Articles

- BLOG / Articles / View

- Articles

Weatherford's Perspective in Q1 2026: KEY Takeaways

By Avik on May 8, 2026 in Articles

Geographic Growth Outlook

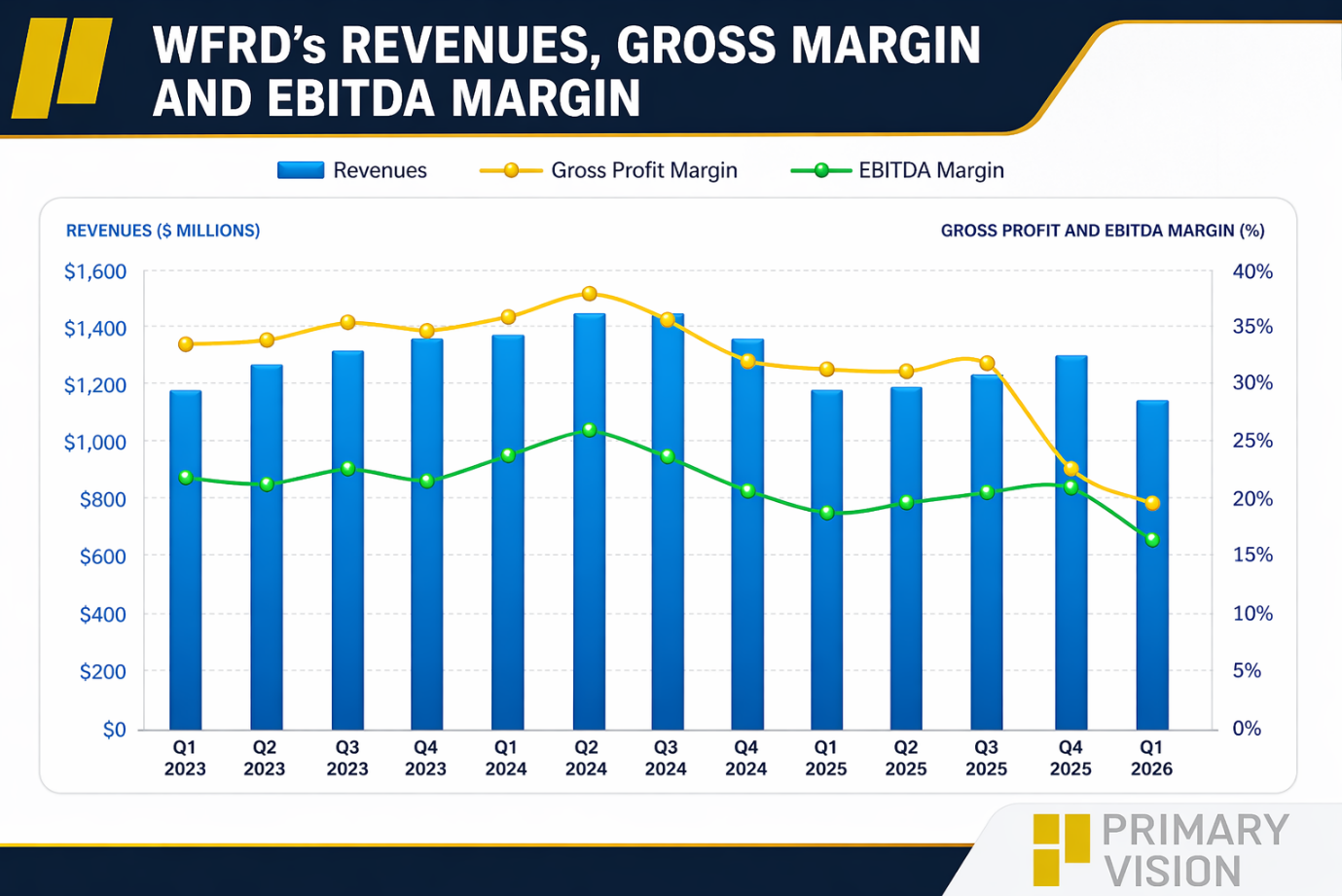

We discussed our initial thoughts about Weatherford International's (WFRD) Q1 2026 performance in our short article a few days ago. This article will dive deeper into its current outlook. First, let’s look into the geographic drivers. North America remained soft as operators maintained tight budgets and U.S. land activity stayed under pressure. Latin America declined sequentially, though higher artificial lift activity in Argentina provided some offset. Mexico showed improvement, with strong collections supporting cash flow and working capital efficiency.

Middle East disruptions led to delays, lower activity, and project suspensions across multiple countries. Rising freight and logistical challenges increased costs and are expected to weigh more on Q2 results. I think the impact is temporary, with recovery expected later in the year and a stronger outlook into 2027.

Short and Medium-term Outlook

WFRD expects stronger growth in the second half of 2026, supported by new project start-ups across multiple regions. However, this outlook depends on Middle East conditions normalizing to pre-conflict levels. International revenues are expected to improve year-over-year in 2H 2026, with 2027 shaping up as a growth year.

Offshore activity is showing early signs of recovery across key basins. Structural tailwinds, including energy security and deferred project restarts, support a multi-year upcycle. I think the setup points to a durable recovery, with both international and North American activity strengthening over time.

WFRD’s Q2 revenue is expected to decline ~7.6% sequentially at the midpoint due to Middle East disruptions. Adjusted EBITDA is expected to decline ~10.9% QoQ at the midpoint, reflecting cost pressures and operational inefficiencies. Free cash flow is expected to remain broadly in line with Q1 levels. For FY2026, performance is expected to be weighted toward a stronger 2H 2026.

Cost Cutting and Working Capital Plans

The company is rightsizing its cost structure across headcount, real estate, and supply chain to align with activity levels and protect profitability. It is also improving productivity by leveraging shared services, digital platforms, and AI to drive efficiency and margins. These actions helped offset revenue declines, pricing pressure, geopolitical disruptions, and the Argentina divestiture impact in Q1.

Working capital improved sequentially to 27.9% of revenue, supported by stronger collections, particularly in Mexico. Management remains confident in free cash flow despite still-elevated outstanding receivables. The company is targeting a further improvement to 25% through ongoing internal initiatives. It also returned $30 million to shareholders in Q1, continuing a consistent capital return program.

Relative Valuation

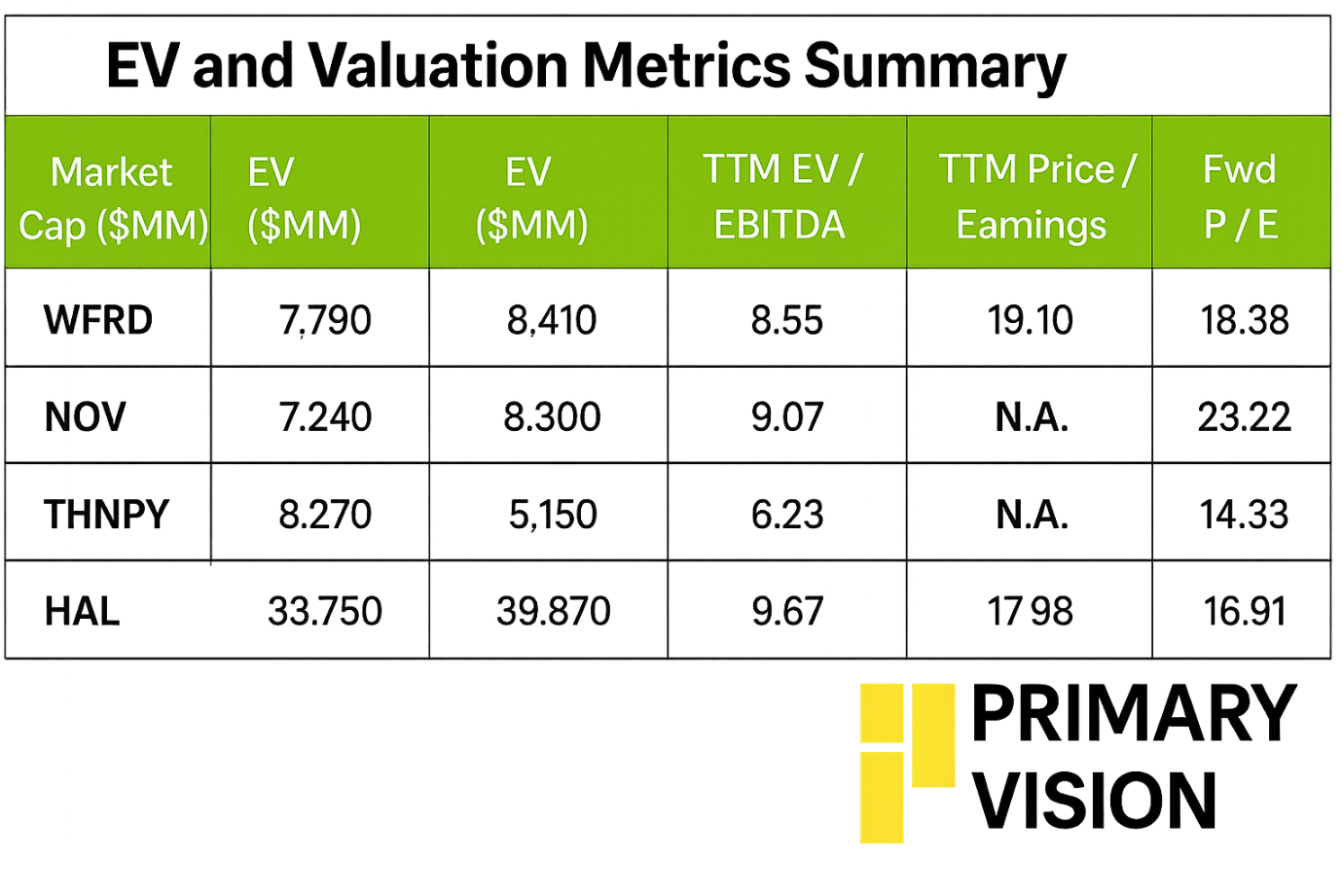

WFRD is currently trading at an EV/EBITDA multiple of 8.6x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 8.4x. The current multiple is significantly lower than its past five-year average EV/EBITDA multiple of 46x.

WFRD's forward EV/EBITDA,versus the current EV/EBITDA multiple, is expected to contract less steeply than its peers. So, the company's EBITDA is expected to increase less sharply than its peers in the next year. This typically results in a lower EV/EBITDA multiple. The stock's EV/EBITDA multiple is lower than its peers' (NOV, THNPY, and HAL) average. So, the stock is reasonably valued, with a negative bias, compared to its peers.

Final Commentary

Weatherford’s near-term outlook remains pressured, with North America soft and Middle East disruptions weighing on activity and costs. However, Mexico collections and Argentina activity are supporting cash flow and operational stability. Q2 is expected to see sequential declines in revenue and EBITDA, reflecting ongoing geopolitical and cost headwinds.

Looking ahead, growth is expected to improve in 2H 2026, driven by international project ramp-ups and early offshore recovery. Overall, cost discipline, working capital improvement, and structural industry tailwinds position the company for a stronger recovery into 2027. The stock is reasonably valued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform