Short and Medium-term Outlook

Our short article discussed our initial thoughts about KLX Energy Services' (KLXE) Q4 2025 performance a few days ago. KLXE’s management expects Q1 to be the weakest quarter due to seasonal budget resets, slower completion restarts, and weather disruptions. Activity is expected to improve gradually after Q1, led primarily by gas-directed basins.

The company sees momentum in the Northeast Mid-Con and other gas-focused regions. In oil basins like the Permian, the strategy is to rightsize costs while maintaining flexibility for recovery. Overall, 2026 revenue is expected to be flat to slightly higher than 2025, with improvement weighted toward 2H 2026.

Current Strategy and Refrac Market

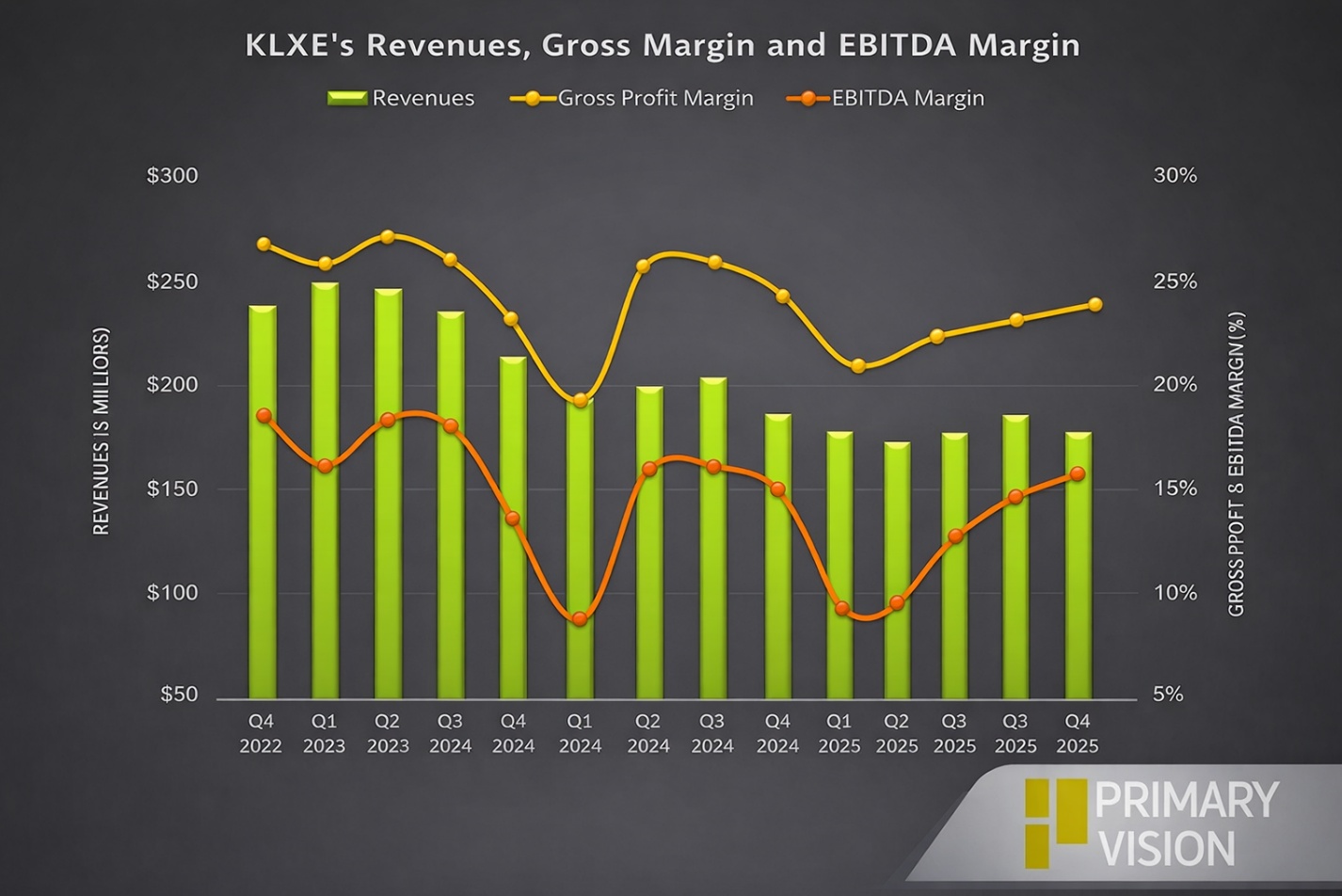

KLX continues to focus on higher-margin, technically differentiated services while maintaining strict cost discipline and selective capital deployment. The Northeast Mid-Con segment was the standout performer, with flat sequential revenue and expanding margins despite seasonal headwinds. Growth was driven by strong gas-directed demand, with dry gas revenue rising both quarter-over-quarter and year-over-year.

Refrac activity in the Bakken and, to a lesser extent, the Eagle Ford slowed through 2025. KLX is closely monitoring customer plans and commodity market developments tied to Middle East disruptions. The company believes its asset base and technology position it to respond quickly if refrac activity ramps.

Geographic Challenges and Strengths

Rockies and Southwest operations faced headwinds from severe weather, customer budget exhaustion, and lower oil-directed activity in the Permian. Despite these challenges, Southwest margins improved as the company optimized its product and service mix.

