Articles

- BLOG / Articles / View

- Articles

Halliburton's Perspective in Q4 2025: KEY Takeaways

By Avik on January 30, 2026 in Articles

Industry Outlook

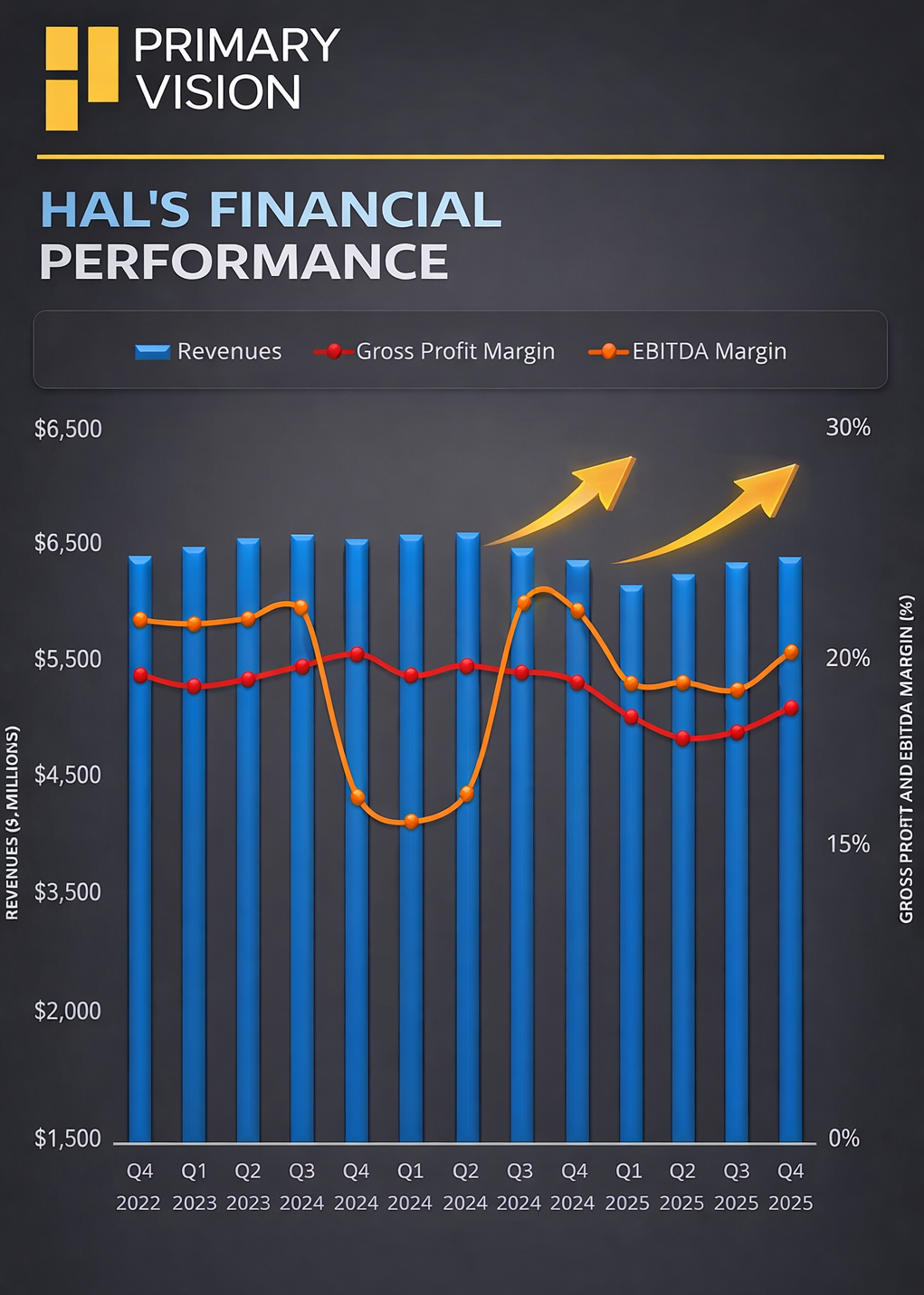

We have already discussed Halliburton's (HAL) Q4 2025 financial performance in our recent article. In the call, 2026 looks like a year of rebalancing to HAL’s management. It should have ample supply from OPEC and non-OPEC and limited upside for commodity prices in the near term. Expect some softness in North America, while international activity should stay broadly stable.

Over the medium term, tightening fundamentals should return as decline rates rise, reservoir quality worsens, and exploration remains limited, with the next cycle likely starting again in North America. Capex is guided at about $1.1 billion for 2026 (excluding any potential spending tied to Venezuela), which is lower than the $1.25B spent in FY2025.

North America and Frac Outlook

Halliburton expects North America revenue to decline “high single digits” in 2026 due to weaker land activity, fleet stacking, and program timing. Attrition is rising while investment is falling. A small demand recovery would tighten the market quickly, so the strategy is to prioritize returns over market share and focus on technology that improves recovery and enables longer, faster, more precise wells.

Uneconomic equipment will continue to be stacked to preserve value and support both a North American recovery and international unconventional growth. Despite that, the company’s ZEUS performed strongly because it directly measures and automates sand placement during fracking. An 18% increase in adoption in Q4 shows the technology is working. iCruise and LOGIX are benefiting from the industry shift toward longer laterals and more complex well geometries across every basin. Despite the decline in rig count, drilling services still grew meaningfully in recent times.

International Market Outlook

HAL’s management thinks that international growth is being driven by unconventionals, drilling, production services, and artificial lift. This is where Halliburton appears positioned to outperform. North American technology is now scaling internationally, with operations across countries. On top of that, the rising adoption of simul-frac, continuous pumping, auto frac, and Sensori is helping the process. The company’s artificial lift performance has been outstanding.

The management’s 2026 outlook is “flat to modest” growth, but collaboration with independents, IOCs, and NOCs is increasingly a competitive advantage. I think the market structure is shifting toward unconventionals, development drilling, and intervention, which directly plays to Halliburton’s strengths.

Power Business Growth

In Q4, Halliburton and VoltaGrid secured 400 MW of modular power manufacturing capacity. This strengthens the case for a meaningful future growth opportunities. Halliburton holds about 20% of VoltaGrid, which secured a 2.3-gigawatt power deal supporting Oracle’s AI data centers. Halliburton also partner with VoltaGrid internationally to deliver data center power projects.

Segment Forecast

In Q1 2026, Halliburton expects the Completion and Production revenue to decline 7%–9% due to lower international activity. Operating margins may compress by up to 300 basis points. In Drilling and Evaluation, revenue can decrease by 2%-4% with margins deteriorating by 25–75 basis points.

Relative Valuation

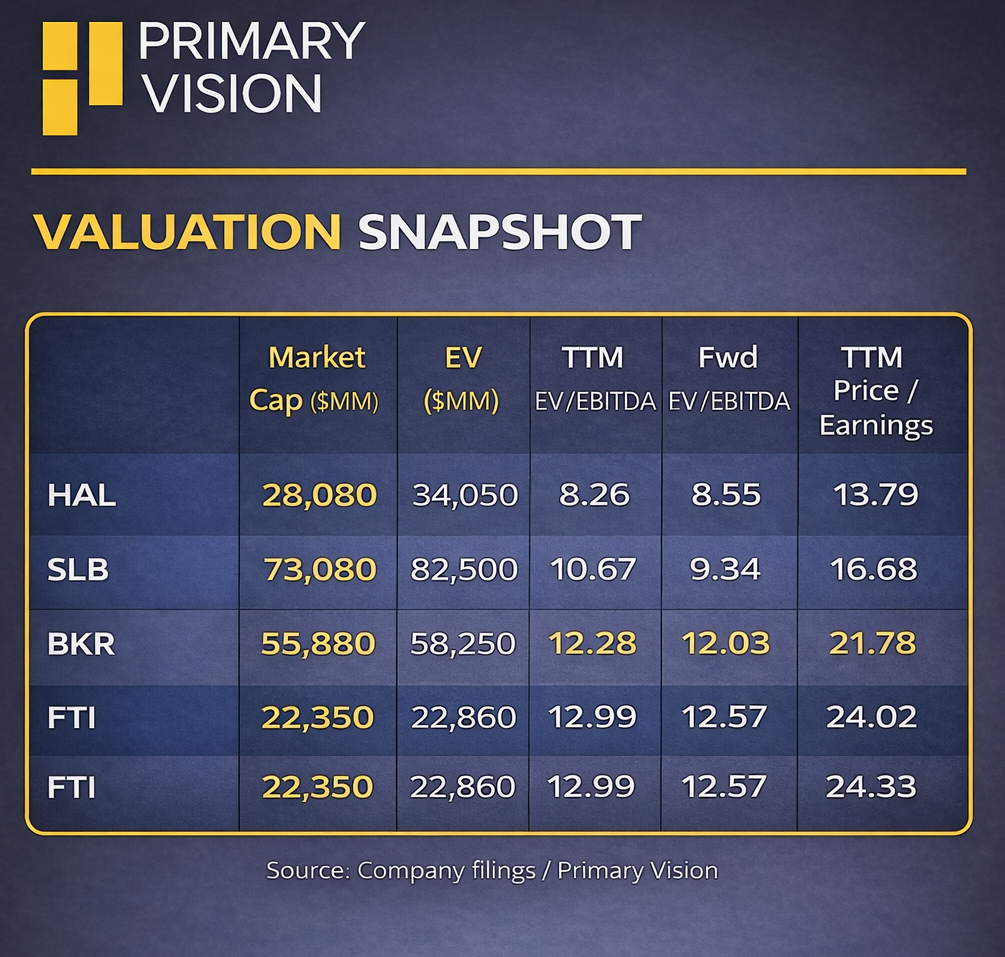

Halliburton is currently trading at an EV/EBITDA multiple of 8.3x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is higher. The current multiple is lower than its five-year average EV/EBITDA multiple of 10.2x.

HAL's forward EV/EBITDA multiple expansion versus the adjusted current EV/EBITDA contrasts a decline in the multiple for its peers because the company's EBITDA is expected to decline versus a rise in EBITDA for its peers in the next four quarters. This typically results in a much lower EV/EBITDA multiple than peers. The stock's EV/EBITDA multiple is lower than its peers' (SLB, BKR, and FTI) average. So, the stock is reasonably valued versus its peers.

Final Commentary

Halliburton’s outlook reflects near-term price pressure, softer North America activity, and broadly stable international demand. Medium-term fundamentals can tighten again. However, the next upcycle is likely starting in North America. Halliburton is by stacking uneconomic fleets and prioritizing returns, while differentiated technologies like ZEUS, iCruise, and LOGIX continue to gain traction.

International remains the structural growth engine, supported by unconventionals, drilling, artificial lift, and deeper collaboration with IOCs and NOCs. New growth options such as modular power, alongside cautious capex and weaker near-term segment margins, frame a mixed but strategically improving setup. The stock is reasonably valued compared to its peers.Bottom of Form

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform