Market Sentiment Tracker: Why Is a Falling Jobless Rate Making the Fed's Job Harder?

By

Osama

on July 7, 2026

in

Market Sentiment

This week's calendar carried three of the releases that actually move policy — U.S. payrolls, eurozone PMIs and CPI, and China's manufacturing and services gauges — alongside a long tail of second-tier prints, sovereign auctions, and central bank speeches that mostly just filled in the edges. The three headline reads landed on the same days investors had been positioning for, which means whatever came out was always going to move the conversation on rate paths, not just sit there as data.

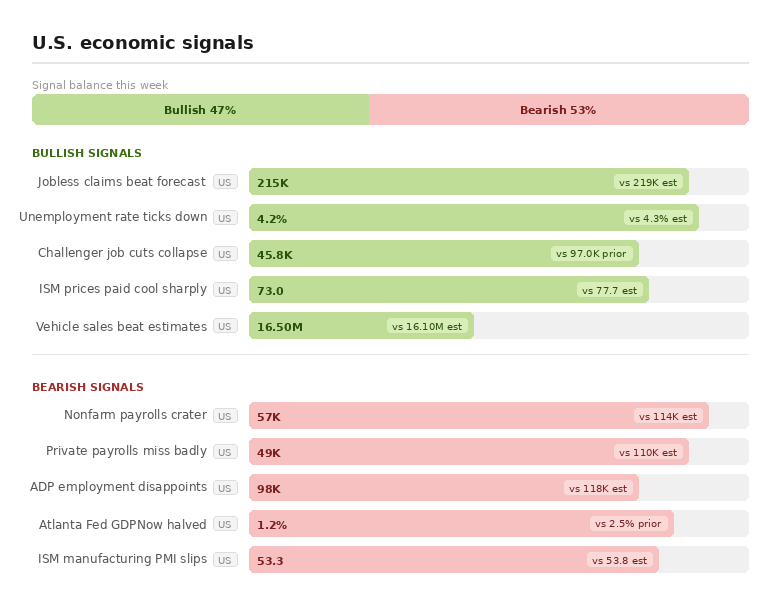

Start with what the U.S. jobs data actually does to the Fed's decision, not just what it says. A payrolls print of 57K against a 114K consensus, backed up by a private payrolls miss at 49K and an ADP number that had already flagged the same softness a day earlier, pulls forward the timeline for rate cuts almost automatically — three independent gauges missing the same direction is the kind of confirmation that moves a committee, not just a headline. But the unemployment rate falling to 4.2% complicates that story rather than supporting it, because participation fell at the same time, from 61.8% to 61.5%. That matters because the improvement isn't coming from hiring, it's coming from people leaving the labor force altogether, and a labor market that shrinks rather than absorbs workers doesn't necessarily relieve wage pressure the way a genuine slowdown would. That's the awkward setup the Fed now has to price: real signs of a cooling job market alongside a labor supply contraction that could keep wage growth stickier than the payrolls miss implies — exactly the kind of ambiguity that makes a September cut a coin flip rather than a formality. The Atlanta Fed's GDPNow getting cut in half, from 2.5% to 1.2%, is the market pricing that ambiguity into growth expectations before the Fed even meets.

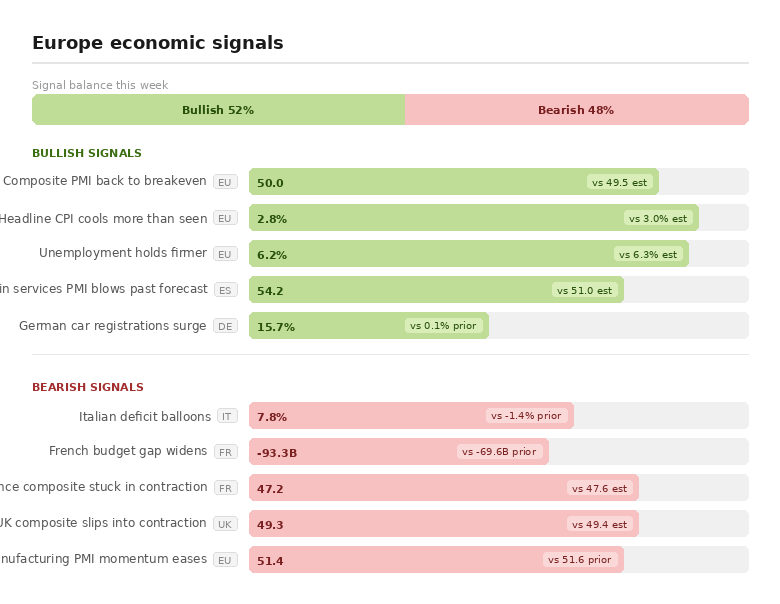

Europe's numbers point somewhere more interesting than "recovery" or "stagnation" — they point toward a policy bind. The composite PMI clearing 50.0 for the first time in this run gives the ECB room to hold rates rather than cut further, especially with inflation cooling to 2.8% against a 3.0% consensus. But that's precisely the wrong moment for Italy's deficit to swing to 7.8% of GDP and France's budget gap to widen to -93.3B, because a central bank that isn't cutting doesn't ease the refinancing pressure building under two of the bloc's largest sovereigns. If growth data keeps improving even modestly, the ECB has less cover to look past the fiscal slippage, which raises the odds that bond markets start repricing peripheral spreads before politicians are forced to act on their own. Germany beating consensus while France's composite stays below 50 isn't just a growth divergence — it's the reason any single ECB policy setting will chronically fit one economy better than the other, and it's why Italy's fiscal deterioration carries more market risk now than it would if the whole bloc were still visibly struggling together.

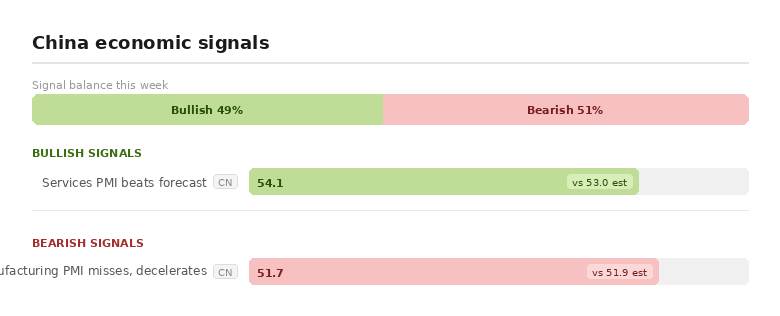

China's split between decelerating manufacturing and resilient services isn't neutral for the rest of the world — it's a signal about where Chinese demand is and isn't showing up. A fourth straight month of factory momentum slipping, even while staying above the expansion line, means the export and industrial-input demand trading partners have been counting on is fading gradually rather than snapping, which is harder for policymakers to justify responding to with major stimulus. Services holding up means the domestic consumer isn't collapsing, which removes the urgency case for a large policy response even as the manufacturing side keeps softening. The practical result is a government more likely to lean on small, targeted support than a broad stimulus push — and a global manufacturing sector that shouldn't expect the usual lift from Chinese industrial demand heading into the third quarter.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform