Articles

- BLOG / Articles / View

- Articles

Monday Macro View: The Shale Race Is No Longer a One-Basin Story

By Osama on May 25, 2026 in Market Sentiment

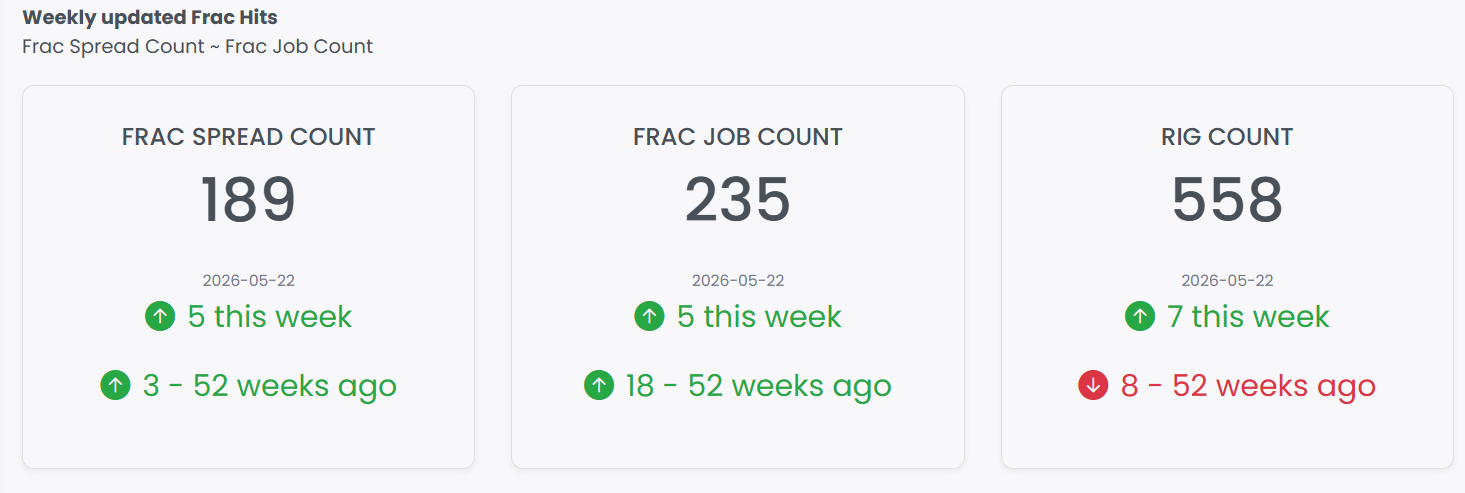

Before we turn to this week's macro focus on Vaca Muerta, the U.S. completion picture deserves its own read. The FSC came in at 189, up 5 from last week, while the FJC registered 235, also up 5 week-over-week. The rig count rose 7 to 558. All three indicators moved higher in the same week, a coordinated uptick that has been uncommon in 2026 and arrives against the backdrop of WTI hovering near $100 on Hormuz-related supply anxiety. Both the FSC and FJC sit above their year-ago levels, by 3 and 18 respectively, though the rig count remains 8 below where it stood 52 weeks ago. That divergence between completion activity and drilling tells a familiar story of operators leaning into their drilled-but-uncompleted inventory rather than committing new iron to the ground, a posture consistent with capital discipline but one that cannot persist indefinitely if prices stay at these levels.

Primary Vision has long noted that sustained, meaningful gains in U.S. completion activity tend to require prices holding in an elevated range for roughly three consecutive months. With WTI trading near $100 per barrel amid Strait of Hormuz disruptions, that threshold has been met and then some. Yet U.S. operators remain disciplined. Argentina's operators are not waiting. According to UPI reporting on government data, Argentina reached record oil production of 874,000 barrels per day in February 2026, a 15.9% year-over-year increase driven almost entirely by unconventional output from Vaca Muerta. The EIA estimates the formation holds 16 billion barrels of technically recoverable shale oil and 308 trillion cubic feet of shale gas, making it the world's fourth-largest shale oil reserve and second-largest for gas.

The most significant development this week is the 15-block licensing round launched by Neuquén's provincial energy authority, Gas y Petróleo del Neuquén. It is the largest Vaca Muerta auction since 2016 and more than double the six blocks offered in the prior provincial round. Bidders will compete on a combination of royalties above the 15% statutory minimum, work program commitments, and access bonuses with a $500,000 per-block floor. The round covers northwest condensate zones, northeast oil-focused acreage, and southrn frontier exploration areas. Chevron and Shell joined the Vaca Muerta Sur pipeline consortium alongside YPF, Vista Energy, Pampa Energía, and Pan American Sur. That 437-kilometer pipeline to the Atlantic coast port at Punta Colorada will carry 180,000 barrels per day at initial service in late 2026, scaling to 550,000 by 2027, with capacity for 700,000 barrels per day thereafter.

A critical nuance that surface-level coverage often misses: Vaca Muerta's geology is genuinely exceptional, not simply "promising." Formations as 100 to 400 meters thick, spanning 30,000 square kilometers, with porosity of 10 to 20 percent, up to eight landing zones, and total organic content averaging 5%. That thickness is two to four times what operators encounter in core Permian intervals. Industry reporting places breakeven costs between $36 and $45 per barrel, comfortably below the current price environment and competitive with mature U.S. plays. Yet only roughly 8% of the formation is under active development, with 4,470 active wells across the basin.

The policy architecture underpinning this expansion matters as much as the geology. President Milei's RIGI framework, the Régimen de Incentivo para Grandes Inversiones, provides 30-year fiscal stability on tax, customs, and foreign exchange terms for qualifying projects. As per the recent developments, $17.9 billion in RIGI filings have been approved, with billions more pending. YPF alone filed a $25 billion application. The EIA's December STEO forecast that Brazil, Guyana, and Argentina would account for half a million barrels per day of global crude production growth in 2026, with Argentina among the key non-OPEC contributors. Hydrocarbon investment in Argentina for 2026 is expected to reach $11 billion, a 17% increase over the prior year.

Primary Vision maintains its constructively bullish posture on U.S. completion activity, and this week's Vaca Muerta focus reinforces rather than undermines that view. The global supply picture is being reshaped by non-OPEC growth from multiple basins simultaneously, which in an elevated price environment supports sustained activity rather than displacing it. The FSC and FJC levels reflect a market that is expanding domestically, while Argentina's acceleration from 45,000 barrels per day a decade ago to nearly 900,000 today demonstrates what happens when geology, capital, and policy alignment converge. The question for U.S. operators is not whether Vaca Muerta competes with the Permian, but whether the global market is large enough for both to grow. At current prices and demand projections, the data suggests it is.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform