BP’s Strategic Priorities

We discussed our initial thoughts about BP's (BP) Q1 2026 performance in our short article a few days ago. This article will dive deeper into its current outlook. The company has announced 14 discoveries since early 2025, many of which are short-cycle and can be quickly tied to existing infrastructure. These discoveries support near-term production growth and help offset natural decline. It also has significant long-term opportunities, including the large Bumerangue field discovery.

However, execution and balance sheet strength remain key priorities before accelerating growth investments. The company is prioritizing structural cost reductions, targeting $6.5B–$7.5B by 2027, supported by portfolio simplification and divestments. Overall, the strategy balances near-term production gains with longer-term development while maintaining financial discipline.

Strategic Alignments

The company has announced 14 discoveries since early 2025, many of which are short-cycle and can be quickly tied to existing infrastructure. These discoveries support near-term production growth and help offset natural decline. It also has significant long-term opportunities, including the large Bumerangue field discovery.

The U.S. remains central to BP’s business, driving future growth across upstream and downstream segments. Key assets like Bumerangue and strong Middle East positions support long-term growth potential. The company is also divesting non-core assets, including Castrol and the Gelsenkirchen refinery, to sharpen its portfolio.

LNG Focus

BP’s LNG portfolio has grown, with nearly 27 MTPA in strategic supply and around 15 MTPA in merchant volumes. The portfolio is highly diversified, sourcing LNG from multiple regions to serve global demand. This flexibility allows optimization of flows and reliable delivery despite market disruptions. While price volatility has moderated, the underlying fundamentals of the LNG business remain strong. So, BP is restructuring its organization into defined upstream and downstream segments to improve decision-making speed.

Relative Valuation

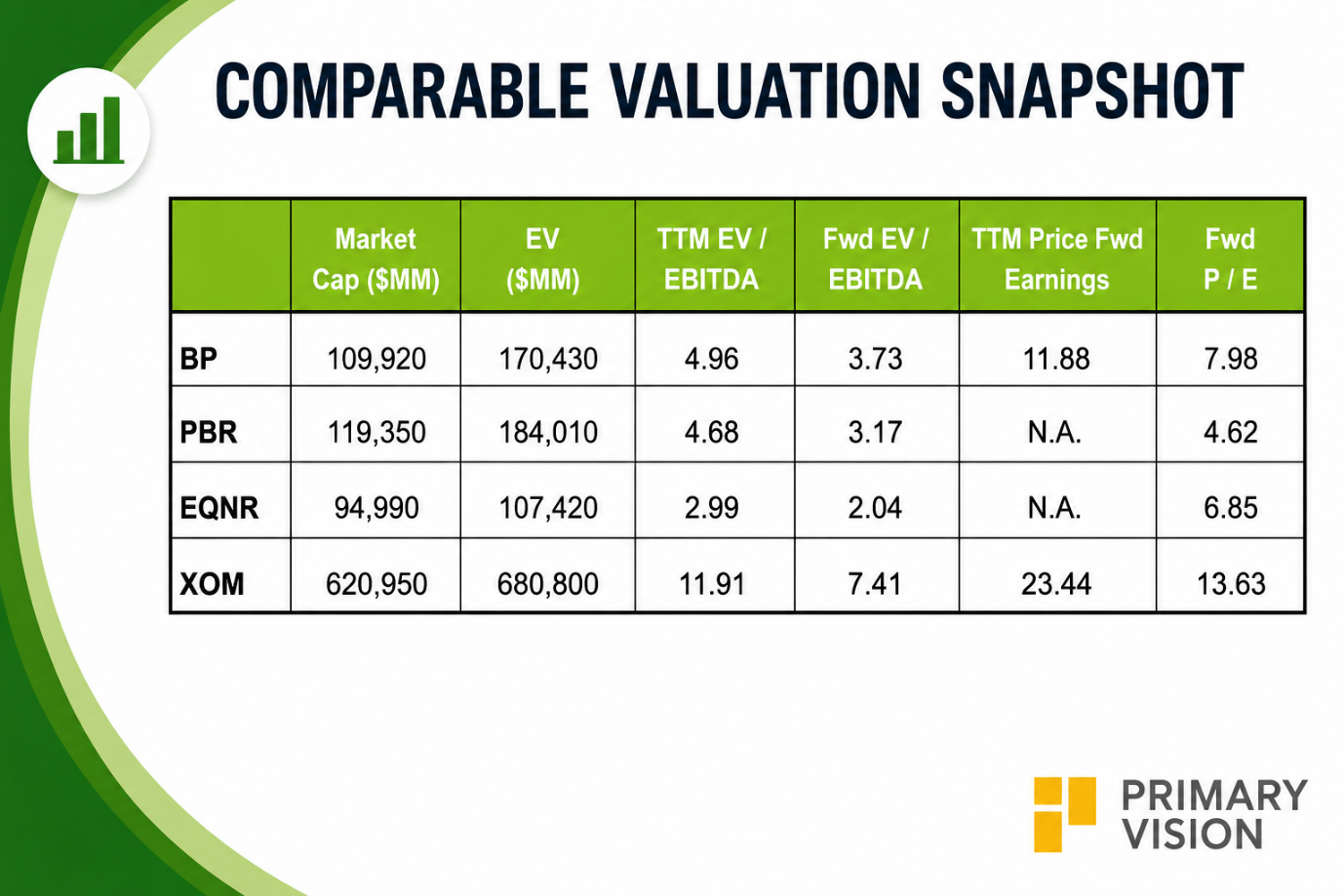

BP is currently trading at an EV/EBITDA multiple of 4.9x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 3.7x. The current multiple is higher than its past five-year average EV/EBITDA multiple of 4.7x.

BP's forward EV/EBITDA multiple versus the current EV/EBITDA is expected to contract less steeply than its peers. This means the company's EBITDA is expected to increase less sharply than its peers in the next year. This typically results in a lower EV/EBITDA multiple. The stock's EV/EBITDA multiple is lower than its peers' (PBR, EQNR, and XOM) average of 6.5x. So, the stock is reasonably valued compared to its peers.

Final Commentary

Overall, BP is driving near-term production through its recent discoveries, with many short-cycle assets tied to existing infrastructure. These gains help offset decline, while larger projects like Bumerangue support long-term growth potential. The U.S. remains a core growth engine, complemented by selective global assets and an expanding LNG portfolio.

However, management is prioritizing execution discipline and balance sheet strength before accelerating investment. The company is targeting $6.5B–$7.5b in structural cost reductions, supported by divestments and portfolio simplification. The stock is reasonably valued compared to its peers.