Outlook Signals Improving Market

ProFrac’s management observed that market conditions shifted materially beginning in late February and continued strengthening through March. Frac utilization went higher late in the quarter, and the hydraulic fracturing calendar tightened into Q2. The company believes limited available pressure pumping capacity, combined with activity levels below those needed to maintain flat shale production, could improve supply-demand dynamics into 2H 2026.

Management also pointed to geopolitical disruptions in the Middle East and ongoing energy security concerns as supportive of stronger North American oil and gas activity. The optimization program remains a central focus. However, conditions remain uneven across segments. While Stimulation Services is expected to improve sequentially in Q2, Proppant Production volumes are expected to decline due to operational issues and unplanned downtime.

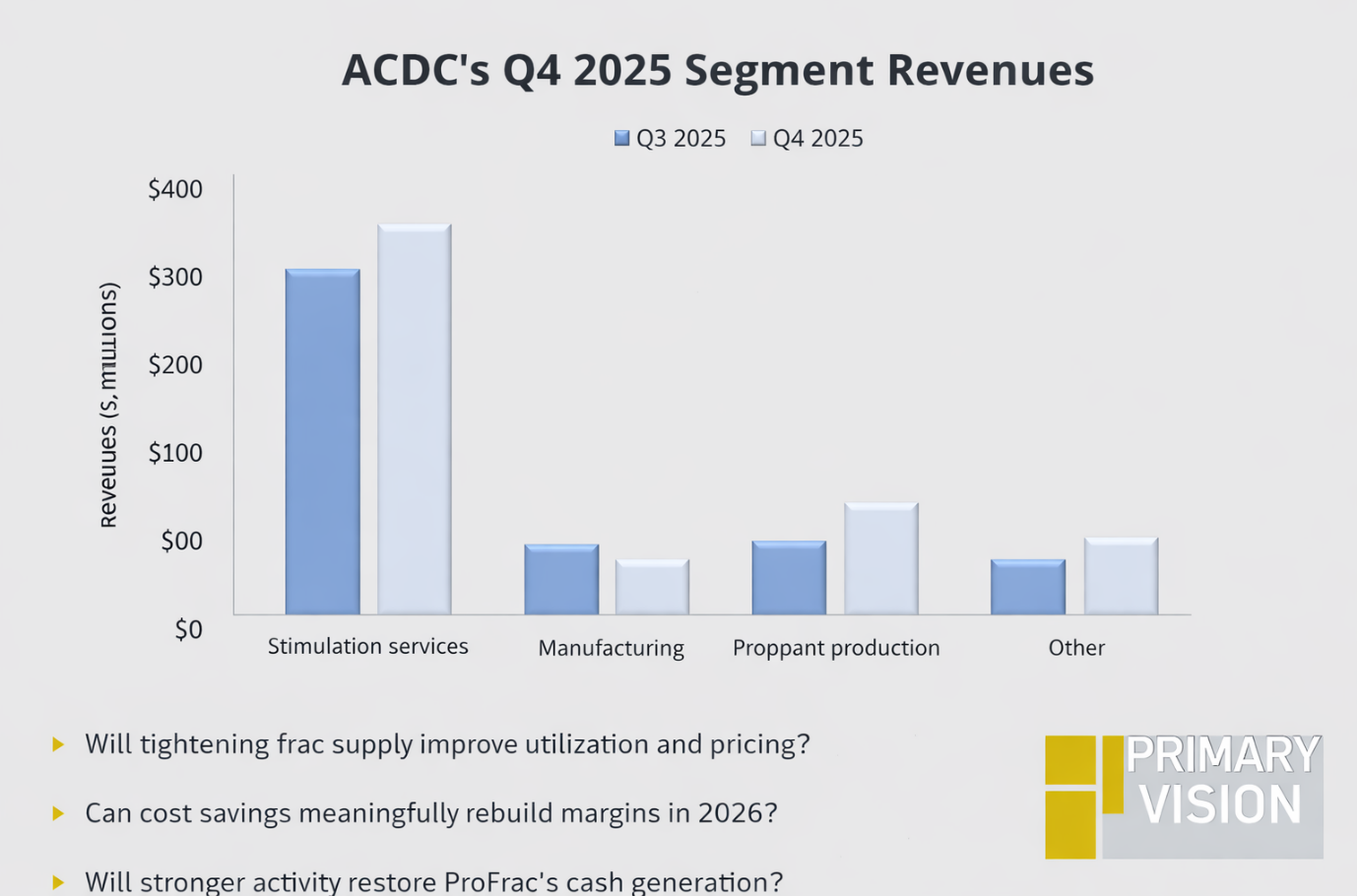

Segment Performance in Q1

Sequentially, total revenue increased ~3% in Q1, supported by improving activity levels late in the quarter. Stimulation Services revenue increased ~6% sequentially, but adjusted EBITDA declined ~4%, as weather-related inefficiencies offset stronger utilization later in the quarter.

Proppant Production revenue increased ~4%, while adjusted EBITDA declined sharply (~59%), reflecting operational disruptions and weaker profitability. Manufacturing improved sequentially, with revenue increasing ~14% and adjusted EBITDA nearly doubling, supported by stronger internal demand. Flotek continued to improve, with both revenue and EBITDA increasing sequentially, reflecting gradual integration benefits and stronger product activity.

FCF Fell Sharply in Q1: Cash generation weakened sequentially in Q1. Free cash flow turned negative compared to positive free cash flow in Q4. However, capital spending remains disciplined relative to prior cycle peaks. ProFrac maintained its FY2026 capital expenditure guidance at $155M–$185M despite improving activity expectations.

Leverage (debt/equity) remains elevated, with net debt increasing to ~$1.05 billion. The setup into 2H 2026 increasingly depends on whether tightening frac supply can translate into sustained pricing recovery and stronger cash generation.

Thanks for reading the ACDC Take Three, designed to give you three critical takeaways from ACDC's earnings report. Soon, we will present a second update on ACDC earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.