In the Mid-Con, adoption of simul-frac has been slower compared to other basins. Factors such as acreage profile, smaller operators, pad size, and limited electrical infrastructure have constrained wider adoption. Even so, simul-frac activity is gradually increasing and is expected to reach roughly 25–30% of stage counts this year.

Relative Valuation

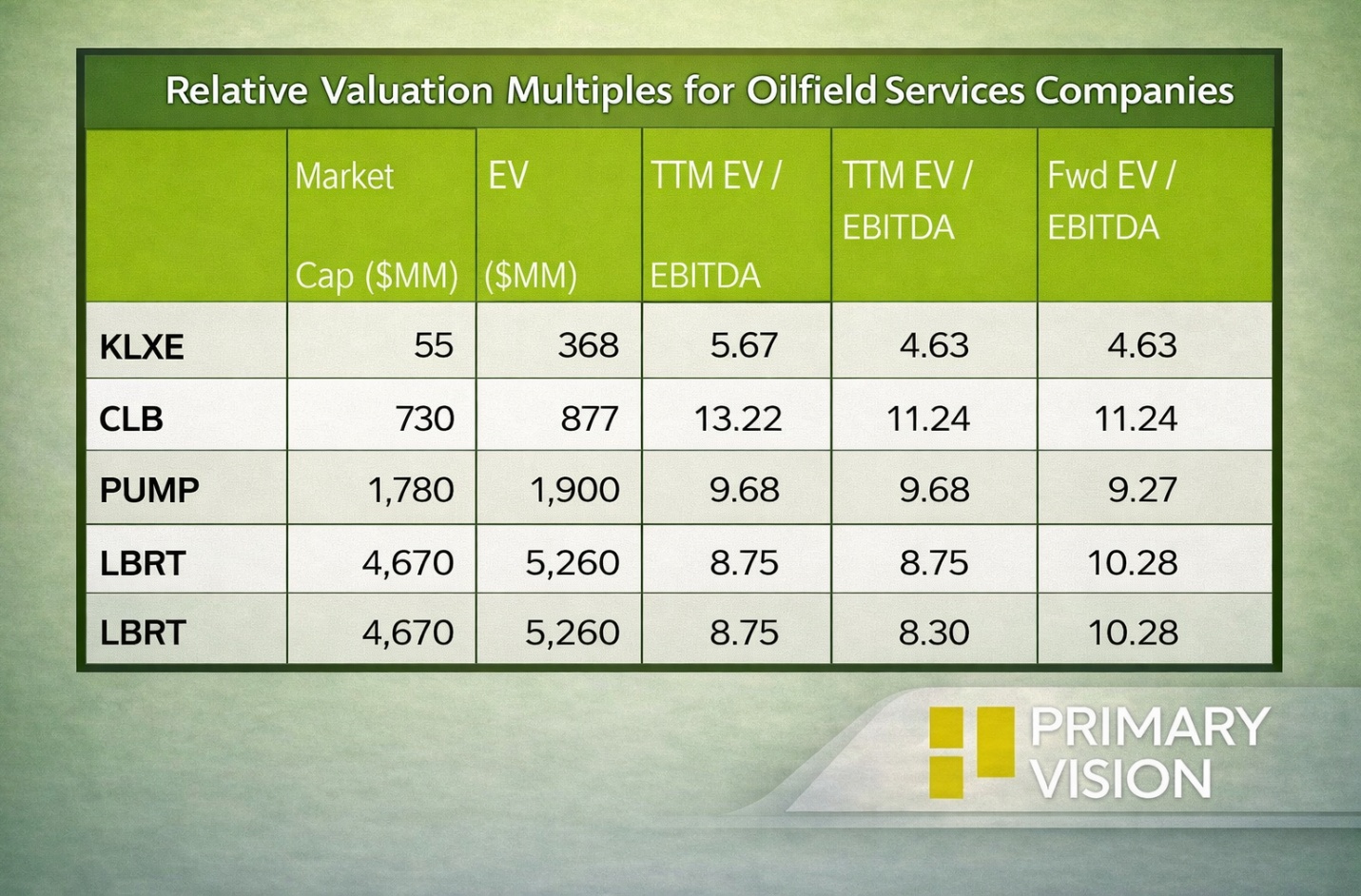

KLXE is currently trading at an EV/EBITDA multiple of 5.7x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is lower (4.6x).

KLXE's forward EV/EBITDA multiple contraction versus the current EV/EBITDA is much steeper than its peers because its EBITDA is expected to decrease more sharply than its peers in the next year. This typically results in a higher EV/EBITDA multiple than its peers. The stock's EV/EBITDA multiple is lower than its peers' (CLB, PUMP, and LBRT) average. So, the stock is undervalued compared to its peers.

Final Commentary

KLX is navigating a soft near-term environment but positioning itself for gradual improvement through 2026. Activity is expected to recover after a weak Q1, led primarily by gas-directed basins such as the Northeast Mid-Con. The company is emphasizing higher-margin, technically differentiated services while maintaining strict cost discipline.

However, oil-directed markets like the Permian remain subdued, and refrac activity in the Bakken and Eagle Ford slowed through 2025. Overall, I believe KLX’s gas exposure, improving margins, and operational flexibility should help it benefit as activity gradually recovers.. The stock is relatively undervalued compared to its peers.