product in its final form so a farmer can put it directly on the field. This reduces the cost significantly, while also providing sulphates throughout the whole growing season.

You might be thinking . . . why does that matter? Urea and AMS (Ammonia Sulphate) have a lot of complexity when it comes to application. Agriculture is a science that has very specific reactions in soil driven by weather, water consumption, composition, seed and plant formation, and crop type, among other things. This means that you can’t just spread urea or AMS whenever it becomes available. There are specific periods for application, and if you HAVE TO apply outside of that timeline, there are very strict rules to follow to avoid “burning” the root zone. A farmer can’t simply delay planting because the right amount of fertilizer isn’t available. Seeds have to be in the ground to maximize yield and emerge on time.

Sultech on the other hand, is COMPLETELY seed and plant safe because it has an osmotic pressure of ZERO. This means there’s NO RISK of burning the root zone or impacting plant growth. Sultech’s products are also much easier to ship than “bulk sulphur” because they can go into a hopper car, shipping container, rail car, flatbed truck, or bulk carrier. The current sulphur produced in the Middle East requires specialized loading facilities and boats for safe transit. One of the reasons ADNOC is so excited to work with Sultech is the flexibility for shipping our product. Sultech can ship on a freight container, flatbed truck, and hopper/freight rail car. We have a significant amount of flexibility driven by our 10% surface moisture, which creates a safe product. If we had our facility established in Abu Dhabi, Sultech would be able to rail or truck product to safer ports in the region, avoiding the current issues in the Strait of Hormuz.

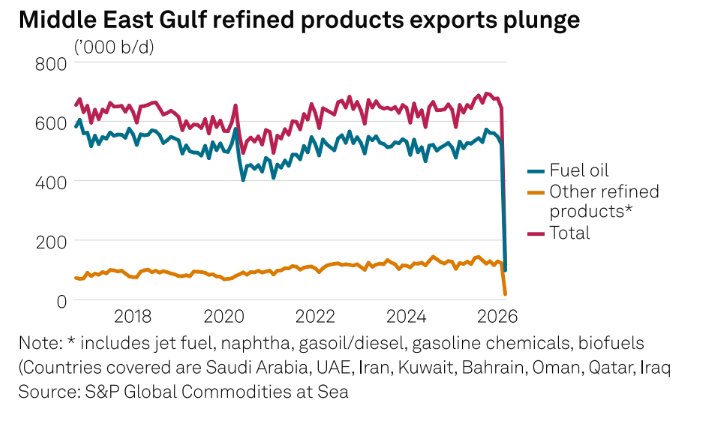

Sultech’s product can also be safely and cheaply stored for years, while urea and AMS are an absolute nightmare to store. These synthetic products require temperature and moisture controls and must be in well-ventilated areas with sealed bags. Farmers usually begin ordering their nitrogen needs at the beginning of the year to be delivered in March/April for application in May (ahead of seeding). Depending on the crop, soil composition, and region, it will be applied again throughout the growing season. Sultech’s product isn’t a replacement for nitrogen, but it is a pivotal nutrient for a healthy plant, optimizing the uptake of nitrogen. Another key component for a farmer is diesel—which has also been increasingly produced in the Middle East. Many GCC countries focused on constructing complex refiners to target a higher diesel cut—and they are all now stuck behind the Strait of Hormuz. The shift in diesel flows have pushed diesel prices to near record levels across the U.S., and we have barely started to see the beginning of the impact. For example, Florida's average diesel price has reached $5 per gallon for the first time since 2022, which is the 6th most expensive in the nation. The East Coast (especially the Southeast) is beholden to imports for diesel and gasoline (but diesel will impact the market the most at this point).

The issues with refined products will only get worse as more production is shut down across Iraq, UAE, Saudi Arabia, and Qatar. The first three nations provide pivotal grades of crude for heavy refining across the U.S., China, and India.

The agriculture world is shifting in rapid fashion given the loss of fertilizer, natural gas, and diesel coming from the Middle East region. It shouldn’t surprise anyone to see how food prices follow the value of refined products.

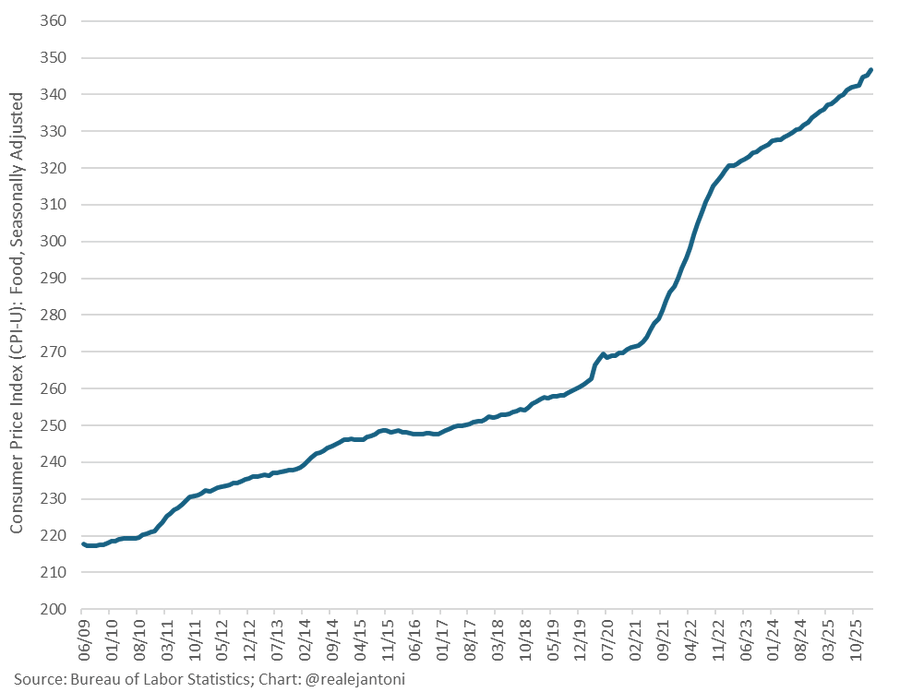

Food prices were already shifting higher even before the outbreak of war in the Middle East (see chart to the right – CPI Food Inflation). Prices are still rising at a fast pace—up 0.4% M/M (4.8% annualized) and 3.1% Y/Y. So while prices are increasing faster than their pre-pandemic rate, they're also up 34.2% from average price levels in 2019. The cost of farming inputs exploding does NOTHING to slow this movement higher.

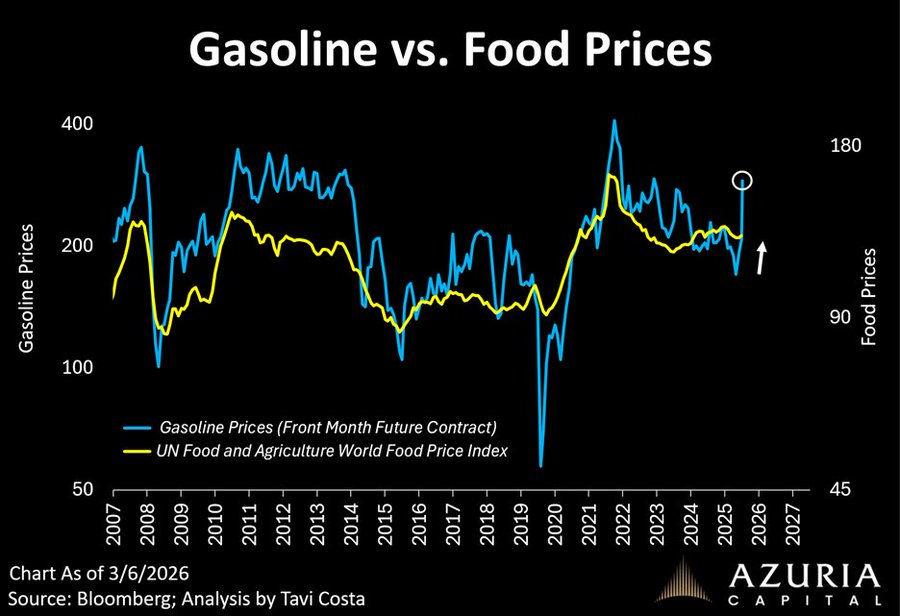

If we shift back to crude, you can see how food price indexes can shift rapidly. Prices have been on an upward trajectory for decades, but really went into overdrive during COVID. The rate of change might have slowed, but the trend has been relentless. I’m sure this is no surprise for anyone tracking their supermarket bills! Crop futures are just now starting to see a large shift higher, and given the timing of planting and fertilizer, none of this is going to happen quickly. Even if the war ends next month, Brazil—the largest fertilizer importer—won't restock in time for the next soybean planting. Farmers will attempt to recoup as much of their cost as possible, but we’re just at the tip of the spear for movements in fertilizer pricing.

CME's NOLA urea 10-ton contract update (product code - MFV) update:

- April: $631//$636 (traded 9 times at $617 earlier)

May - $594//$600 (traded 1 time at $595 earlier)

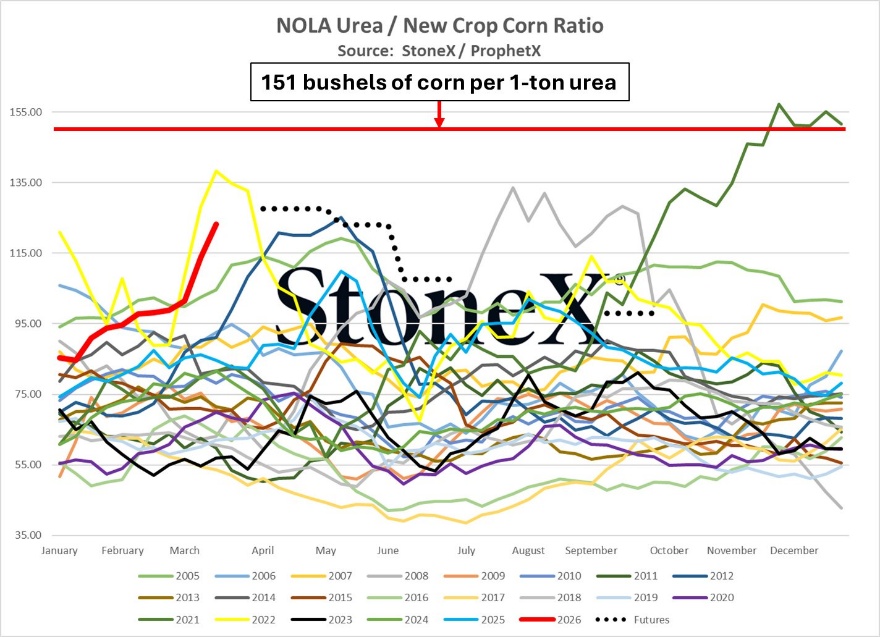

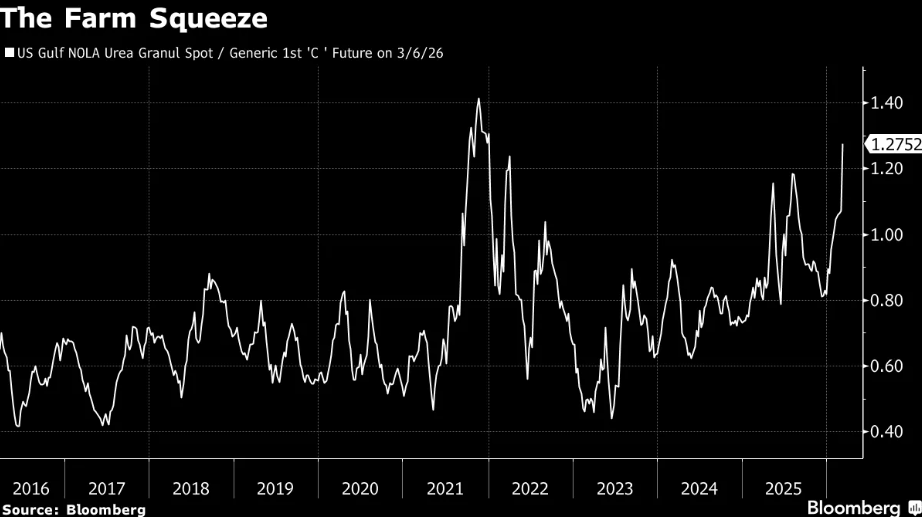

It’s likely we’ll see a sizeable uplift in pricing, but we’ve already been at the top of the cost curve when it comes to farming inputs. In December, it took 75 bushels of corn (Chicago price) to pay for 1-ton of NOLA urea. Today, it is taking 126 bushels of corn to pay for the same ton of NOLA urea: NOLA urea—up 77% or $270. Dec '26 corn is up 5% or 25 cents.

This urea chart shows how expensive fertilizer has been in relation to the price received by the farmer. We sit in a delicate balance to manage what comes next . . . global shortages. If NOLA urea were in line with current Middle East urea prices and current estimated vessel freight rates, the NOLA urea / Dec '26 corn ratio would be 151 bushels of corn per 1-ton NOLA urea. That would be 6 bushels away from setting the all-time high . . .

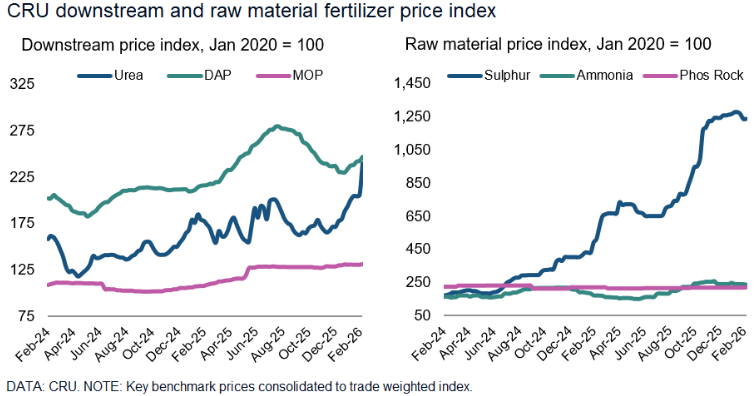

This CRU chart shows how raw materials for fertilizers have shifted higher, and this will keep pushing prices higher. It’s important to mention that prices have been shifting higher since the end of the year, and the current conflict is just exacerbating an already growing problem.

As we saw during the early days of the Russian invasion of Ukraine, urea costs exploded, yet we didn’t lose as much supply. Now, we still don’t have the same level of Russian product while supply disruptions expand around the world. It’s fair to assume that prices will take out those Russian conflict highs. We’re still in the early stages of urea facilities cutting runs with Slovakia’s Duslo, the first of others to follow.

C6 has focused on food and fertilizer since inception, with countless YouTube shows and podcasts discussing the issues. Here’s a broad sample: https://www.youtube.com/@PrimaryVisionNetwork/search?query=food

We’ve actively looked for solutions that were cheaper and more effective than the incumbent products, especially ones that aren’t synthetic. Sultech’s products are a beautiful, elegant nutrient that deliver sulphates through the WHOLE growing season at a fraction of the cost to current options. Does Sultech replace the need for nitrogen or phosphate? No. BUT it optimizes what is currently in the ground or what a farmer adds to the field. It allows for flexibility and a diversified supply chain that offers a farmer optionality + huge cost savings. The agriculture community needs solutions that replace or reduce the amount of synthetic fertilizers, but they also need ways to improve soil health. Luckily, Sultech delivers both solutions in their products, depending on run rates.

C6 is committed to finding long-term solutions to today’s problems. Iran and the Strait of Hormuz are now shining a bright light on what we’ve been predicting for a decade.