~1.6 MMboe/d of pro forma production is the headline outcome highlighted by the merger presentation, underscoring that this is a scale-driven platform move rather than a niche consolidation. The combined volume places a Devon–Coterra entity firmly among the largest U.S. shale producers, increasing relevance with large-cap investors and reinforcing the case for durability over short-cycle growth.

~$57 billion of pro forma enterprise value would move the company into a higher competitive tier, closer to EOG Resources and ConocoPhillips’ Lower 48 portfolio than to mid-cap shale independents. The document emphasizes that scale is not pursued for growth optics, but for capital markets positioning, balance-sheet resilience, and the ability to sustain returns across commodity cycles.

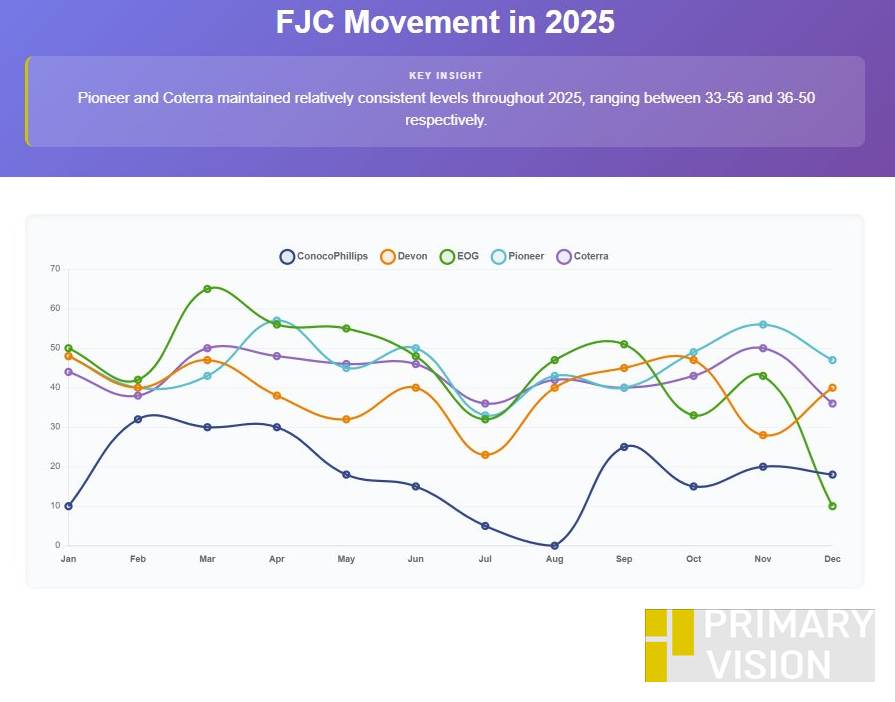

According to Primary Vision’s frac job count estimates, in 2025, Pioneer and Coterra demonstrated the most consistent performance patterns. EOG experienced notable fluctuations, particularly in the final quarter.

~863 Mboe/d of Permian (Delaware) production anchors the combined platform and represents the only basin where overlap is both material and strategic. The presentation frames this overlap as additive rather than redundant, with larger contiguous development, improved capital efficiency, and enhanced service leverage as the primary benefits. This is where operational synergies are concentrated.

Six pro forma basins: Permian, Marcellus, Anadarko, Eagle Ford, and a combined Rockies position (Williston plus Powder River)—define the operating footprint. Outside the Permian, the emphasis is not cost synergy but portfolio construction. The assets are largely complementary, expanding geographic reach and commodity exposure without meaningful duplication.

~2.0 Bcf/d of Marcellus gas production is presented as a structural stabilizer rather than a growth engine. The deck highlights gas duration and low decline as mechanisms for supporting free cash flow and capital returns during weaker oil price environments. For Devon, this materially shifts the portfolio’s risk profile; for Coterra, it preserves the value of a long-life gas asset within a larger platform.

~205 Mboe/d in the Rockies and ~63 Mboe/d in the Eagle Ford add oil-weighted diversification beyond the Permian. The presentation frames these basins as sources of optionality rather than near-term growth, reducing exposure to single-basin constraints and smoothing capital allocation decisions over time.

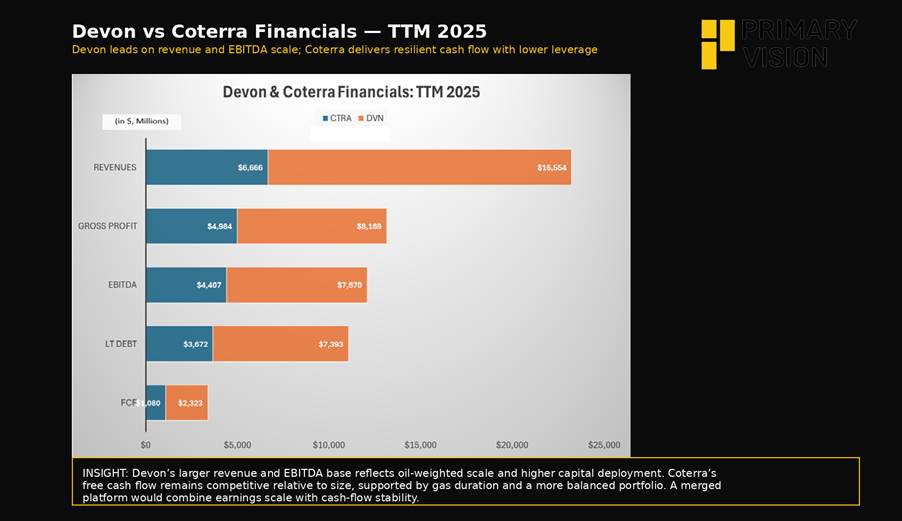

~$12–13 billion of combined EBITDA and ~$11 billion of long-term debt

This suggest manageable leverage, but the document is explicit that cost synergies outside the Permian are limited. Execution risk remains, particularly given the broader geographic footprint. The value proposition rests on disciplined capital allocation, not aggressive cost takeout.

$500 million+ of annual synergies and capital efficiencies, as implied in the pro forma narrative, are expected to come predominantly from Permian operating scale, capital optimization, and corporate efficiencies rather than aggressive cost cutting. The presentation emphasizes improved capital pacing, lower per-unit development costs in the Delaware, and streamlined corporate overhead. Importantly, it does not rely on large non-Permian cost synergies, reinforcing the supplementary nature of the combination.

Why Does The Merger Matter?

The pro forma case emphasizes scale, diversification, and capital flexibility as tools for extending shale relevance in a maturing U.S. onshore landscape. While still speculative, the presentation makes clear that this would be a platform-building merger, with success ultimately determined by valuation discipline and execution rather than asset fit alone. In an industry shifting from growth to returns, the merger matters because it prioritizes scale, durability, and cash flow stability over incremental production expansion.