Backlog Remains Elevated, But Order Intake Softened In Q4

Q4 orders totaled $7.9 billion, down sequentially from Q3, bringing full-year orders to $29.6 billion. Remaining Performance Obligations increased to a record $35.9 billion exiting 2025, reflecting strong order intake earlier in the year rather than accelerating Q4 demand. Book-to-bill remained above 1.0x for both the quarter and the full year, supporting backlog coverage into 2026 despite slower sequential order flow.

Within IET, Q4 orders of $4.0 billion declined sequentially, though segment RPO reached a record $32.4 billion. Backlog composition continued to skew toward LNG, gas infrastructure, power systems, and industrial technology projects, with non-LNG equipment representing the majority of IET orders. Overall, backlog depth remains intact, but Q4 results indicate that order momentum cooled across both segments.

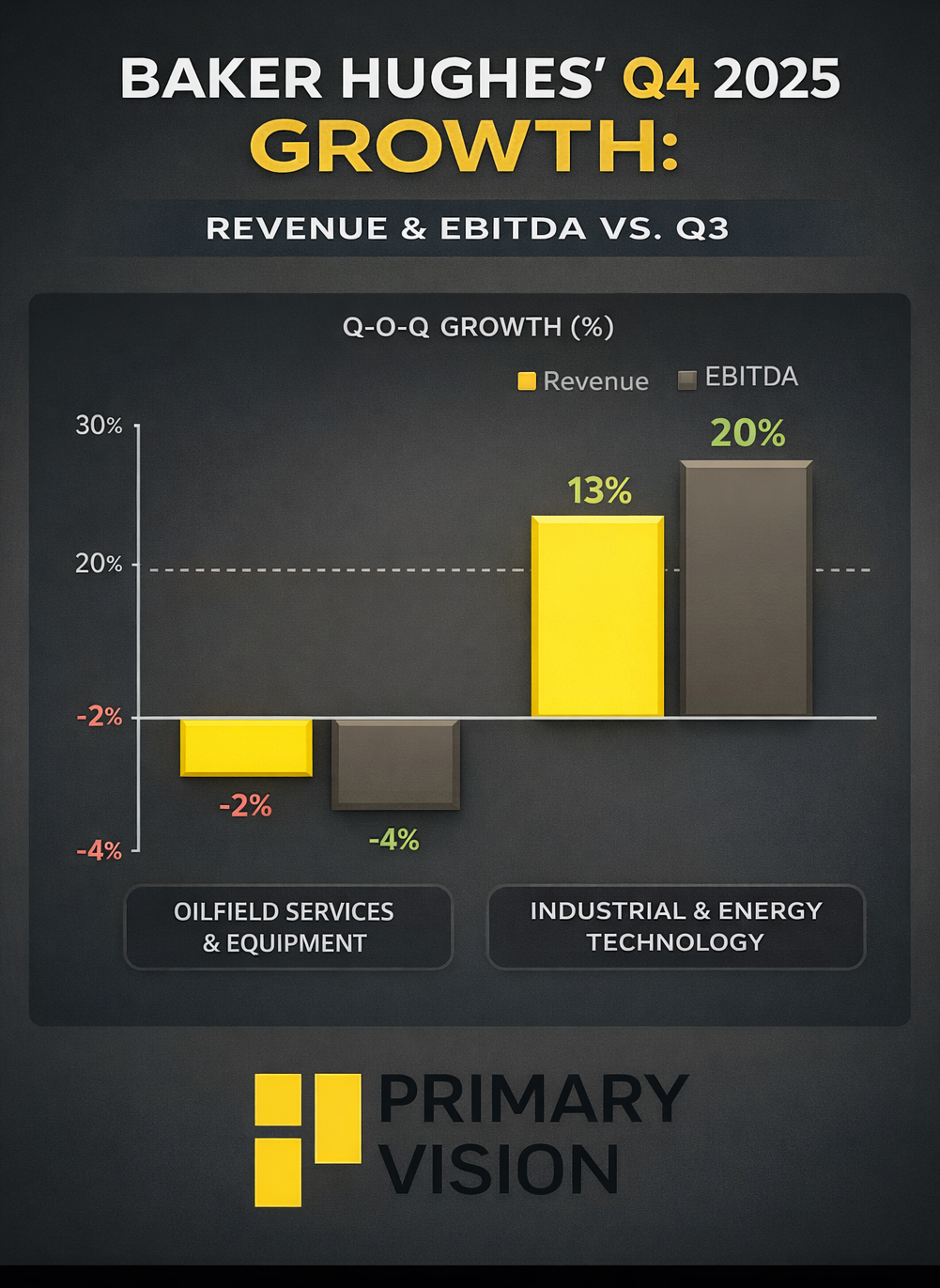

Segment Revenue and EBITDA Diverged in Q4: IET delivered a stronger Q4, with revenue increasing 13% sequentially and EBITDA rising 20%, lifting segment margins to 20.0%. Performance reflected higher volumes across gas technology equipment and services, pricing, productivity gains, and favorable FX, partially offset by inflation. For full-year 2025, IET revenue grew 10% year over year, and EBITDA increased 21%, reinforcing the segment’s role as the company’s primary earnings driver.

OFSE results remained constrained. Q4 revenue declined 2% sequentially and 8% year over year, while EBITDA fell 4% sequentially, reflecting lower volumes and unfavorable business mix despite continued cost-out initiatives. International revenue softened modestly, with weakness in the Middle East/Asia partially offset by Europe and Latin America, while North America also declined sequentially. Margins remained relatively resilient but continue to face pressure from activity softness and inflation..

FY2025 Cash Flows Improved: For FY2025, Baker Hughes generated free cash flow of $2.7 billion, supported by disciplined capital spending and working capital efficiency rather than volume-led growth. Net debt declined year over year, and leverage remained modest, preserving balance-sheet flexibility. While Q4 cash flow benefited from customer down payments and timing-related working capital inflows, full-year performance provides a more reliable indicator of cash generation sustainability heading into 2026.

Thanks for reading the BKR Take Three, designed to give you three critical takeaways from BKR's earnings report. Soon, we will present a second update on BKR earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.