Outlook for 2026: Liberty expects near-term softness in North American completions to persist into early 2026, reflecting producer discipline, pricing pressure, and underutilized fleets. Management expects market conditions to stabilize as equipment attrition accelerates and supply-demand balance gradually improves.

Liberty advanced its power platform with concrete data center commitments. The company signed an agreement with Vantage Data Centers to develop at least 1 GW of utility-scale power capacity, anchored by a firm 400 MW reservation for delivery in 2027. In addition, Liberty entered a preliminary ESA with another leading data center developer for a 330 MW project in Texas, expected to come online in phases in late 2027 and mid-2028. It reinforces power as a scalable, long-duration growth opportunity for LBRT tied to hyperscale demand.

Market Dynamics: Weak industry activity and excess capacity continue to weigh on frac pricing, particularly for legacy fleets. However, sustained underutilization is accelerating cannibalization and attrition, tightening effective supply over time. Liberty’s digiTechnologies fleets continue to see stronger demand due to efficiency, fuel savings, and emissions performance, reinforcing a widening gap between premium and conventional equipment. The ongoing “flight to quality” favors technologically advanced operators as customers prioritize cost efficiency and execution reliability.

Topline and Bottomline In Q4

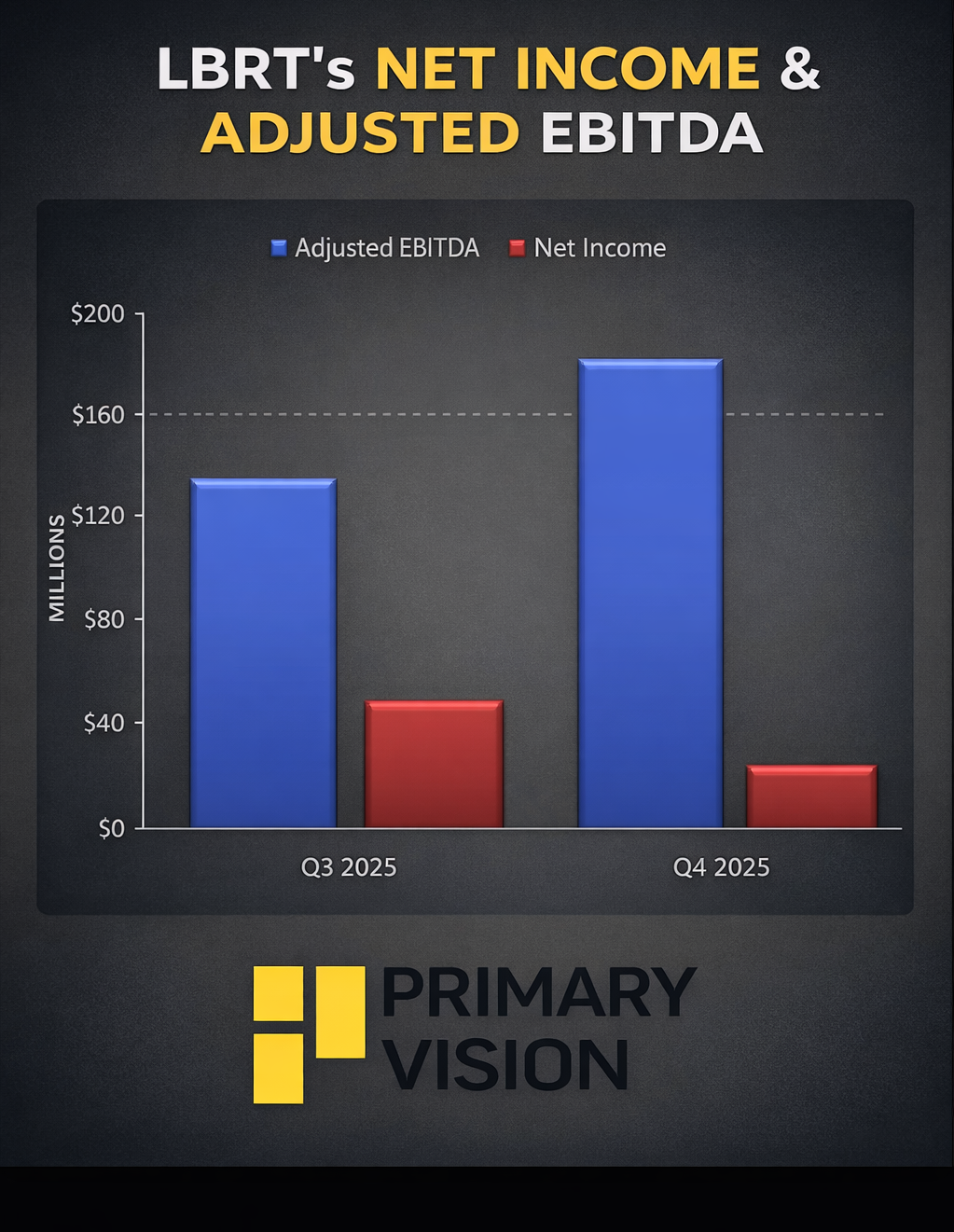

LBRT's revenue increased 10% sequentially in Q4, reflecting steadier completions activity than typically seen seasonally, while adjusted EBITDA rose 23% sequentially. On a full-year basis, revenue declined 7% year over year, and adjusted EBITDA fell 31%, reflecting lower activity levels, pricing pressure, and margin compression. Net income for Q4 declined sharply compared to a quarter earlier, underscoring the cyclical impact of weaker completions markets despite operational efficiencies.

In FY2025, Liberty’s net debt increased by 28% compared to FY2024. Leverage deteriorated modestly in FY2025, as debt and shareholders’ equity both increased. Liquidity of $281 million remained adequate.

Thanks for reading the LBRT Take Three, designed to give you three critical takeaways from LBRT's earnings report. Soon, we will present a second update on LBRT's earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.