Articles

- BLOG / Articles / View

- Articles

From AI to Oilfield Power: The AI Company

By Avik on July 3, 2026 in Articles

Mapping the Hyperscalers in AI Economy

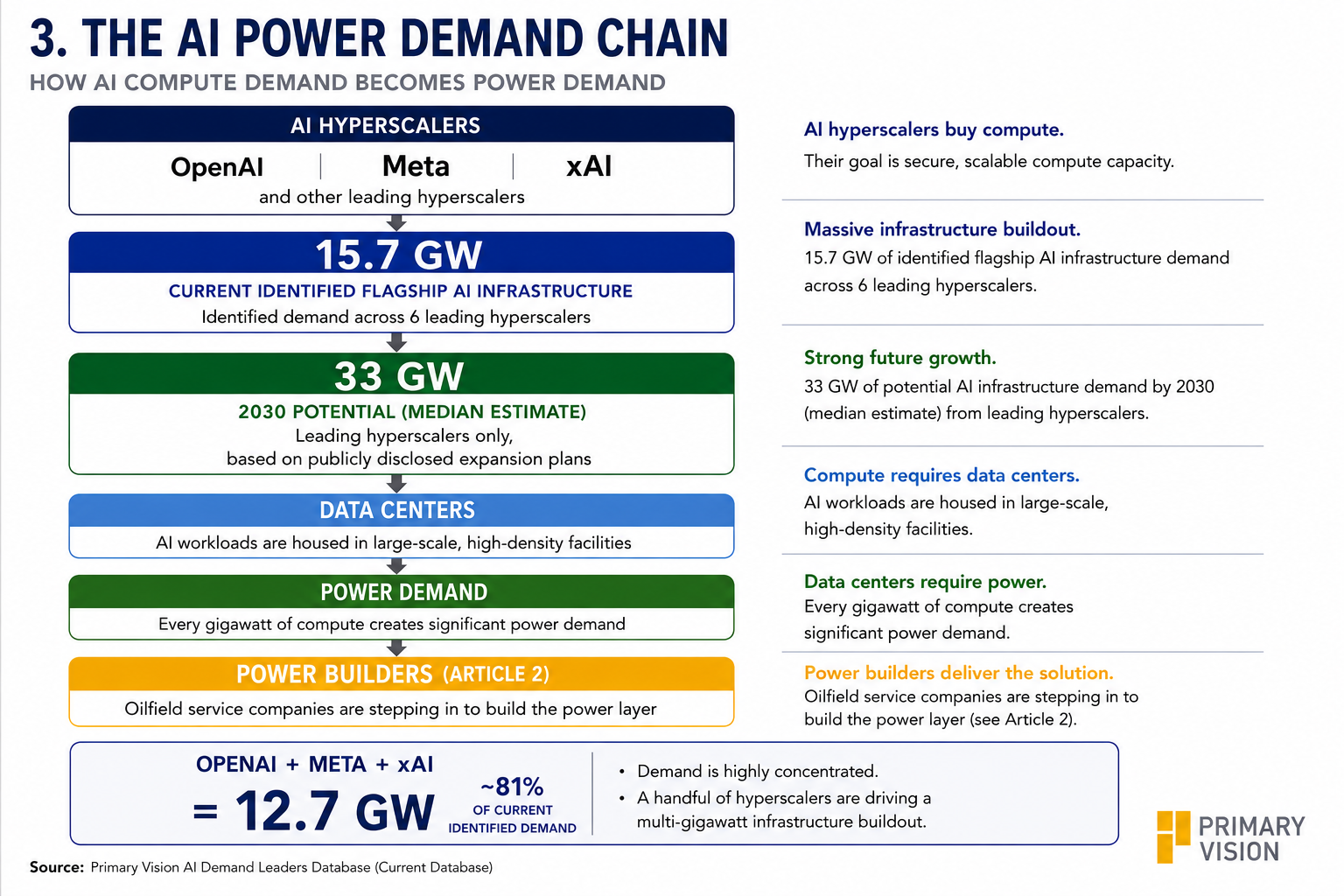

The first article in this series introduced the AI Power Stack and the growing electricity requirements associated with artificial intelligence. The next question is straightforward: who is actually creating that demand?

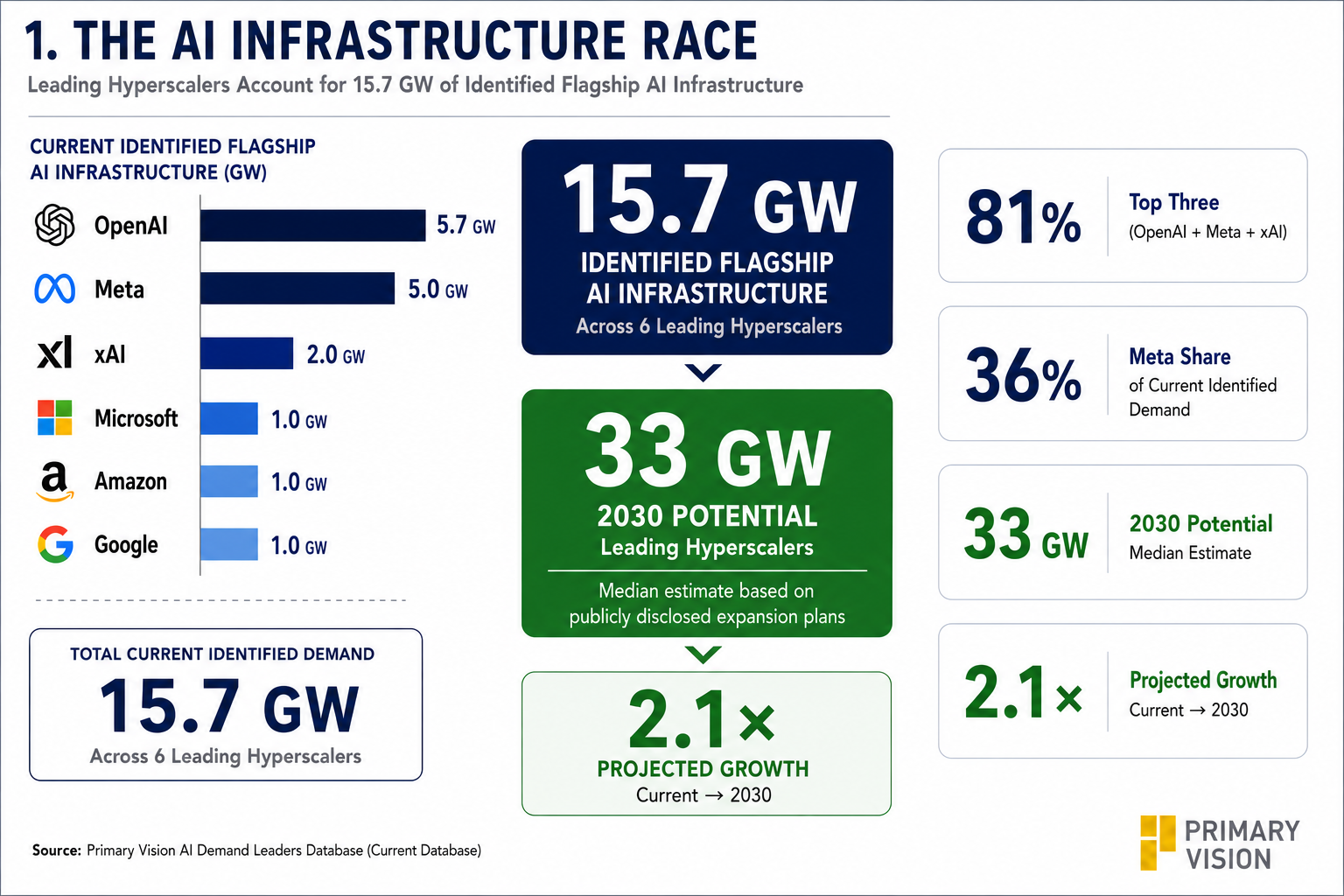

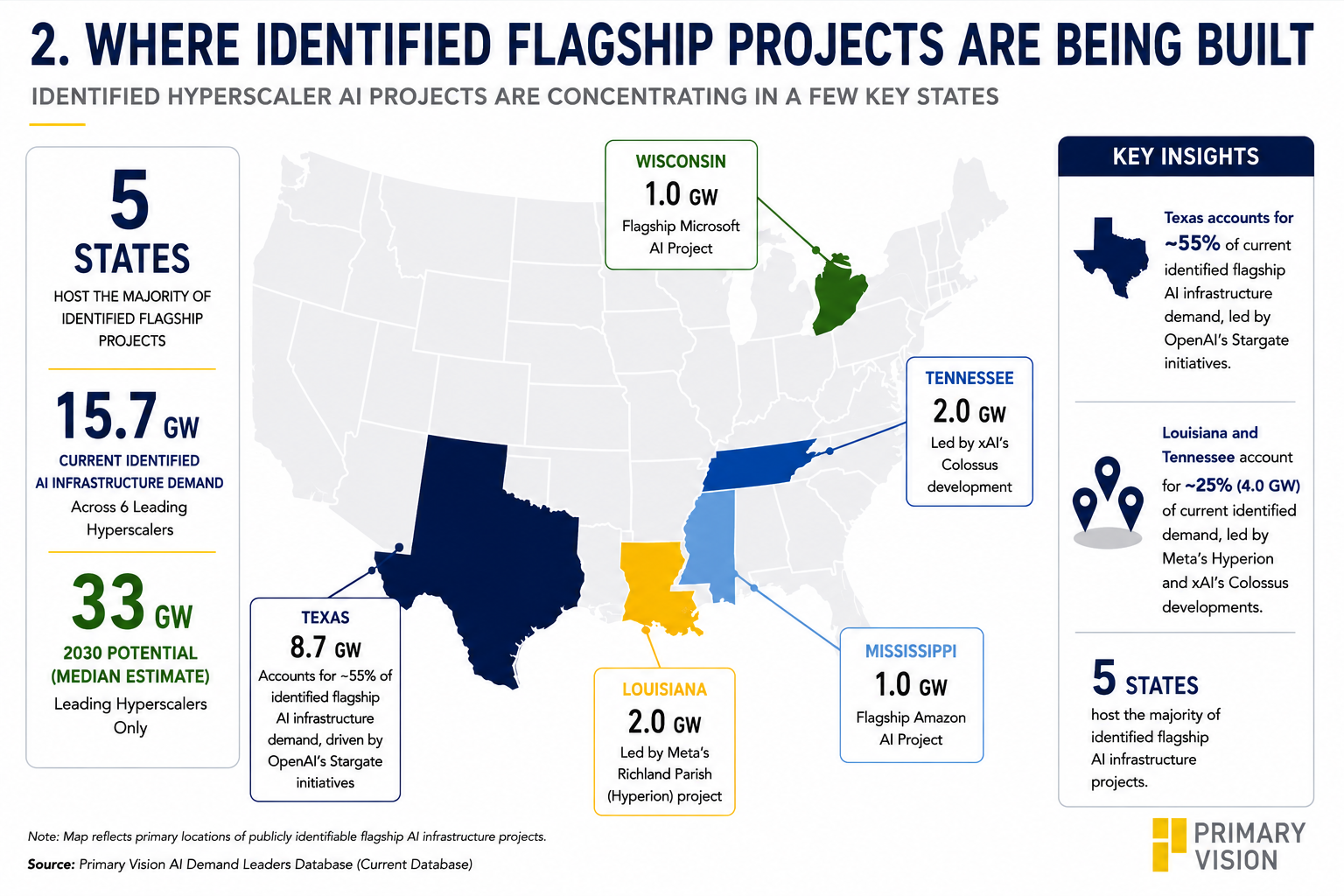

To answer that question, Primary Vision built the AI Demand Leaders Database, which tracks flagship AI infrastructure projects announced by leading AI developers and hyperscalers. The current database identifies approximately 15.7 GW of publicly identifiable flagship AI infrastructure demand across six leading hyperscalers.

Publicly disclosed expansion plans suggest this identifiable demand could increase to approximately 33 GW by 2030. The database intentionally focuses on flagship projects with identifiable company attribution and excludes utility load forecasts, interconnection queues, and undisclosed developments to minimize double counting.

Our Hyper Universe

We are considering OpenAI, xAI, Anthropic, Meta, Microsoft, Amazon, and Google. The findings suggest that AI infrastructure demand is highly concentrated. A handful of companies are driving a multi-gigawatt buildout that increasingly resembles industrial infrastructure rather than traditional data-center development.

*Primary Vision's AI Demand Leaders Database intentionally tracks only publicly identifiable flagship AI infrastructure projects sponsored by leading hyperscalers. While the current database identifies 15.7 GW of hyperscaler demand, total U.S. AI-related power demand is likely to be substantially larger when enterprise AI deployments, colocation providers, GPU cloud operators, sovereign AI projects, and undisclosed developments are included.

OpenAI Is Setting The Pace

OpenAI accounts for the largest identified infrastructure pipeline in the database. The centerpiece is Stargate, a joint initiative involving OpenAI, Oracle, and SoftBank. The flagship Abilene, Texas campus is expected to support approximately 1.2 GW of capacity when fully developed. Beyond Abilene, OpenAI and Oracle have announced plans for an additional 4.5 GW of U.S. AI infrastructure capacity.

Combined, OpenAI’s disclosed infrastructure pipeline totals roughly 5.7 GW. That figure alone exceeds the peak demand of many regional utility systems and highlights the scale of compute capacity required to support future model training and inference workloads.

xAI And Meta Are Building At Gigawatt Scale

Elon Musk’s xAI has rapidly emerged as another major source of infrastructure demand. The company’s Colossus facility in Tennessee currently represents roughly 300 MW of operating capacity. Expansion plans could add another 1.2 GW, bringing the identified xAI pipeline to approximately 1.5 GW.

Meta is pursuing an equally aggressive strategy. The company’s Richland Parish development in Louisiana serves as the foundation of its Hyperion AI infrastructure initiative. Current plans point to approximately 2 GW of compute capacity, placing the project among the largest AI-focused developments announced to date. Taken together, OpenAI, Meta, and xAI account for approximately 12.7 GW of identified flagship AI infrastructure demand, representing roughly 81% of the current database.

The Hyperscalers Continue To Expand

Microsoft, Amazon, and Google remain critical participants in the AI infrastructure race. Each contributes approximately 1 GW of identifiable flagship AI infrastructure demand. While individually smaller than the largest OpenAI and Meta developments, together they account for another 3 GW of current identified demand and reinforce the breadth of hyperscaler investment across the AI ecosystem. Anthropic is more difficult to isolate because much of its infrastructure is embedded within AWS deployments. Nevertheless, the company’s growth continues to contribute to demand for large-scale AI compute infrastructure.

Demand Is Becoming Geographically Concentrated

The database also highlights the emergence of several key AI infrastructure hubs. Texas leads the identified pipeline, driven primarily by Stargate. Tennessee has become a major center through xAI’s Colossus development. Louisiana has emerged as another focal point through Meta’s Richland Parish project. Additional investments are occurring in Wisconsin, Mississippi, and other regions with access to power, land, and supporting infrastructure.

The geographic concentration is notable because these same regions increasingly sit at the intersection of natural gas supply, power generation, and industrial development. As AI infrastructure scales, local power availability is becoming just as important as access to GPUs and computing hardware.

Demand Is Beginning To Reach The Power Layer

The 15.7 GW identified in Primary Vision's AI Demand Leaders Database is no longer simply a data-center story. More importantly, publicly disclosed expansion plans suggest identifiable hyperscaler demand could increase to approximately 33 GW by 2030. The industry is transitioning from isolated gigawatt-scale campuses to a multi-decade buildout of AI power infrastructure.

At this scale, power procurement is becoming as strategically important as compute procurement. Multi-gigawatt campuses increasingly require dedicated generation, behind-the-meter power solutions, natural gas supply, and long-term power contracts. The bottleneck is no longer just GPUs—it is increasingly the ability to secure reliable electricity at scale.

Key Takeaway

The AI infrastructure race is entering a new phase. Primary Vision currently identifies 15.7 GW of flagship AI infrastructure demand across six leading hyperscalers, with publicly disclosed expansion plans pointing to approximately 33 GW by 2030. The first direct links between hyperscalers and the emerging OFS power ecosystem are already appearing. The question is no longer whether AI will create power demand—it is who can build and supply power infrastructure fast enough to support the next generation of AI campuses.

That question leads directly to the next article in this series, which examines how oilfield service companies are leveraging excess horsepower, power-generation expertise, and existing infrastructure to become some of the earliest builders of the AI power layer.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform