FTI’s Offshore Strategy

We have already discussed TechnipFMC's (FTI) Q1 2026 financial performance in our recent article. This article will dive deeper into the industry and its current outlook. Subsea orders reached $1.9 billion, supported by strong services activity and direct project awards.

Order momentum is improving, reinforcing confidence in achieving $10 billion in Subsea orders for 2026.

Around 50% of FTI’s revenue could come from Subsea 2.0 orders by 2027, reflecting a growing contribution from this model. With the majority of new orders now Subsea 2.0, the company is improving efficiency, shortening cycle times, and enhancing project economics.

Geographic Capital Flows

FTI observes that capital is increasingly shifting toward offshore developments, especially in regions like the U.S. Gulf, the North Sea, and West Africa. The Subsea opportunity pipeline has grown to around $30 billion over the next 24 months. This represents sustained expansion, with the opportunity set increasing more than 30% over two years. Larger project sizes and growth in key regions are supporting a stronger long-term outlook.

Outlook And Key Drivers

FTI expects inbound orders to accelerate from 2027 and continue growing through the decade. Growth will be driven by Subsea 2.0, iEPCI, and increasing direct awards. Strategically, the company is focused on reducing cycle times to improve project economics and efficiency.

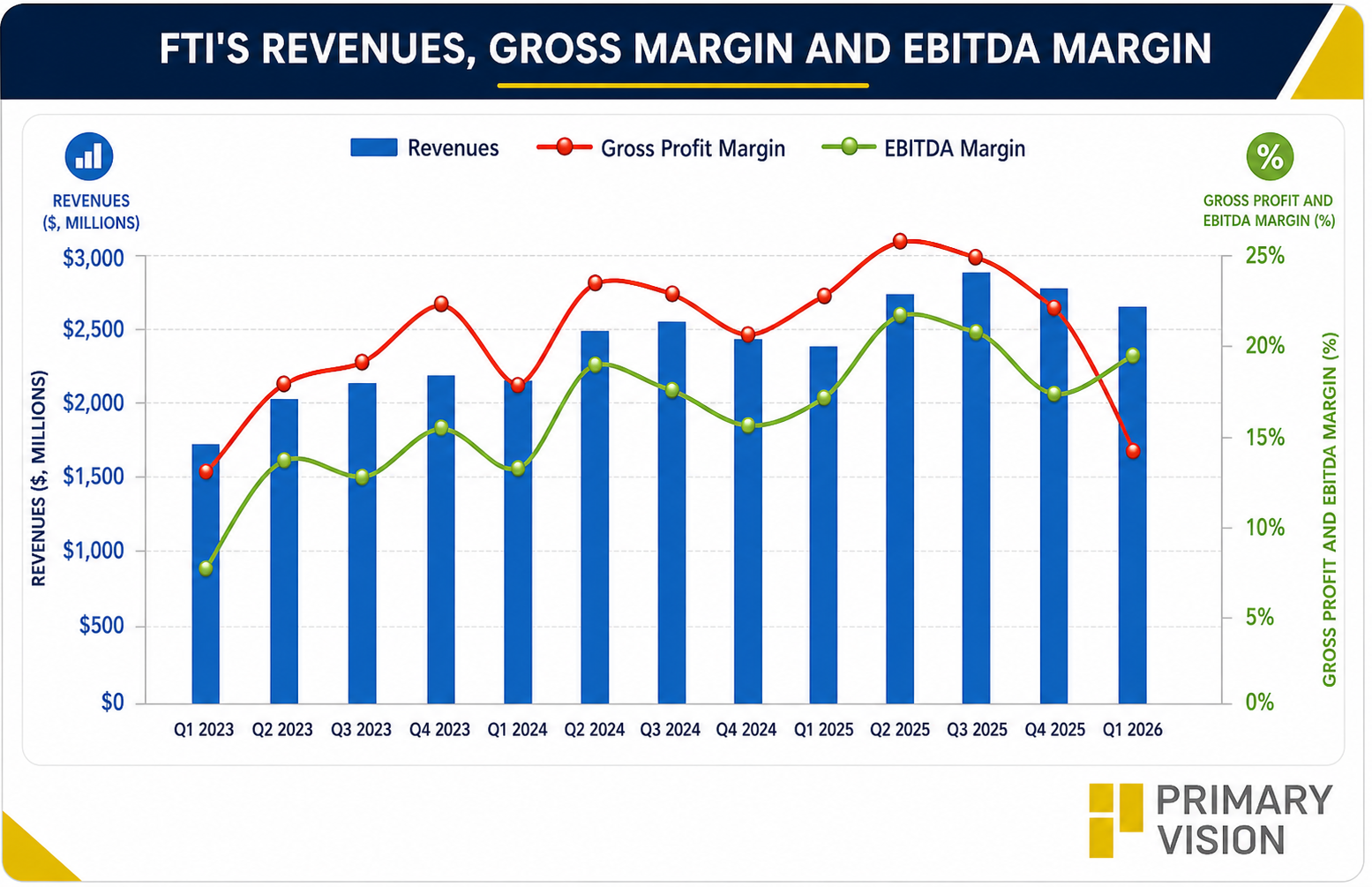

The management expects Subsea revenue to grow sequentially in the “high single digits,” with margins improving to around 23%. Surface Technologies revenue is expected to “decline slightly”, with margins near 17%.

Subsea has strong visibility, with about 95% of 2026 revenue already covered by backlog. The company remains confident in exceeding $2.1 billion EBITDA in 2026 and delivering continued growth into 2027.

So, 2026 is expected to be driven by smaller awards, with larger project contributions shifting toward 2027 and beyond. Growth is broad-based across offshore oil and gas regions, including Latin America, Africa, and Asia Pacific. Offshore investment is strengthening, supported by capital rotation from U.S. onshore and improving project economics.

Relative Valuation

FTI is currently trading at an EV/adjusted EBITDA multiple of 14.3x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 12.8x. The current multiple is higher than its five-year average EV/EBITDA multiple of 10.5x.

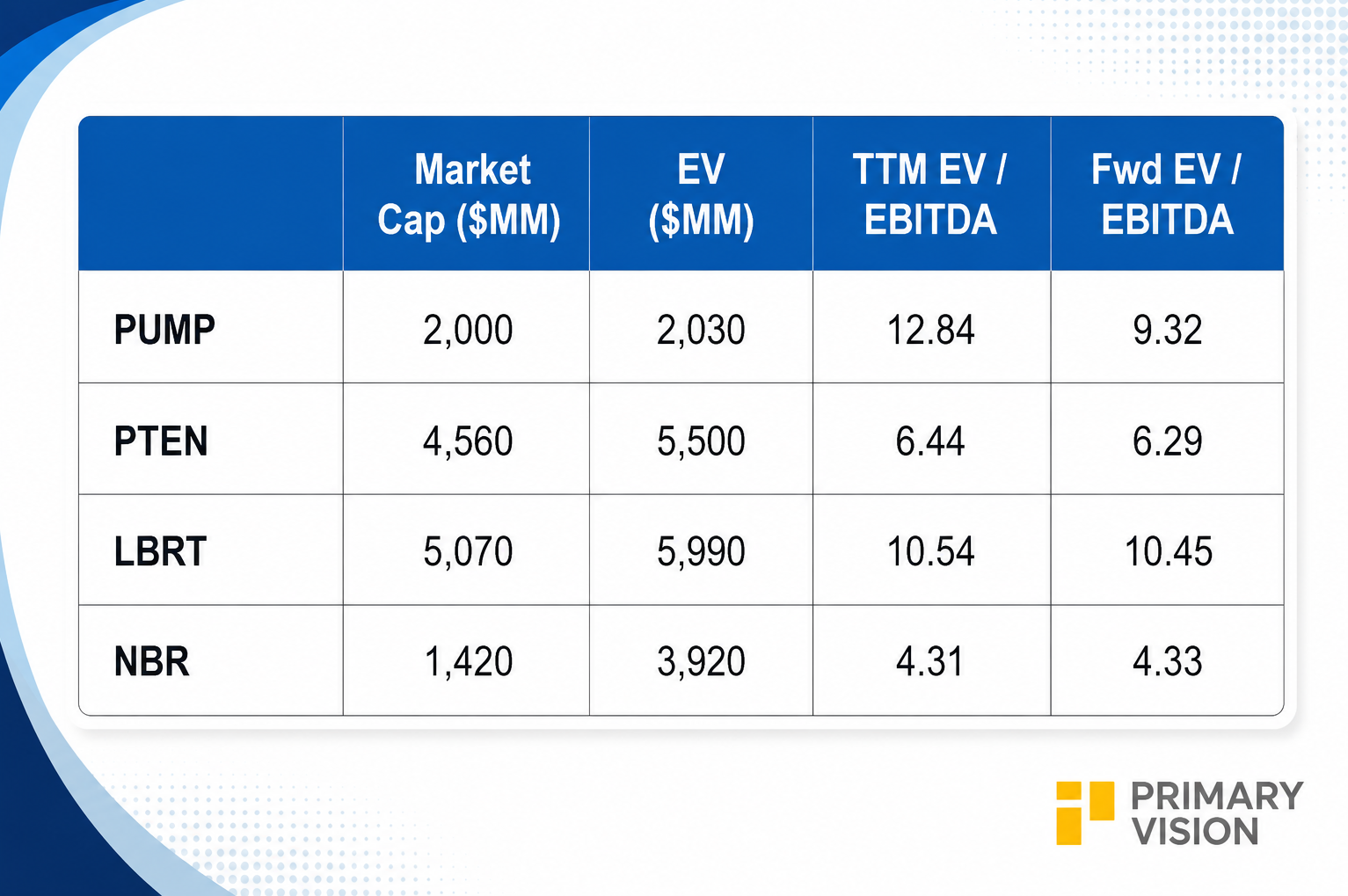

FTI's forward EV/EBITDA multiple contraction versus the adjusted current EV/EBITDA is steeper than peers' because the company's EBITDA is expected to increase more sharply in the next four quarters. This typically results in a higher EV/EBITDA multiple than peers. The stock's EV/EBITDA multiple is higher than its peers' (SLB, BKR, and HAL) average of 11.9x. So, the stock is reasonably valued compared to its peers.

Final Commentary

Capital is clearly shifting offshore, with a $30 billion pipeline of opportunities and larger project sizes. So, TechnipFMC is seeing strong Subsea momentum, with rising orders supporting its $10 billion 2026 target. Subsea 2.0 is becoming the dominant model, improving efficiency, shortening cycle times, and enhancing project economics. Its near-term performance remains supported by strong backlog visibility and improving margins in Subsea.

However, 2026 will be driven more by smaller awards, with larger projects weighted toward 2027 and beyond. Overall, I believe the company is well-positioned for a multi-year offshore growth cycle driven by technology, direct awards, and global capital reallocation.

The stock is reasonably valued compared to its peers.