Articles

- BLOG / Articles / View

- Articles

Baker Hughes's Perspective in Q4 2025: KEY Takeaways

By Avik on February 20, 2026 in Articles

Market and Strategy

We have already discussed Baker Hughes's (BKR) Q4 2025 financial performance in our recent article. Here is an outline of its strategies and outlook. Baker Hughes’s management expects the macro environment to stay resilient through 2025 and should improve modestly in 2026. Long-term energy demand continues to rise with population growth and electrification. AI, digital infrastructure, and data centers are adding a durable new layer of power demand. A broader inflection in oilfield services activity likely requires tighter balances and now looks more like a 2027 event.

Natural Gas and LNG Market Outlook

Baker Hughes continues to believe that natural gas remains central to the energy mix, with global demand expected to grow around 20% by 2040. It will support a rising investment in gas and power infrastructure. LNG demand is also on a strong trajectory, with expectations of at least 75% growth by 2040 and improving near-term FID visibility. The company expects to exceed its 2024–2026 LNG FID outlook, reinforcing confidence in the long-term installed base outlook.

For 2026, global upstream spending is expected to decline low single digits, with North America down mid single digits and international slightly lower overall. However, production-weighted exposure should allow the company to outperform a soft market. Over the longer term, investment should skew toward international, offshore, and OpEx-driven activity focused on recovery and asset life extension.

Power Business Growth

The power business is becoming a more central pillar within Baker Hughes’ portfolio. Power systems orders reached $2.5 billion in 2025, including $1 billion linked to data centers. Baker Hughes now expects to book around $3 billion of data center-related orders over 2025–27 and is working toward doubling NovaLT turbine capacity by H1 2027. NovaLT turbines booked around 2 gigawatts of orders, with a further 1 gigawatt slot reservation that could convert into firm orders in 2026. The portfolio is now differentiated across power generation, grid stability, and energy management, supported by continued investment and acquisitions.

Management views global power demand as entering a multi-year growth cycle, with electricity consumption potentially doubling by 2040 and gas-fired generation playing a key role. The company is increasingly shifting toward power, data centers, and LNG to offset softness in oilfield services. It appears that the strategy will drive growth in the next phase.

IET and New Energy Order Outlook

IET booked $4 billion of orders in Q4 and $14.9 billion for the full year, finishing above the high end of guidance. Backlog ended the year at $32.4 billion, with book-to-bill above 1x. Around 85% of orders came from non-LNG equipment, reflecting broad demand across power generation, New Energy, and energy infrastructure. LNG orders reached $2.3 billion in 2025 and are expected to remain similar in 2026, supported by new long-term service agreements.

BKR’s New Energy (non-traditional energy like Hydrogen and ammonia, CCUS, Geothermal, Power generation, and Industrial decarbonization) booked $434 million in Q4 and $2.0 billion for the year, exceeding the previous target, supported by blue ammonia and geothermal awards. Management is targeting $2.4–$2.6 billion of New Energy orders in 2026.

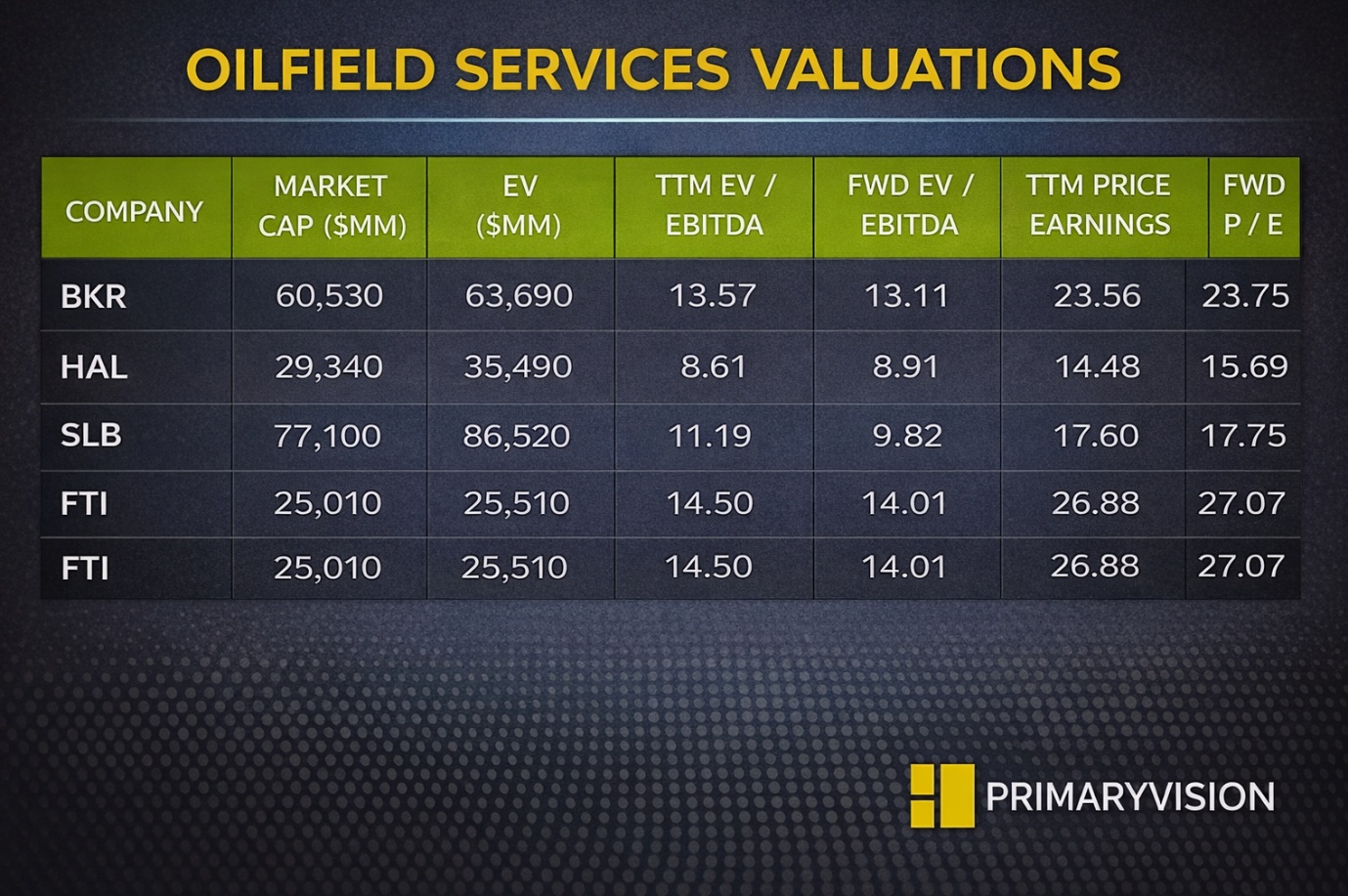

Relative Valuation

Baker Hughes is currently trading at an EV/EBITDA multiple of 13.6x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 13.1x. The current multiple is higher than its five-year average EV/EBITDA multiple of 10.6x.

BKR's forward EV/EBITDA multiple contraction versus the current EV/EBITDA is less steep than its peers because the company's EBITDA is expected to increase less sharply in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock's EV/EBITDA multiple is higher than its peers' (HAL, SLB, and FTI) average. So, the stock appears overvalued compared to its peers.

Final Commentary

Near-term industry conditions look steady, but Baker Hughes’ management believes a broader oilfield services inflection is likely to shift to 2027. Long-term demand remains constructive, driven by electrification, AI, and rising power intensity across the global economy. Natural gas and LNG sit at the center of the company’s strategy, with strong multi-decade demand growth and improving project visibility. The power business is becoming a key growth pillar, supported by rising orders, NovaLT expansion, and growing exposure to data centers and grid infrastructure.

IET and New Energy orders continue to show momentum, with backlog strength and increasing contribution from power, energy infrastructure, and transition technologies. Overall, Baker Hughes is positioning away from pure OFS cyclicality toward structurally growing end markets, which should improve resilience across cycles. The stock appears overvalued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform