Monday Macro View: Spreads Are Up and Shale Executives Are Running Out of Reasons to Wait

By

Osama

on April 27, 2026

in

Market Sentiment

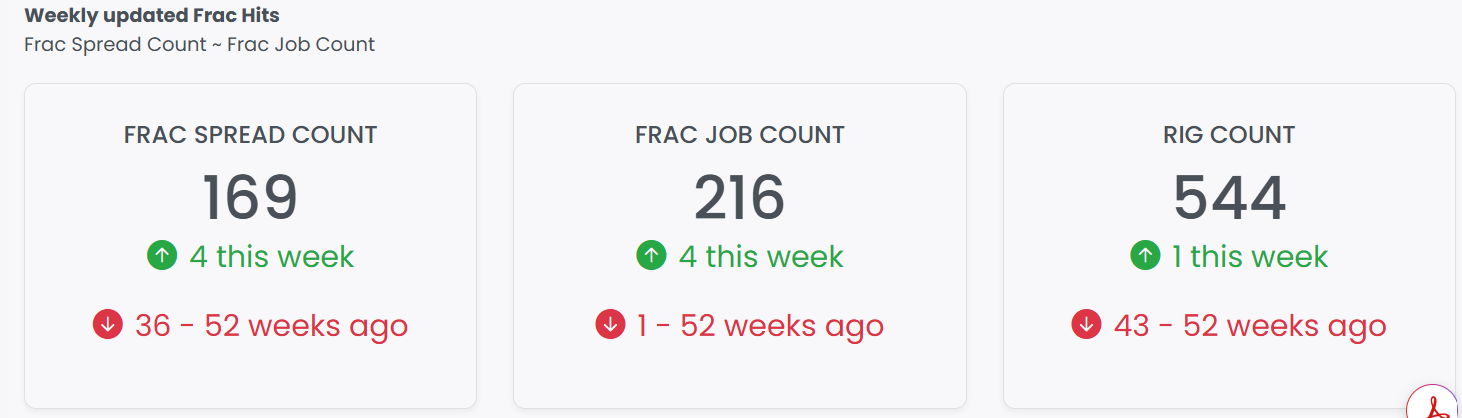

The latest Primary Vision data confirms what the broader directional trend was already suggesting: last week's modest pullback in completion activity was a data point, not a pattern. Frac Spread Count rose by four spreads to 169, and Frac Job Count added an identical four jobs to reach 216. Both indicators are moving in the same direction, at the same pace, which is a meaningful signal. When we flagged last week that a single week of softness did not constitute a trend reversal, this week's reading validates that view. The recovery in both FSC and FJC is continuing.

What gives us additional confidence in the trajectory is the pricing environment. Oil prices have remained elevated and, given the ongoing supply disruption from Strait of Hormuz closures, there is a credible case that higher prices persist into the medium term. Completion activity follows economics, and when prices stay high, utilization of spreads and crews does not retreat quietly. Our historical data suggests that sustained activity gains become more meaningful when prices hold in an elevated range for at least three consecutive months. We are not there yet, but if current price levels hold through the summer, the conditions for a more durable step-up in FSC and FJC will be in place. We expect both indicators to continue their recovery in the weeks ahead, barring a significant shift in the pricing regime.

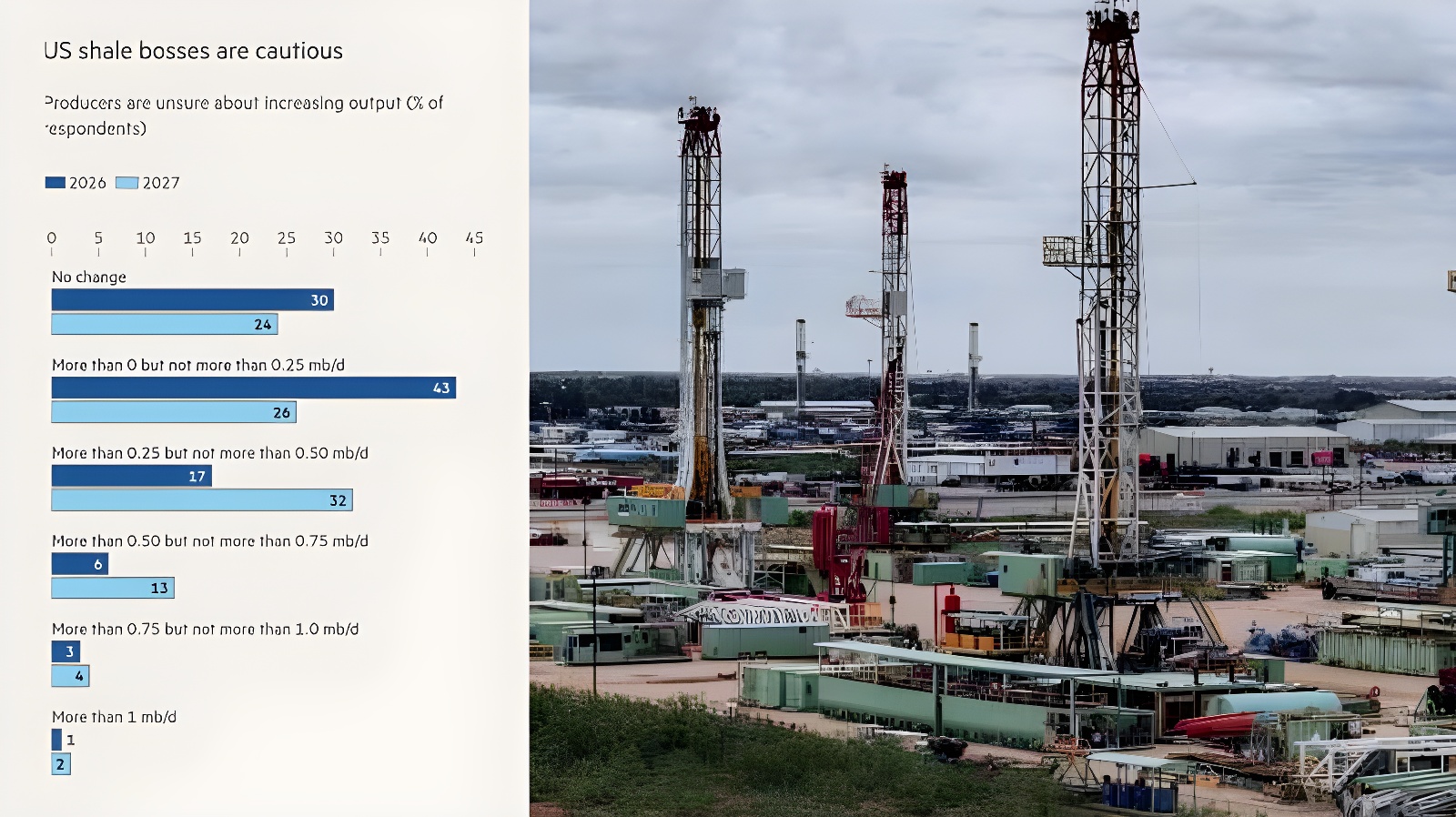

On the wider US market, the picture is more complex. The Dallas Fed's latest quarterly survey of more than 100 oil and gas executives reveals a striking degree of restraint. Roughly 43% of respondents said they do not expect daily production to grow by more than 250,000 barrels per day in 2026. For 2027, 32% projected growth in the 250,000 to 500,000 bpd range. These are modest numbers in the context of a global supply dislocation that has seen the Strait of Hormuz effectively closed to normal shipping.

It is worth being precise about what the survey does and does not tell us. Executives saying they do not plan to significantly increase production is not the same as saying production will fall. Current output levels are expected to be maintained; the restraint is on the expansion side. That distinction matters for how we read the supply picture: US production is not a source of downward pressure, it is simply not acting as the rapid relief valve some have hoped for. The survey comments are instructive. Executives cited the difficulty of planning capital budgets in an environment where paper market prices and physical crude prices are diverging sharply. One noted that price swings driven by headlines are enough to disrupt rig and budget decisions. Most companies are taking a wait-and-see approach to their 2026 budgets. To read more on the financials, please check out our Take Three series.

JPMorgan's commodities team has flagged that physical crude stockouts are already suppressing demand in vulnerable markets across the Middle East, Asia, and Africa, which have absorbed around 87% of the supply reduction so far. But the demand destruction scenario will also depend on multiple factors such as dollar exchange, oil prices and overall market sentiment. As spare capacity in Saudi Arabia and the UAE remains difficult to activate quickly , and as shale executives hold back on capital commitments, the gap between supply and demand seems a bit intimidating in the shorter run. But on a longer run things look different. Wait for this week's free read that will focus on how many barrels have been lost and if the current scenario regarding an impending supply shock is exaggerated.

At Primary Vision, we remain constructively bullish on the industry's trajectory, and this week's FSC and FJC data supports that posture. The Dallas Fed survey reflects rational caution, not pessimism, and the distinction between restraint on growth and an actual production decline is one the market should keep in mind. That restraint, combined with a constrained global supply environment, supports prices remaining higher for longer, which in turn should continue to pull completion activity upward. The data and the fundamentals are, for now, pointing in the same direction.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform