Articles

- BLOG / Articles / View

- Articles

Mapping U.S. Shale Resilience: Latest Projects

By Avik on January 7, 2026 in Articles

Inside the Shale Build-Out: What Today’s Projects Say

Following up with Primary Vision’s breakeven series, here, we peeked at the select operators’ shale basin projects to get an idea of who is running ahead and who lags. In the context of fracking, we have explained the break-even prices here. We discussed the significance of the BE prices for some major US energy producers. We even did scenario analysis, assuming a fall in oil price or a move towards lower-tier acreages. Against a breakeven backdrop that turns punitive below $55 crude and under a 20% cost inflation scenario, the new wave of U.S. shale projects puts Exxon, EOG, and ConocoPhillips in the strongest starting position. Chevron remains exposed to the same core basins.

In contrast, the more concentrated footprints at Crescent and Riley leave little room to absorb stress, while Talos’ offshore slate sits outside shale economics. Here is a summary of their US shale basin projects and their implications.

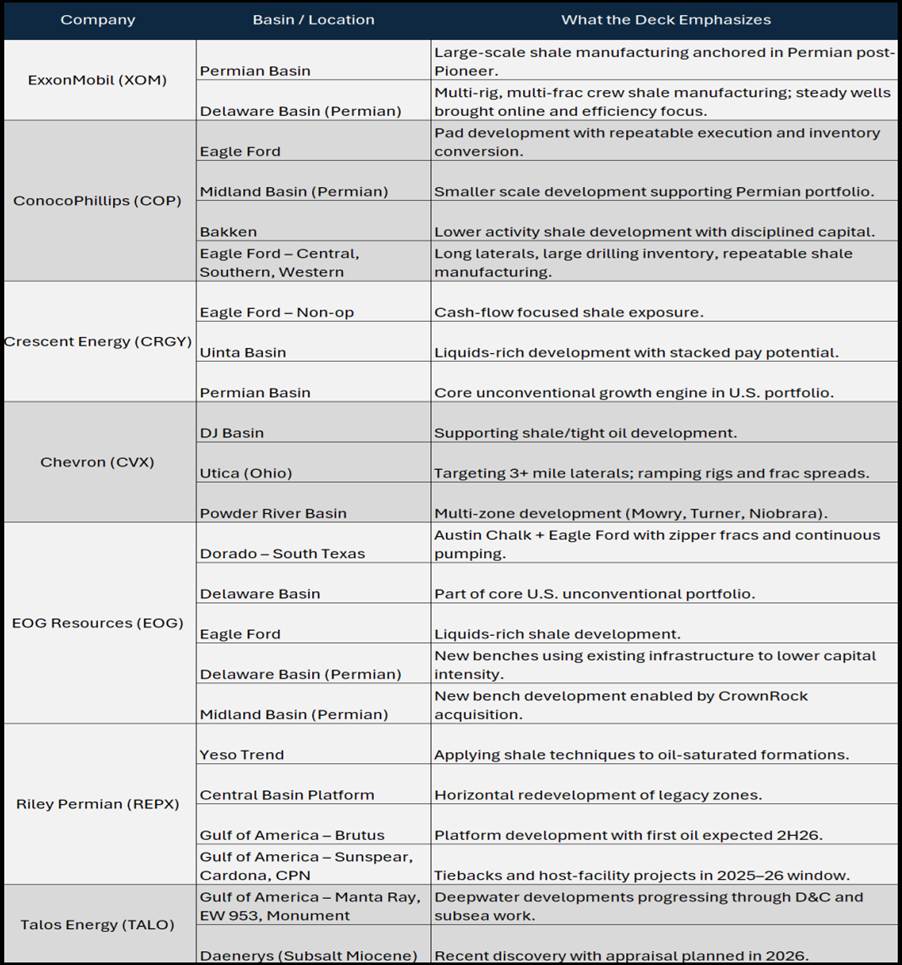

Top Posts – XOM, CVX, COP, EOG

ExxonMobil (XOM): Exxon’s story is scale in the Permian. The basin has become a core unconventional engine post-Pioneer, with manufacturing-style development and integration across a massive footprint. Expect steady, high-volume shale execution and cost leverage. I think Exxon is best positioned on scale and durability, not agility.

Chevron (CVX): Chevron also centers on the Permian, with DJ as a secondary asset. The presentation is high level, but the intent is clear: keep shale disciplined and repeatable. Expect stable development rather than aggressive ramp-ups. I think Chevron is well placed, but the project visibility looks thinner than Exxon’s.

ConocoPhillips (COP): COP runs multiple shale programs — Delaware, Eagle Ford, Midland, and Bakken — with clear emphasis on manufacturing efficiency and steady wells brought online. This gives flexibility across basins and inventory depth. I think COP is better placed than CVX on portfolio breadth, even if it lacks Exxon’s sheer scale.

EOG Resources (EOG): EOG’s article is the most operationally detailed: long laterals in Utica, stacked-pay PRB development, Dorado gas co-development, plus core Delaware and Eagle Ford oil. Expect technical optimization and capital efficiency to drive outcomes. I think EOG is best positioned on well quality and execution, even if it doesn’t match majors on size.

Crescent Energy (CRGY): CRGY is all about Eagle Ford manufacturing with long laterals and a repeatable inventory, plus Uinta as a secondary lever. Expect steady, cash-driven development rather than growth. I think CRGY is solidly positioned for returns, but its basin concentration limits upside versus Permian-heavy peers.

Riley Permian (REPX): Riley is a focused Permian developer across Delaware, Yeso, and CBP using modern horizontals. Expect small-cap style execution: steady well cadence and niche development. I think REPX is well placed within its scale, but it lacks diversification and balance-sheet depth versus larger peers.

Talos Energy (TALO): Talos is offshore. Its projects are deepwater developments and appraisal wells in the Gulf of America, not shale. Expect project-driven volume steps tied to first oil milestones. I think TALO sits outside this shale comparison — it’s a different risk-return profile altogether.

Breakeven and Low Oil Price Implications

Looking at the project map through this breakeven lens, the Permian-heavy and diversified slates at Exxon, EOG, and ConocoPhillips leave them best placed to sustain selective drilling while protecting base production. Their scale and core basin exposure mean new projects can still clear near half-cycle thresholds, even as capital tightens.

Chevron retains resilience from integration, but its narrower shale project set implies quicker discipline if margins compress. Crescent and Riley would shift into preservation mode, while Talos’ offshore slate remains vulnerable to project deferrals rather than shale-style resilience.

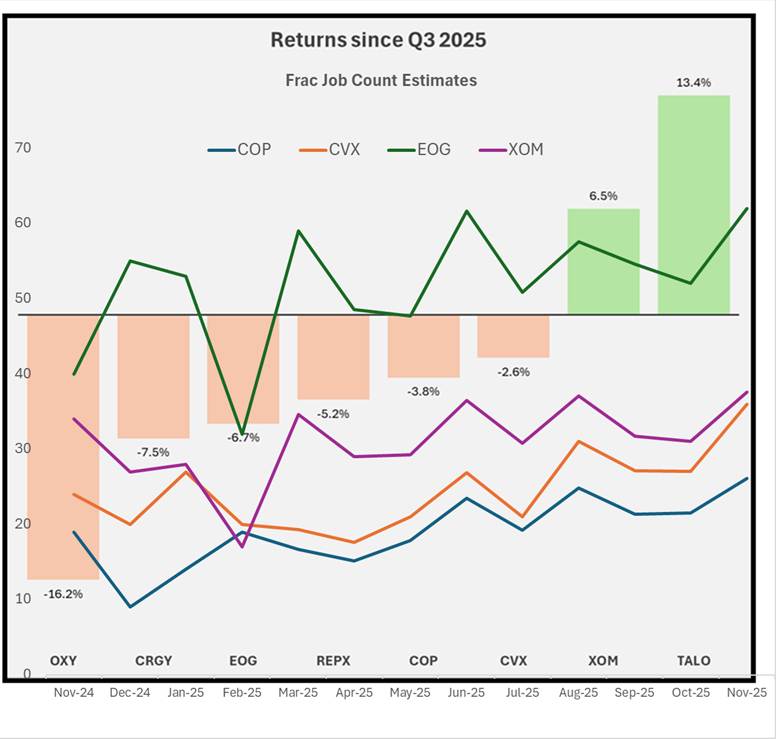

What Do Frac Job Counts Say?

From September to November 2025, frac activity steps up sharply across all majors, with the biggest absolute lifts at EOG, Exxon, and Chevron, and solid gains at Conoco as well. This broad November jump suggests operators were still leaning into core projects while prices held up, prioritizing Tier-1 Permian and premium shale inventory. In the context of the breakeven analysis, it indicates that once crude slips toward the low-$50s or costs rise, this level of activity would be hard to sustain, even for the lowest-cost names.

Investors’ reactions can be a guiding point to separate the wheat from the chaff. While most of the stocks from our list posted negative returns, CRGY saw the steepest dip. XOM and TALO were the only names to post gains. While other factors influenced prices, Exxon’s Permian-centric refocus could have influenced investors’ choices.

Takeaway

Putting the project map through both stress tests, the message is clear: in a $50–55 crude world or under rising cost pressure, only operators with core Permian exposure and diversified shale depth can defend activity. I think Exxon, EOG, and ConocoPhillips are best positioned to sustain production and selectively fund new wells, even as full-cycle economics turn challenging.

Chevron should hold steady but lean conservative. However, Crescent and Riley are likely forced into preservation mode, and Talos faces offshore deferrals rather than shale slowdowns. The next downturn, if it comes, won’t just test balance sheets — it will separate basin quality and project resilience from everything else.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform