Articles

- BLOG / Articles / View

- Articles

AI and Power Series: Who Moved First, Who Is Real, and Who Is Still Narrating

By Avik on February 2, 2026 in Articles

The separation is becoming visible

Part 1 of the series established the structural backdrop: the traditional grid struggles to meet AI-driven timelines, speed increasingly determines viability, and a parallel power supply model is beginning to form. Part 2 shifts the focus to company-specific differentiation. The central question is no longer whether the opportunity exists, but which companies are converting the theme into tangible businesses.

This distinction increasingly matters for investors, operators, and competitors. The divergence is no longer conceptual. It is evident in disclosed capacity, contractual progress, organizational structure, partnerships, and evolving business mix. The AI power narrative is therefore moving away from a sector-wide story and toward a stock-by-stock evaluation. Power Solutions is expected to become a significant contributor to EBITDA over time, signaling more than adjacency and pointing toward a structural reweighting of the business.

Capturing The Power Journey

Liberty, ProPetro, ProFrac, and New Fortress Energy are the key players shown here, all of which we discussed in Part 1 of this series. The timeline highlights how their power-related initiatives have accelerated from early experimentation toward more structured partnerships and pilots. The takeaway is momentum, but at very different stages of maturity.

Solaris: Early scale and structural commitment

Solaris Energy Infrastructure appears furthest along in translating the AI power theme into an operating business. Its presentation outlines a path toward 2.2 GW of operated capacity by 2028, with more than 1 GW already associated with two data center customers.

SEI has invested in internal capability through the acquisition of electrical engineering and integration assets, reducing dependence on third-party EPC providers and increasing control over design. Its geographic approach is broader than most peers. Its materials reference hyperscalers, industrial users, utilities, and microgrid applications across markets. The company currently shows the clearest evidence that power is evolving into a core business line rather than a peripheral initiative.

ProPetro: Credible structure with execution ahead

ProPetro has taken tangible steps toward building a power platform. The creation of its dedicated subsidiary, PROPWR, provides organizational focus. The company has disclosed approximately 360 MW of mobile natural gas generation capacity secured through equipment supply agreements extending into 2027. Management has explicitly referenced data centers and non-oilfield industrial demand as target markets.

The strategic logic is grounded in geography. ProPetro’s footprint is heavily concentrated in the Permian Basin. That brings proximity to natural gas supply, infrastructure density, and operational familiarity. The company directly links these advantages to potential demand from power-intensive customers seeking alternatives to congested grid markets.

Halliburton: Exposure without ownership

Halliburton’s positioning reflects a different risk-reward profile. Its partnership with VoltaGrid includes a 400 MW manufacturing commitment for modular power systems. That provides exposure to rising demand for distributed generation while avoiding direct ownership of generation fleets.

Strategically, this approach is conservative. It allows HAL to benefit from increased equipment demand without committing large amounts of capital to long-lived assets. It also limits exposure to regulatory, operational, and financing complexity inherent in owning power infrastructure.

The trade-off is upside. Asset-light participation is unlikely to drive the same business mix transformation as fleet ownership. Primary Vision thinks HAL’s strategy is pragmatic but should be evaluated differently from companies seeking to build power as a primary revenue stream.

Other Aspirants

Liberty Energy’s power strategy has developed logically from its frac electrification efforts. Liberty Power Innovations established an internal platform. The acquisition of IMG Energy adds engineering depth and signals intent to build capability rather than rely exclusively on partners. However, there are currently no disclosed megawatt targets, contracted capacity figures, or visible commercial scale in the public materials. Other energy firms are peripherally exposed. New Fortress Energy operates large gas-to-power portfolios. Caterpillar and GE Vernova benefit as turbine and genset suppliers. But the strategic shift — building dedicated power businesses — is concentrated inside oilfield services.

Geography as a differentiator

Across all players, geographic positioning is a determinant of viability. This market will remain fragmented and localized, shaped by infrastructure and policy at the regional level. Permian adjacency matters. Access to low-cost gas, existing infrastructure, experienced workforce, and regulatory familiarity all influence project economics and execution risk. That is why ProPetro’s thesis resonates. It is grounded in basin realities rather than abstract demand growth.

SEI’s broader market strategy introduces both opportunity and complexity. Operating across regions opens access to larger contracts but also increases exposure to differing regulatory regimes and stakeholder environments.

What the market will ultimately reward

Narrative will matter less over time. Evidence will matter more. Investors are likely to focus increasingly on disclosed megawatts under contract, quality and duration of counterparties, utilization and uptime performance, capital efficiency of deployments, and repeatability of project execution. The next 12–24 months will be crucial as early projects move from announcement to operation.

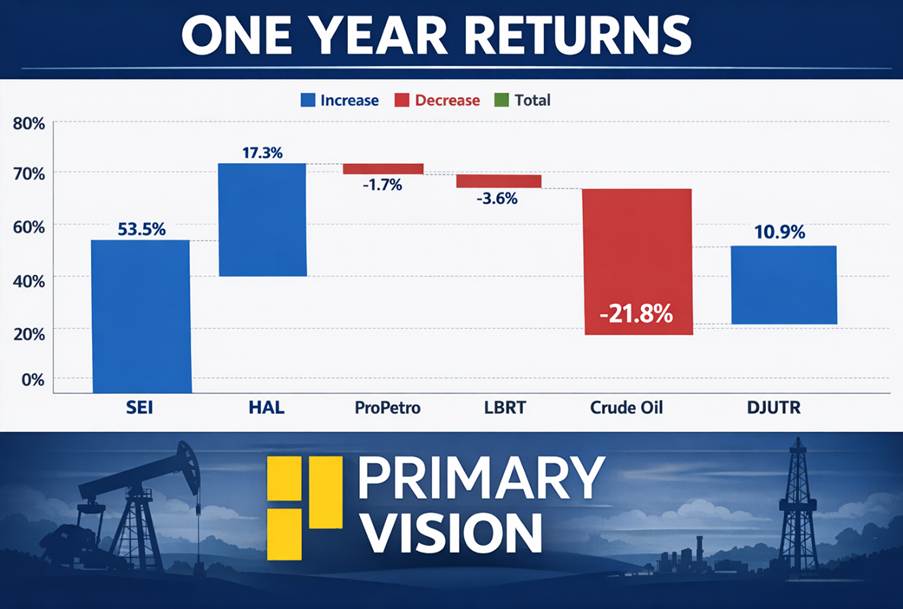

SEI’s strong 53.5% return over the past year suggests the market is already rewarding companies perceived as early and credible in the AI-linked power transition, rather than simply benefiting from the oilfield cycle. HAL’s positive performance reflects the value investors place on exposure to the theme with lower execution risk. The weaker returns for ProPetro and Liberty, alongside the sharp decline in crude oil, reinforce that this is not a traditional energy beta trade but an emerging, company-specific re-rating story.

Conclusion: the theme is real, the dispersion is real

The opportunity created by AI-driven power demand is real. SEI has moved early and is building scale. ProPetro has credible structure and geographic logic, with execution now the key variable. Liberty has established direction and capability but remains earlier in commercial development. Halliburton has chosen participation without ownership, balancing exposure with risk control.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform