Outlook Signals Gas-Driven Strength: KLX’s (KLXE) management highlighted growing demand from gas-focused work, particularly in the Northeast/Mid-Con region. The company noted that capacity rationalization across the oilfield services sector and stronger dry-gas exposure helped expand margins late in the year. While winter weather and storm disruptions are expected to soften activity in early 2026, management expects the company to return to the stronger operational run-rate achieved in 2H 2025 as the year progresses.

Revenue and EBITDA Margin in Q4:

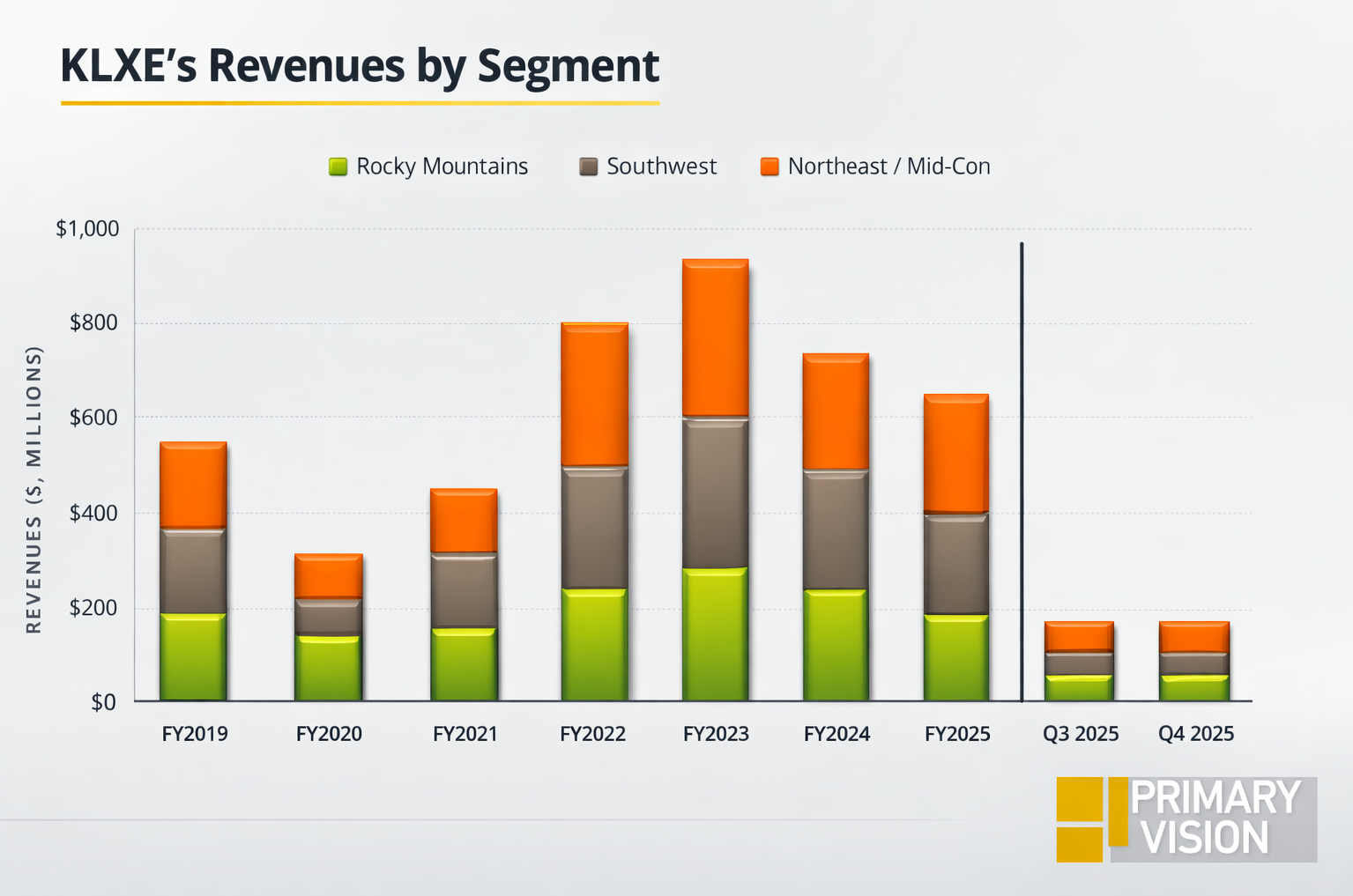

Its Q4 revenue declined sequentially due to seasonal slowdowns across several regions. Rocky Mountains revenue fell 9% quarter-over-quarter, reflecting reduced completions and intervention activity during the holiday period. Southwest revenue declined 10% sequentially, also driven by year-end budget exhaustion and reduced frac-related activity.

In contrast, the Northeast/Mid-Con segment remained resilient, with revenue rising slightly quarter-over-quarter as natural-gas-focused work offset seasonal declines in coiled tubing and frac rental activity. Overall, stronger gas-weighted activity and operational efficiency helped lift adjusted EBITDA and margins despite lower revenue.

FCF Negative; LT Debt Decreased: KLXE’s free cash flow turned steeply negative in FY2025 compared to a year ago, reflecting weaker operating cash flow and ongoing capital spending. Liquidity remains limited as cash & equivalents nearly evaporated in FY2025. Long-term debt declined by 11%, while shareholders’ equity remains negative due to accumulated losses. This highlights the importance of sustained activity and margin improvement to strengthen financial flexibility going forward.

Thanks for reading the KLXE Take Three, designed to give you three critical takeaways from KLXE's earnings report. Soon, we will present a second update on KLXE's earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.