Articles

- BLOG / Articles / View

- Articles

Monday Macro View: When Are the Gulf's Missing Barrels Coming Back?

By Osama on June 15, 2026 in Market Sentiment

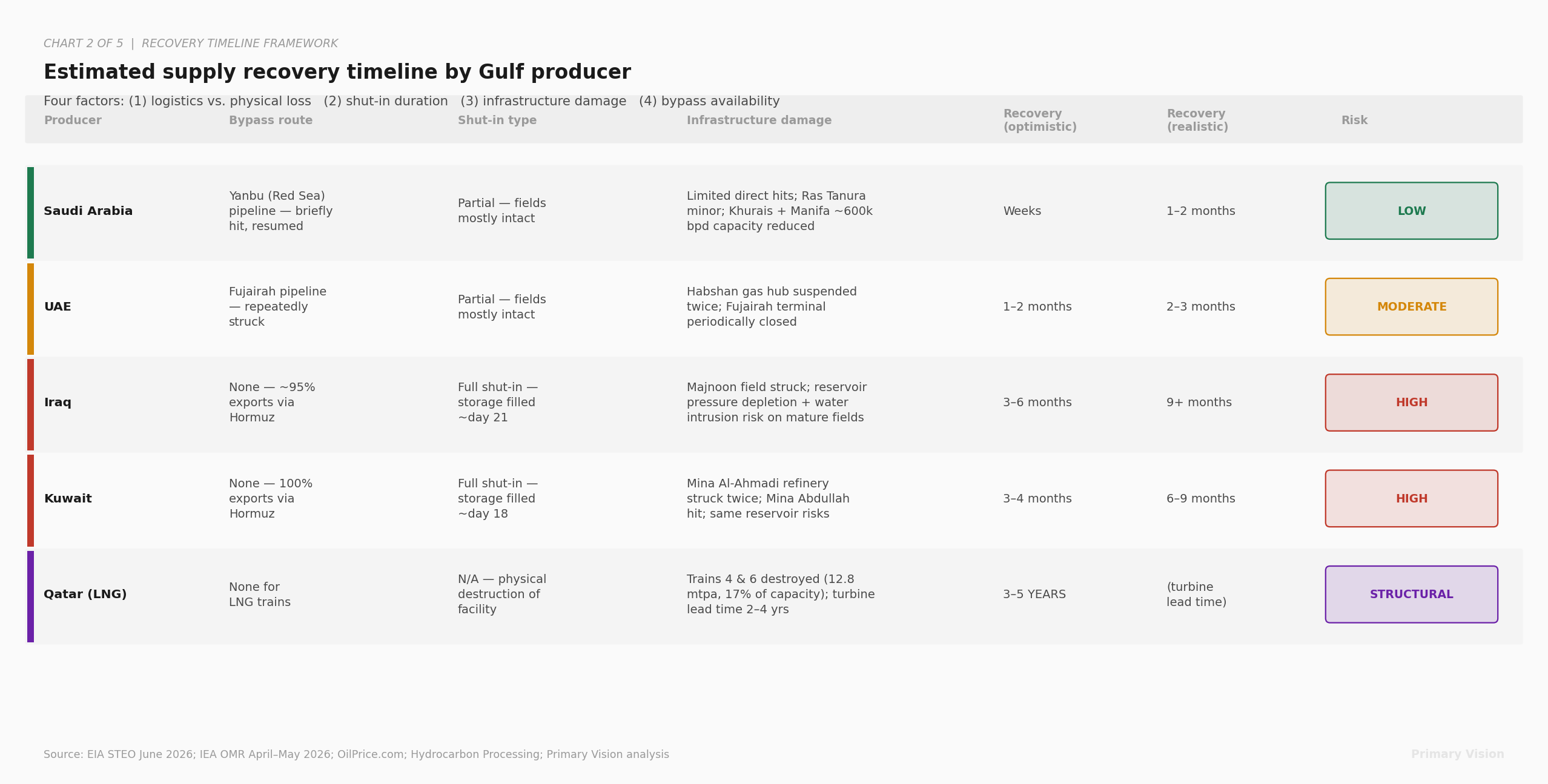

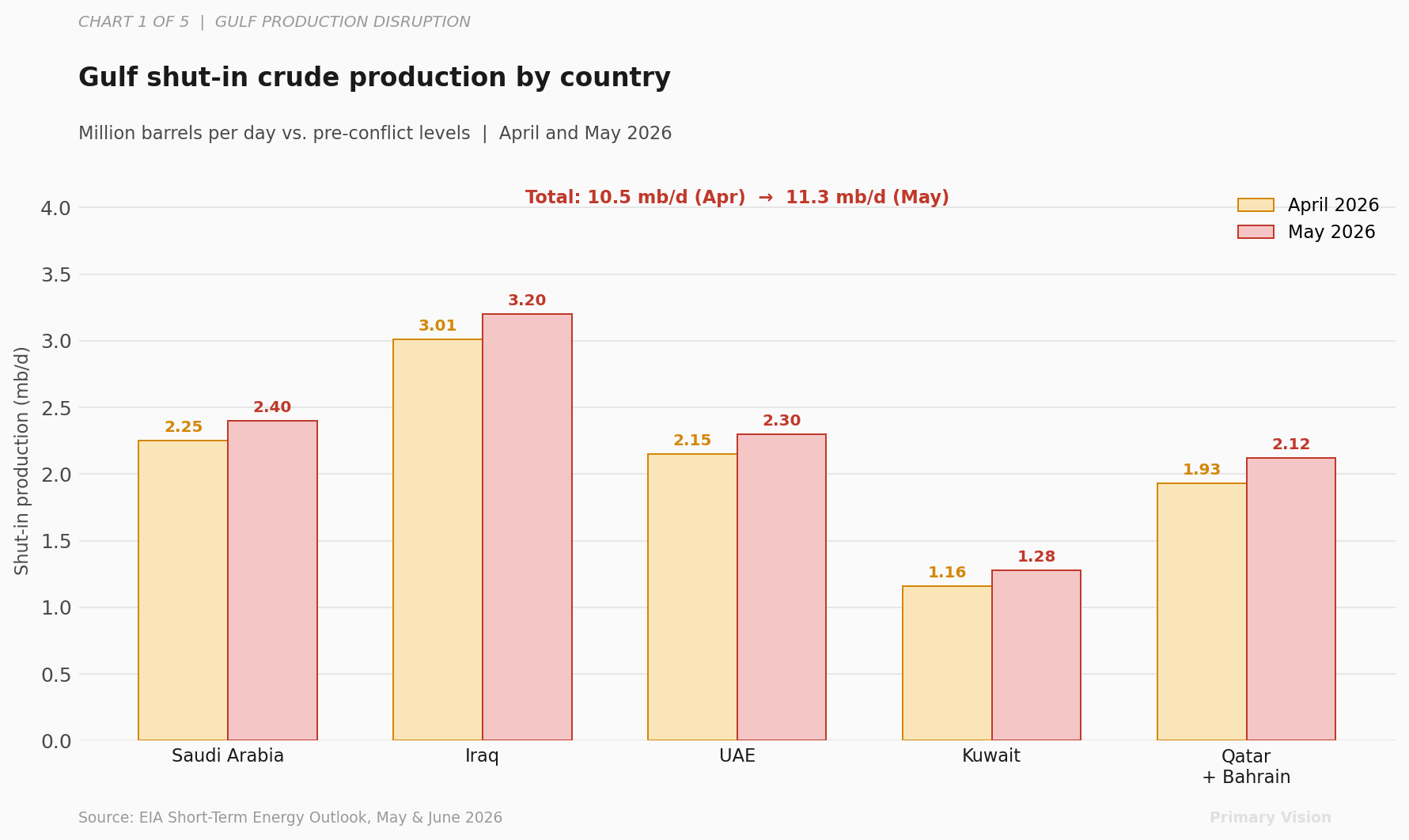

The Frac Spread Count added two crews to reach 192 for the week ending June 12, and the Frac Job Count matched that gain at 237. The rig count at 562 slipped by one but holds above its year-ago mark. Iran's agreement in principle to reduce nuclear enrichment, reportedly reached through Pakistan-mediated talks and framed around a 60-day negotiating window, pulled oil prices lower (a formal agreement still has to be signed). The question that the markets will be asking if and when a deal is signed is whether the roughly 10 million barrels per day of Gulf supply that was offline comes back quickly, slowly, or not at all. The answer depends on four things: whether the loss is a logistics problem or a physical one, how long wells have been shut in, whether production infrastructure was directly struck, and whether bypass routes exist. Running each Gulf producer through that framework produces a very different picture than the one market headlines are currently painting.

Saudi Arabia scores relatively well on all four counts. Its production fields suffered limited direct strikes. The kingdom had bypass capacity through its East-West Pipeline to the Red Sea port of Yanbu, which was itself briefly hit but resumed loadings quickly. The UAE similarly retained export capacity through its Abu Dhabi Crude Oil Pipeline to Fujairah, though Fujairah was periodically taken offline by repeated drone strikes and the Habshan gas processing hub was also suspended twice following attack debris. Both Saudi and UAE upstream wellbore conditions are comparatively intact, and both countries maintained partial export flow throughout the crisis. Under a genuine, sustained Hormuz reopening, their lost crude volumes are largely recoverable within weeks to a couple of months. That is the supply the market is currently pricing in.

Iraq and Kuwait are a fundamentally different problem, and this is where the permanent-loss argument has the most traction. Iraq's output collapsed to approximately 1.39 million barrels per day in April, against a pre-conflict ceiling near 4.4 million. Iraq has no pipeline bypass to speak of — roughly 95 percent of its monetized crude transits Hormuz — so when tanker traffic collapsed, onshore storage tanks filled within weeks and production had to halt at the wellhead. The same happened in Kuwait, which reached storage capacity around day 18 of the closure. Here the petroleum engineering becomes the binding constraint: shut-in wells in mature fields lose reservoir pressure — the natural underground drive that lifts oil to surface — while water and gas from adjacent zones infiltrate the producing interval, and paraffin wax builds up in tubing. Forced shut-ins can reduce long-term well recovery rates by 10 to 30 percent through these mechanisms. The 1991 Gulf War produced the clearest precedent: some Kuwaiti fields lost 15 to 25 percent of long-term recovery capacity. Kuwait's national petroleum corporation chief said in March that even if the war ended immediately, three to four months would be required to restore pre-conflict output — and that assumes wellbore conditions are intact, which is no longer guaranteed. Iraq may take even longer recovery time, up to 8 months because of mature field reservoir management constraints that exist independently of any diplomatic agreement.

Qatar is a third category entirely: not a logistics problem, not a reservoir damage problem, but a physical infrastructure destruction problem with a known multi-year repair clock. Iranian missile strikes on Ras Laffan on March 18 and 19 destroyed LNG Trains 4 and 6, cutting 12.8 million tonnes per year of export capacity, or 17 percent of Qatar's total LNG output. QatarEnergy declared long-term force majeure on contracts to buyers in China, South Korea, Italy, and Belgium. The CEO put the repair timeline at three to five years, a figure constrained not by politics but by the lead time on replacement gas turbines, which runs two to four years globally. Separately, the Habshan gas processing complex in the UAE — one of the world's largest, processing over 6 billion cubic feet per day — was suspended twice after attack debris sparked fires on site. These disruptions require replacement equipment which has to be manufactured, shipped, and installed. That means time.

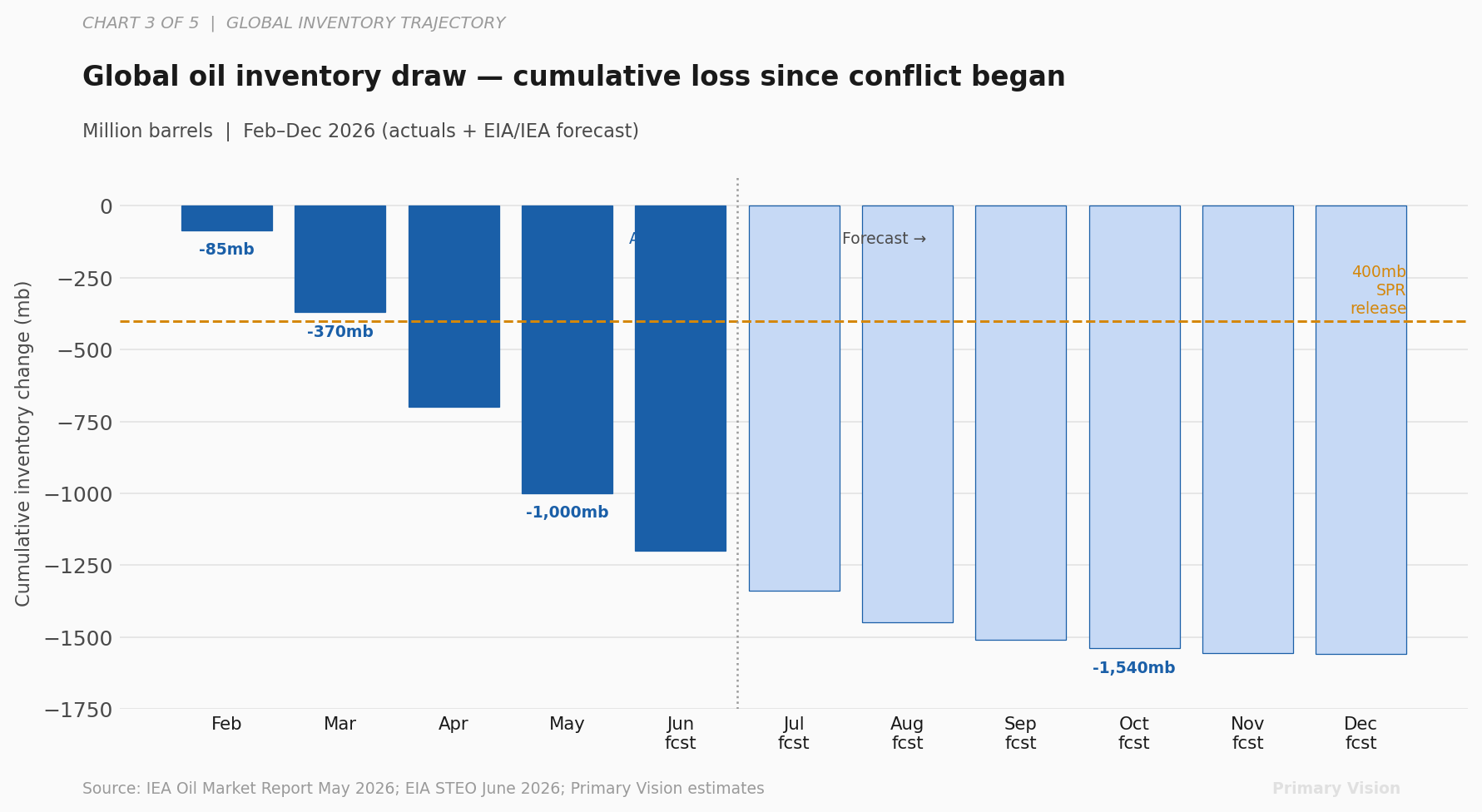

Oil has fallen to $80, and the market has clearly decided the worst of the supply disruption is behind us — and it may be right. But roughly 2.4 million barrels per day of Gulf production faces a recovery timeline measured in years, not weeks. Those barrels will not be back because a deal was signed. Whether that gap is enough to move prices materially from here remains to be seen — but for US completion activity, it remains a quiet source of structural support that will keep both metrics on the higher end for now.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform