Articles

- BLOG / Articles / View

- Articles

Break-even Series Part 3: Imagine Everything Goes Wrong

By Avik on December 13, 2025 in Articles

What If Price Drops?

A few weeks earlier, Osama discussed the context of break-even prices for the energy operators and why they matter for the industry. Later, we discussed the significance of the BE prices for some major US energy producers. In today’s article, we shall explore the possibility of a crude oil price fall and its impact on these operators’ margins and production.

Given today’s backdrop of weak demand growth and rising supply, there is a credible risk that crude prices soften from current levels. For our case, we assume a 20%-25% decline in realized oil prices, effectively testing how much margin cushion each operator retains when prices fall toward the low-$50’s WTI range. This stress test highlights which producers remain resilient and which are more vulnerable under softer market conditions.

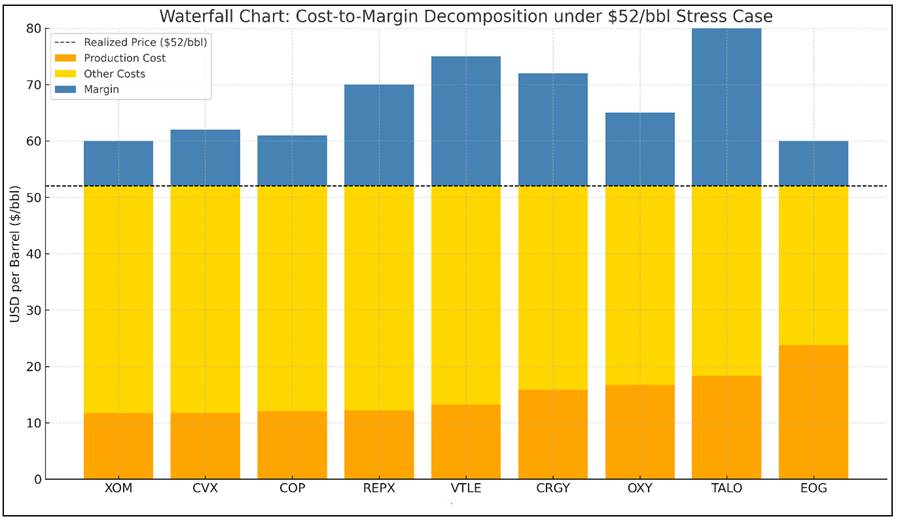

Stress-testing 1

Cost Position (against lower realized price)

Here’s the effective cost stack (Total Costs $/boe) vs realized price margin buffer:

In a low-price scenario of $50–55 crude, resilience varies sharply across producers. EOG, XOM, COP, and REPX hold the strongest cushions, helped by low operating costs and diversified assets. They remain near breakeven even as crude falls into the low $50s. XOM and CVX also gain support from downstream and chemical operations, which soften the hit from weaker upstream margins. In contrast, CRGY faces the steepest squeeze, with its cost stack nearly matching realized prices. OXY stays marginally profitable but risks single-digit margins and higher leverage pressure. VTLE can sustain operations, though with narrow $10–15/bbl cushions and limited diversification.

Key Observations

• All operators still cover basic operating costs, so existing wells keep running.

• Most producers fall below full-cycle breakevens at $52 WTI, meaning new drilling would lose money.

• The stress case pushes prices below industry half-cycle ($50–70/bbl) and new well ($65/bbl) thresholds.

• Large operators’ scale shields them for now, but sustained low prices could force spending cuts—especially for OXY and CVX, whose margins sit closest to breakeven.

Gas and NGL exposure drag realized prices below crude benchmarks, trimming margins for mixed producers.

Price Fall - Impact on Production

We dived even further and estimated a rough forecast of what would happen to production if the 20% fall in crude oil prices indeed occurred. Remember, the estimates are linked to our crude oil price production cost forecast, which combines the company’s lifting costs and total production costs based on various definitions, as Osama carefully explained in the first episode of the series. We have also borrowed from the total productions and expenses (on a per barrel basis) as described in the first part of the series.

In reality, no company (discussed in the article) explicitly reduced 2025 guidance. Our stress-related production plan model imply alignment with the model's thresholds. In a real 20% drop, small operators' conservatism would likely amplify reductions.

In conclusion, in a stress scenario, large operators (XOM, CVX, COP, EOG) will maintain 2024 production levels covering lifting costs and being close to full-cycle costs. Small operators (REPX, VTLE, CRGY, TALO) and OXY are expected to reduce production, as their margins fall significantly below full-cycle costs, limiting new drilling.

Stress-testing 2

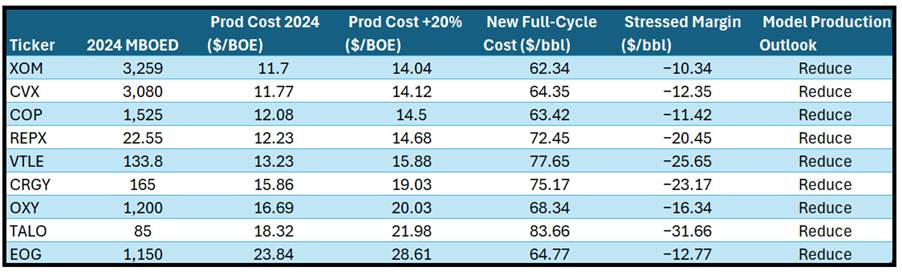

Let us test another hypothesis that shale oil production is moving from premium to less-premium acreages. There are evidences that U.S. shale oil production is moving from Tier 1 (“sweet-spot”) acreage into Tier 2/3 zones. The move entails raising production costs because of Lower well productivity, reduced recovery efficiency, and higher supporting costs. At the same time, it can lower frackers’ operating margin due to Inflation stickiness. So, it will be equally interesting to see the effect of higher operating costs when production moves places. We will assume that all components of the production costs rise by 20% from the current level, while the average realized price remains the same.

Production Impact (against higher operating costs)

At $63 crude, only XOM narrowly maintains profitability, reflecting its efficiency and scale. CVX, COP, and EOG hover near breakeven but would likely trim discretionary drilling. OXY remains under pressure due to leverage and cost inflation. Smaller independents — TALO, VTLE, CRGY, REPX — see steep margin erosion and would face immediate cutbacks in new well activity. Overall, higher costs erase nearly all cushion except for the most efficient integrated producers.

Where Does It Leave Us?

Crude prices could fall into the low $50s amid weak demand and rising supply, testing operators’ ability to stay profitable at lower realizations. In this price-driven scenario, EOG, XOM, COP, and REPX remain best positioned, while OXY, VTLE, CRGY, and TALO face thinner margins or potential losses.

Separately, if operating costs rise—such as from a shift into less-productive Tier 2 and Tier 3 acreage—industry breakevens would move higher even if prices stay steady. Larger, diversified producers could absorb this cost pressure, but smaller independents would likely scale back drilling and defer development. Taken together, the analysis shows that shale resilience depends as much on cost discipline as on price strength.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform