Articles

- BLOG / Articles / View

- Articles

Frac Capacity Is Not Absorbed Fast Enough As Operators Tighten Capex

By Avik on April 10, 2026 in Articles

A Stabilizing Market Is Being Mistaken for a Tightening One

The U.S. pressure pumping market is no longer deteriorating, but it is also not tightening in the way many expected going into 2026. Activity has stabilized, completion schedules are becoming denser, and operators are pulling forward DUCs. However, this improvement remains incremental rather than structural. Read more about the top energy producers’ recent projects in the US shale basins in our article.

Management commentary across the sector reflects this nuance. ProFrac pointed to better utilization following delayed activity returning, but from a weak base. Patterson-UTI continues to highlight high utilization levels, yet without a meaningful increase in overall activity. Liberty Energy sees supply tightening through attrition, but pricing remains under pressure. Meanwhile, ProPetro is maintaining disciplined deployment, keeping fleets contracted rather than chasing incremental work. The direction is clearly improving. But the pace is not strong enough to force a broad tightening cycle.

Utilization Trends Suggest the Market Is Not Tight

Looking at utilization proxies across major pressure pumpers, the trend is uneven rather than reinforcing. Halliburton is the only name showing a consistent upward trajectory into late 2025, suggesting it is capturing utilization through scale, technology, and international exposure. The rest of the group tells a different story. Patterson-UTI remains largely flat, indicating stable but capped utilization. ProFrac and Liberty show a decline followed by stabilization, pointing to recovery rather than tightening. ProPetro remains volatile, reflecting contract-driven stability instead of market-driven strength.

If frac demand were rising fast enough to absorb available capacity, this strength would appear across all operators. Instead, utilization gains are selective, not systemic. This suggests that the market is improving at the margin, but not tightening in a way that would support sustained pricing power.

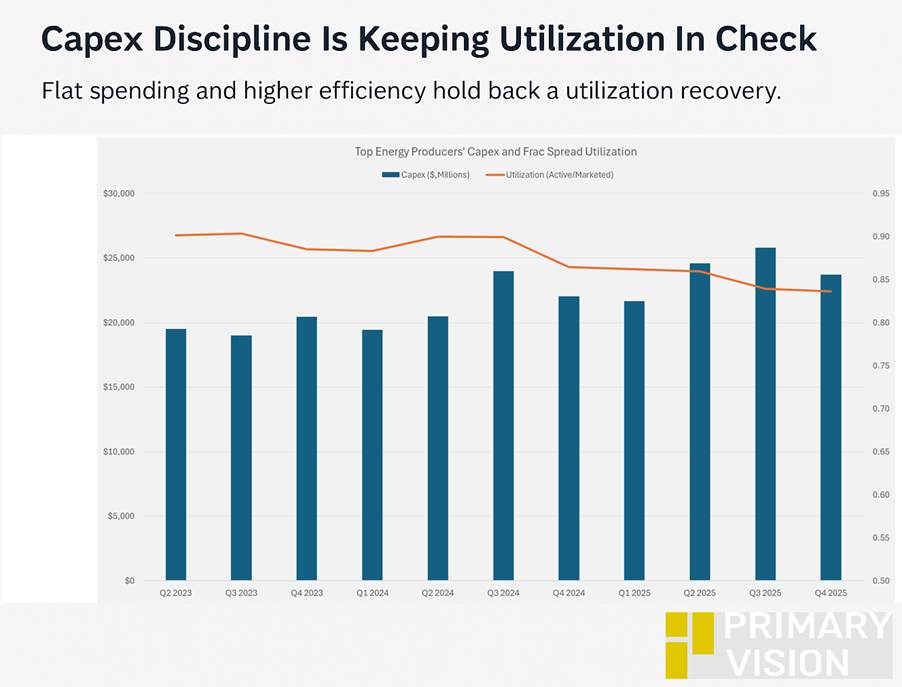

Capex Discipline Is Keeping Utilization In Check

Operator capex discipline is capping utilization. In Q4, top US energy producers’ capex decreased by 8% compared to Q3. E&Ps reduced budgets flat and reallocating within existing programs rather than increasing spending, with any activity uplift pushed into later 2026 and fleets deployed only against contracted visibility. At the same time, efficiency gains—larger fleets, higher intensity, and stable horsepower despite fewer fleets—are allowing more work to be done with the same capital. As a result, utilization is improving but not tightening meaningfully, as incremental demand is absorbed through productivity rather than additional fleet deployment.

Capacity Is Evolving, Not Shrinking

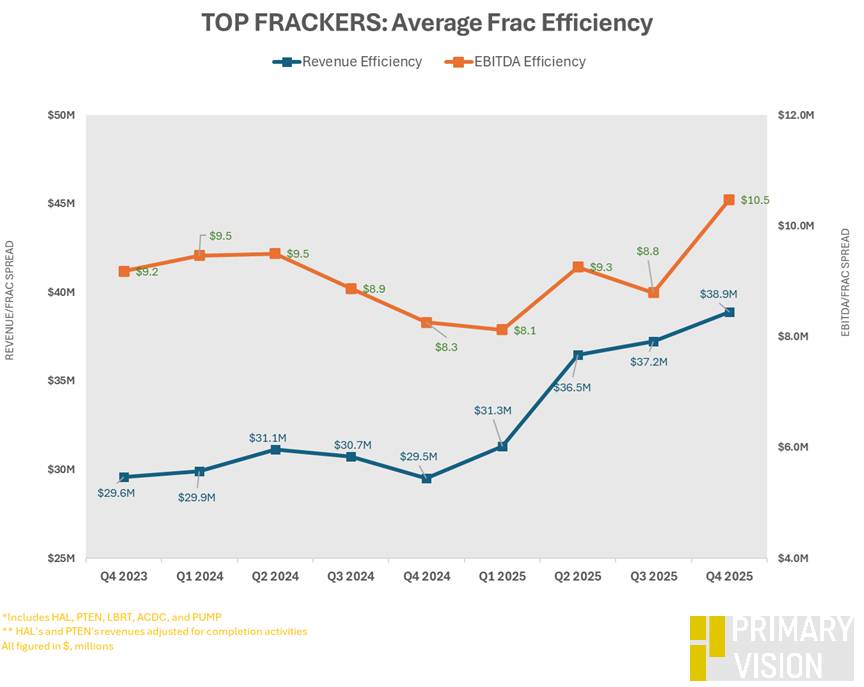

The core issue lies on the supply side. While fleet counts have declined, effective capacity has not tightened as much as expected. Patterson-UTI has emphasized that deployed horsepower remains broadly unchanged despite a reduction in fleet count. Liberty continues to highlight rising completion intensity and larger fleets per well site. ProFrac’s vertically integrated model is allowing it to offset weaker activity through efficiency gains.

The implication is straightforward. Fewer fleets are now doing more work. This shift toward higher efficiency, longer laterals, and larger fleet configurations means that capacity is not being removed from the system as quickly as headline fleet counts suggest. As a result, utilization takes longer to tighten, even as activity stabilizes.

A Two-Tier Market Is Emerging

Rather than a broad recovery, the market is splitting into two distinct segments. High-spec fleets—particularly Tier IV, dual-fuel, and electric equipment—are seeing strong utilization and relatively stable pricing. These fleets benefit from fuel efficiency, automation, and customer preference for lower-cost, lower-emission operations.

In contrast, legacy fleets remain underutilized and continue to face pricing pressure. Much of the reported attrition is concentrated in this segment, but it has not yet been sufficient to rebalance the market.

This bifurcation explains the divergence in company commentary. Some operators are experiencing tight utilization, while others continue to operate in a soft pricing environment. Both views are valid, but they reflect different parts of the same market structure.

Margins Are Being Defended, Not Driven Higher

This uneven utilization backdrop is directly impacting margins across the group. Halliburton is better positioned due to its international exposure and technology differentiation, allowing it to capture stronger margins where activity is less commoditized. Patterson-UTI is operating with high utilization, but limited incremental demand is capping margin expansion. ProFrac continues to rely on efficiency gains to support profitability, but a stronger utilization recovery is still needed for meaningful upside.

Liberty’s structural positioning is improving, but near-term pricing pressure continues to weigh on earnings. ProPetro is maintaining margin stability through contracts and capital discipline rather than relying on a tightening market. Across the sector, the pattern is consistent. Margins are stabilizing, but they are not expanding in a meaningful way.

Takeaway

The pressure pumping market is improving, but not tightening fast enough to absorb evolving frac capacity. Efficiency gains and fleet high-grading are keeping effective supply elevated, even as headline fleet counts decline. This is delaying a broader utilization inflection and limiting pricing power.

However, a clear bifurcation is emerging between high-spec and legacy fleets, with utilization strength concentrated in premium equipment. I think margins will remain range-bound in the near term, with any meaningful expansion dependent on a stronger demand recovery rather than further supply attrition.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform