Articles

- BLOG / Articles / View

- Articles

Liberty Energy's Perspective in Q4 2025: KEY Takeaways

By Avik on February 23, 2026 in Articles

Industry Outlook

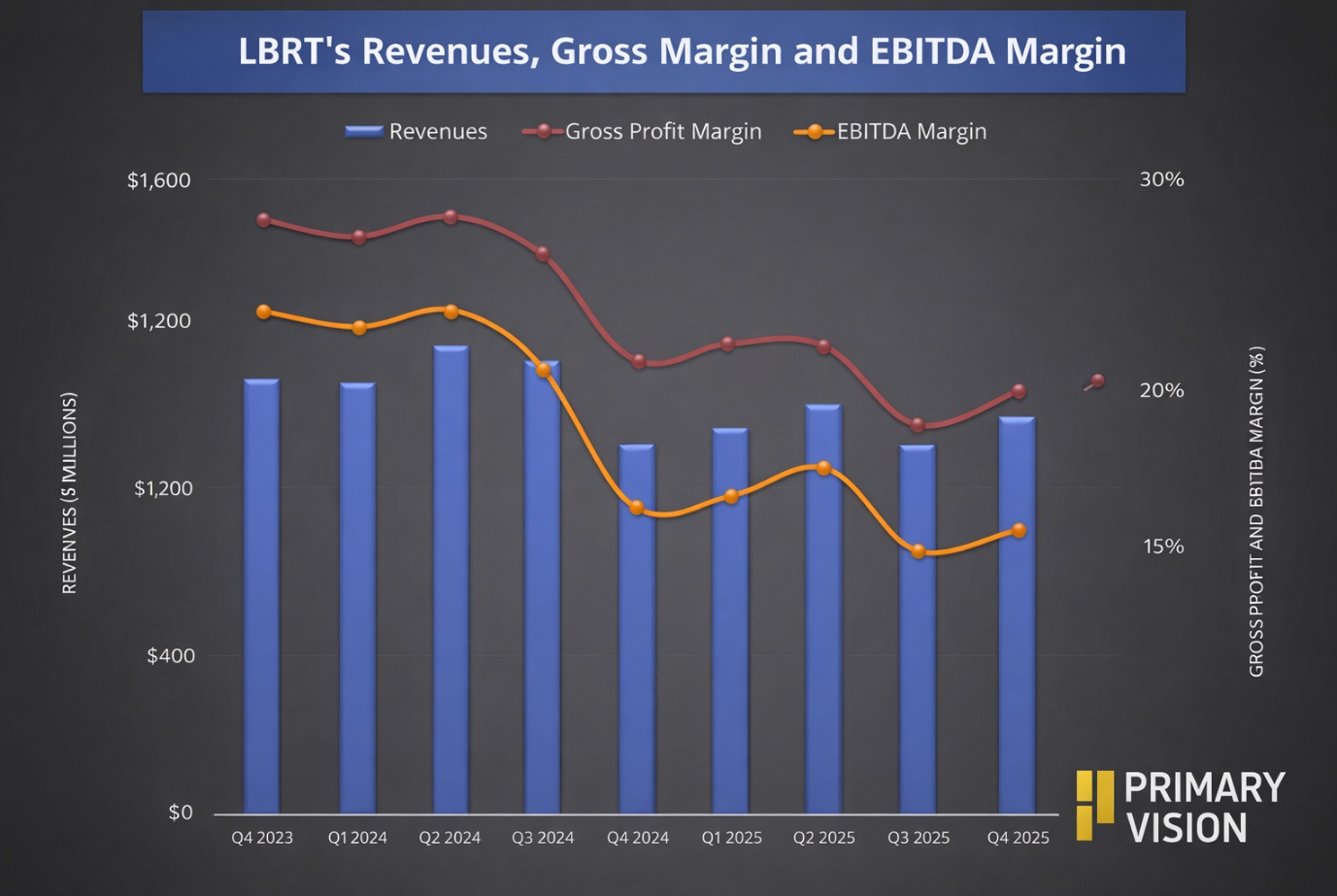

We have already discussed Liberty Energy's (LBRT) Q4 2025 financial performance in our recent article. Here is an outline of its industry outlook. LBRT’s management expects completions demand to hold firm in 2026, with flat oil production and modest growth in gas activity in North America. Oil prices remain range-bound due to surplus supply, geopolitical risk, and OPEC+ restraint, while natural gas is supported by LNG exports and rising power demand.

Pricing pressure and slower activity have accelerated equipment attrition and cannibalization, while underinvestment has limited replacement capacity. As the market recalibrates, fewer crews are available, raising the risk of tightness if demand improves. Against this backdrop, operators are pushing harder on efficiency and engineering solutions to lower unit costs.

Frac Utilization Drivers

Liberty’s launch of Atlas and Atlas IQ directly addresses this need by using real-time data and AI-driven insights to improve decision-making and operational performance. The management has identified that rising intensity, larger fleets, and customer push toward continuous pumping drive the current fleet utilization. As operators move into deeper, higher-pressure plays like the Western Haynesville, horsepower requirements and on-site complexity continue to increase. Liberty looks to offset these pressures by efficiency gains from AI, software, and digiTechnologies across operations and maintenance.

Top of Form

Bottom of Form

Power Solutions Business Outlook

LPI’s Power-as-a-Service platform is becoming a core growth pillar, offering resilient, flexible, and cost-competitive distributed power solutions. In the near term, it signed agreements with data center customers anchor deliveries beginning in 2027. According to the management estimates, data center demand for power is projected to grow threefold by 2030.

In this environment, management’s short-term goal is to scale execution while supporting rising U.S. power demand driven by AI, onshoring of manufacturing, and electrification. Grid constraints and long interconnection queues are increasing the value of LPI’s distributed power model. Over the longer term, the company aims to monetize 3 gigawatts of power by 2029 through a growing project pipeline.

Company Outlook

For Liberty Energy, FY2026 revenue is expected to be roughly flat, as higher fleet utilization is offset by industry pricing headwinds and higher costs tied to the power business buildout. Liberty expects adjusted EBITDA to decline near term due to $15M–$20M of incremental overhead and development spending for its distributed power solutions business.

Over time, frac fleet attrition should tighten supply and create an opportunity for pricing improvement. Completions capex moderates to about $250 million, with continued investment in digiFleets supported by a superior economic profile. The LPI power business carries a longer-duration earnings profile, with equipment deliveries and project spending largely supported by project financing.

Relative Valuation

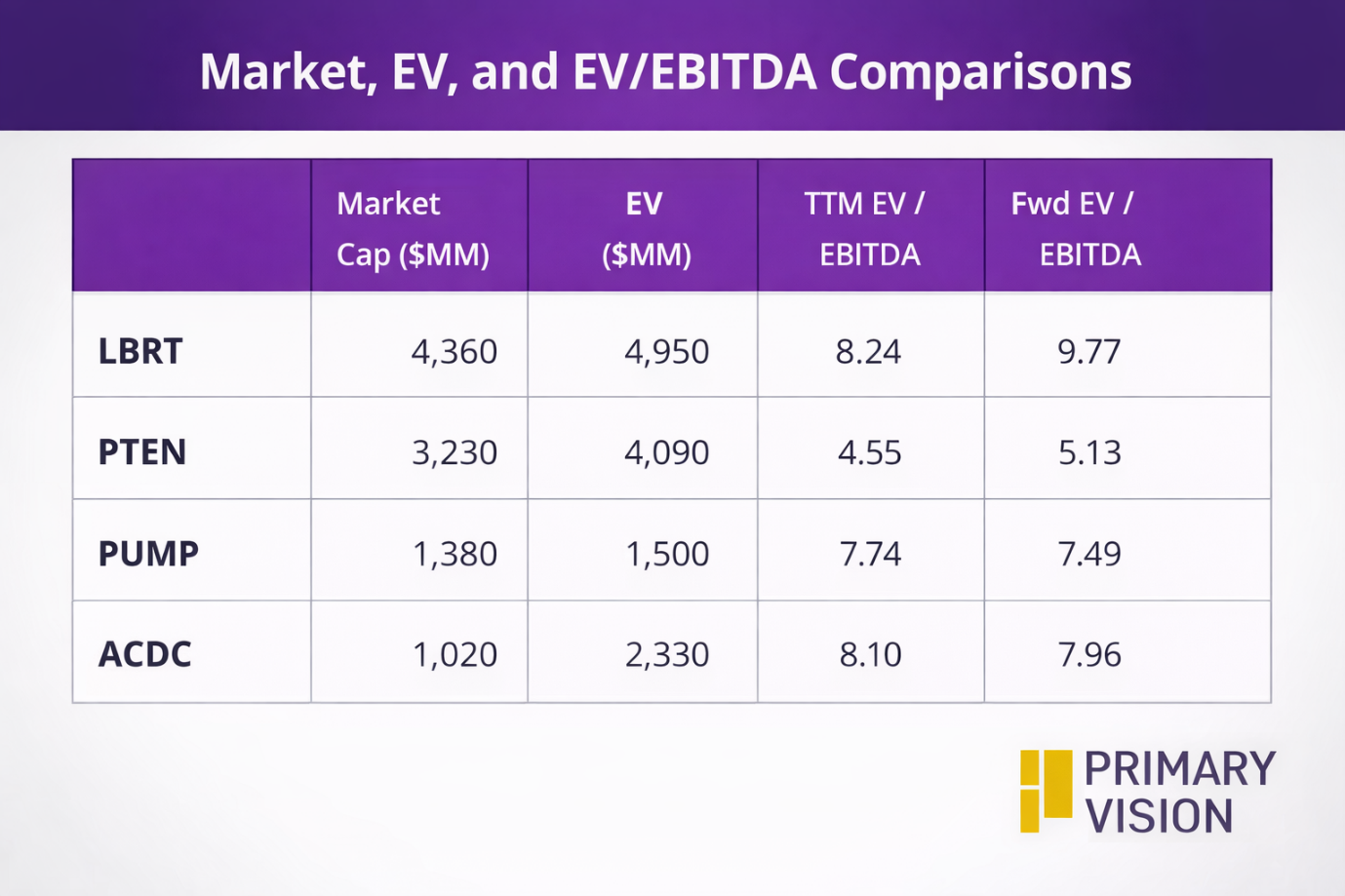

Liberty is currently trading at an EV/EBITDA multiple of 8.2x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is higher. The current multiple is lower than its five-year average EV/EBITDA multiple of 13.2x.

LBRT's forward EV/EBITDA multiple expansion versus the current EV/EBITDA is higher than its peers because the company's EBITDA is expected to decline more steeply than its peers in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock's EV/EBITDA multiple is higher than its peers' (PTEN, PUMP, and ACDC) average of 6.8x. So, the stock appears to be overvalued compared to its peers.

Final Commentary

LBRT views that the completions demand is expected to hold firm in 2026. However, pricing pressure and range-bound oil prices will keep near-term industry conditions tight. Equipment attrition and underinvestment are reducing available frac capacity, which raises the risk of market tightness if demand improves. Liberty is responding by emphasizing efficiency. The company’s Atlas IQ and digiTechnologies can help offset rising intensity and larger fleet requirements.

The power solutions business is emerging as a meaningful growth pillar, supported by accelerating data center demand and a clear execution runway into 2027 and beyond. Near-term financials remain constrained, but tightening frac supply and long-duration power projects improve the medium- to long-term setup. Compared to its peers, the stock appears overvalued.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform