Market Sentiment Tracker: How the Hormuz shock split the world's central banks

By

Osama

on May 26, 2026

in

Market Sentiment

This week, I'm watching the growing split between the Fed and the ECB — and what it means for every other central bank on the planet.

Kevin Warsh took over as Fed Chair on May 15. Five days later, the minutes from Powell's final FOMC meeting revealed four dissents — the highest number since 1992. The committee is split three ways: hawks who want hikes on the table, a minority pushing for cuts, and a cautious centre that voted to hold at 3.50–3.75%. At the same time, Bloomberg's latest survey confirmed the ECB will likely hike rates twice this year, in June and September. The Fed and ECB are now responding to the same oil shock — Brent still volatile around $98, the Strait of Hormuz still effectively restricted — in opposite directions. The rate gap sits at 160 basis points and is set to widen. What makes this divergence unusual compared to 2015–2018, when the Fed hiked while the ECB eased, is that both central banks are reacting to the same supply shock rather than different domestic cycles. The Hormuz crisis is producing sticky inflation in Europe through energy import dependence, while in the US it's draining crude inventories (down 7.86M barrels this week, triple expectations) without yet feeding through to consumer prices at the same pace.

This week's data explains why each central bank thinks it's right. In the US, the economy looks strong enough to justify holding: GDPNow tracking 4.3% for Q2, housing starts beating at 1.465M, jobless claims steady at 209K. But the Philly Fed manufacturing index dropped from +26.7 to -0.4 in a single month, with new orders turning negative — the steepest decline since the 2020 lockdowns. The manufacturing sector is telling a different story than the aggregate numbers, and Warsh has to decide which signal to trust before his first meeting on June 16. The 20-year Treasury auction clearing at 5.122% suggests bond investors aren't confident he'll get the answer right.

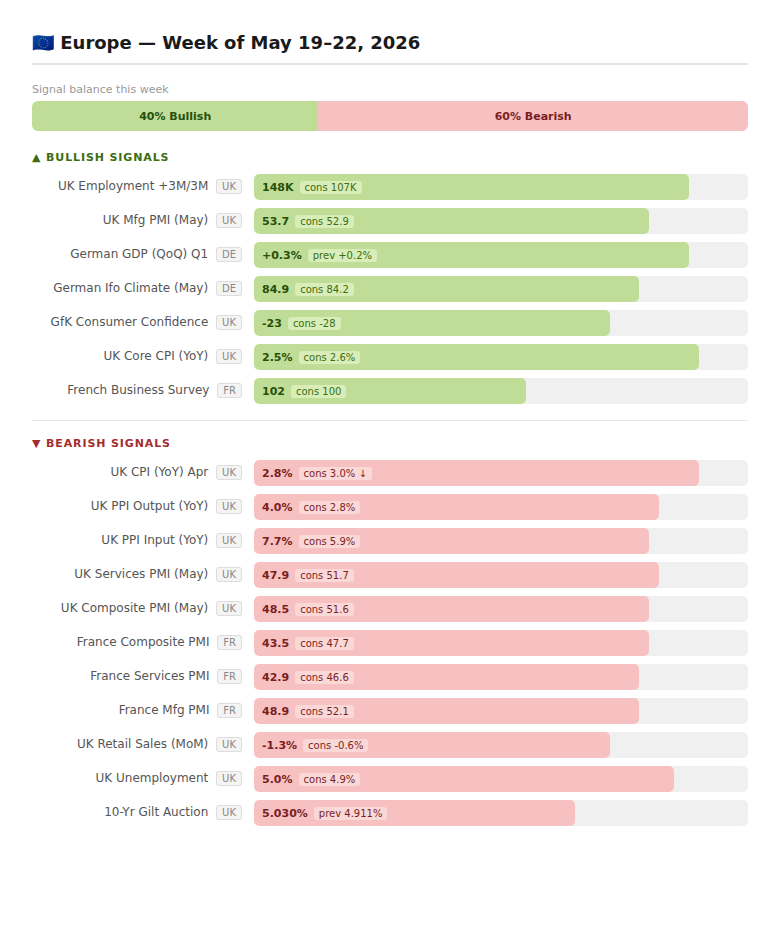

In Europe, the inflation data leaves the ECB with limited options. UK input PPI came in at 7.7% year-on-year, nearly two points above expectations, and output PPI hit 4.0% against 2.8% consensus — clear evidence that energy costs are passing through to end prices. Eurozone headline inflation reached 3.0% in April. Lagarde has already signalled publicly that the ECB will act even if the inflation overshoot proves temporary, partly because allowing prices to rise unchecked would undermine the bank's credibility. The problem is that the economies receiving these hikes are already weakening. France's composite PMI printed 43.5, deep in contraction and four points below consensus. The UK composite fell to 48.5. Rate hikes will tighten financial conditions further in economies where demand is already falling — without addressing the supply-side energy costs driving inflation in the first place.

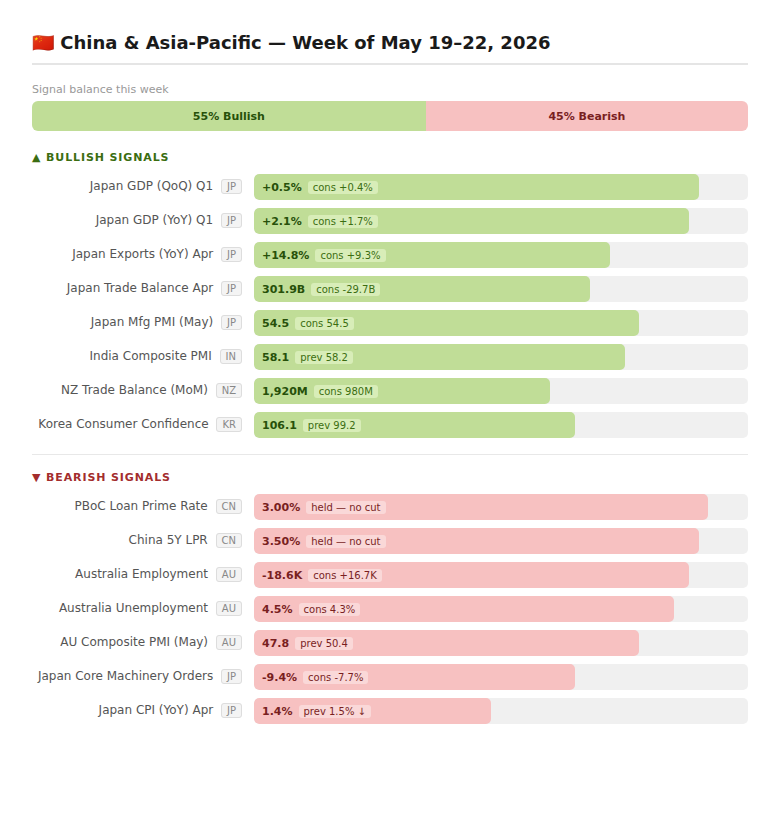

Asia-Pacific is absorbing the consequences of both positions. Beijing held both loan prime rates unchanged this week, and the logic is straightforward: with the Fed at 3.50% and US long-end yields above 5%, cutting rates would widen the interest rate differential and accelerate capital outflows at a moment when yuan stability matters. The PBoC is effectively constrained by the Fed's stance. Japan, meanwhile, is benefiting from the disruption — exports surged 14.8% year-on-year as redirected trade flows and a weak yen combined to produce a surprise trade surplus. But even there, the picture is uneven: machinery orders collapsed 9.4% as Japanese firms sit on export earnings rather than reinvest them domestically. Australia's labour market lost 18.6K jobs against expectations for a gain, suggesting the RBA's hawkish posture has already overtightened.

Every central bank is watching the other two. The Fed can't ease because inflation won't cooperate. The ECB feels compelled to hike because credibility demands it. The PBoC can't move because the Fed won't. Warsh's first decision is in three weeks. So is the ECB's expected hike. What happens in June will determine whether this divergence holds — or snaps.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform

.png)