Articles

- BLOG / Articles / View

- Articles

Nabors Industries’ Perspective in Q3 2025: KEY Takeaways

By Avik on December 1, 2025 in Articles

Industry Outlook

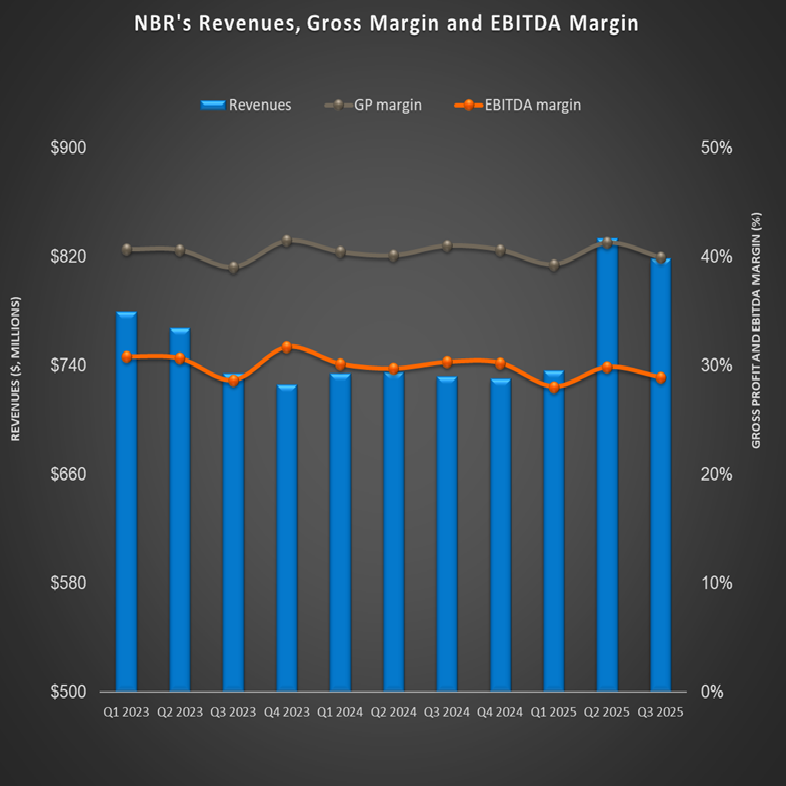

We have already discussed Nabors Industries' (NBR) Q3 2025 financial performance in our recent article. Here is an outline of its strategies and outlook. Crude oil prices have been volatile following the geopolitical uncertainty and its impact on the world energy market. On top of that, mixed signals from tariffs, OPEC production increases, and high inventories are keeping markets uncertain.

Nabors expects U.S. activity to stay soft near term but gradually recover by late 2026, while its international exposure should cushion any short-term weakness. On the gas side, the outlook looks solid as U.S. LNG exports and Middle Eastern projects drive steady rig demand, setting the stage for recovery ahead.

SANAD and International Market Update

Drilling activity in Saudi Arabia has leveled off, but a rebound looks possible as Aramco pushes ahead with plans to boost gas output through 2030. The recent onshore and offshore rig tender could restore up to 50% of the suspended onshore rigs by late 2026. SANAD is performing well, adding another newbuild rig and planning more through 2027 to reach a total of 20 rigs.

Nabors also sees more growth opportunities across the Eastern Hemisphere, with about two dozen potential rig contracts—most in regions where it already operates. In Latin America, activity in Mexico is soft as cash conservation curbs rig demand. However, Argentina is ramping up, with multiple rigs set to start by early 2026, taking its total there to 13.

North America Outlook

According to NBR’s management, the U.S. drilling activity looks steady through 2025, though some operators are tweaking rig counts up or down, creating mild downside risk for Nabors. Rig margins in the Lower 48 slipped in Q3 as higher operating costs outpaced revenue gains, but the company deployed its most powerful rig yet in the Eagle Ford.

Its technology arm, NDS, saw record adoption, averaging seven services per rig and growing third-party revenue despite a shrinking rig market — proof that demand for its high-end drilling solutions is holding strong.

Quail Sale and Parker Synergies

During Q3, Nabors sold Quail Tools for $625 million at roughly 4.2x EBITDA, a sharp premium compared to the 1.4x multiple it paid for the Parker acquisition (in July). The sale effectively valued Nabors shares at around $130 each and helped cut net debt by over 20%. The company plans to use all sale proceeds for further debt reduction while keeping strong-performing Parker assets.

The Parker businesses are expected to generate $55 million in 2025 EBITDA and about $70 million in 2026 as cost synergies build. Integration is on track, with over $60 million in synergies by 2026, strengthening both margins and cash flow.

Nabors expects FY2025 capex to land at $$720 million, with a large share funding the SANAD newbuild rigs. The company guides Q4 CapEx at around $180–$190 million. Free cash flow should be about breakeven for the year. The relatively low eyeball signals delayed collections from PEMEX and the Quail may underperform the earlier guidance.

Relative Valuation

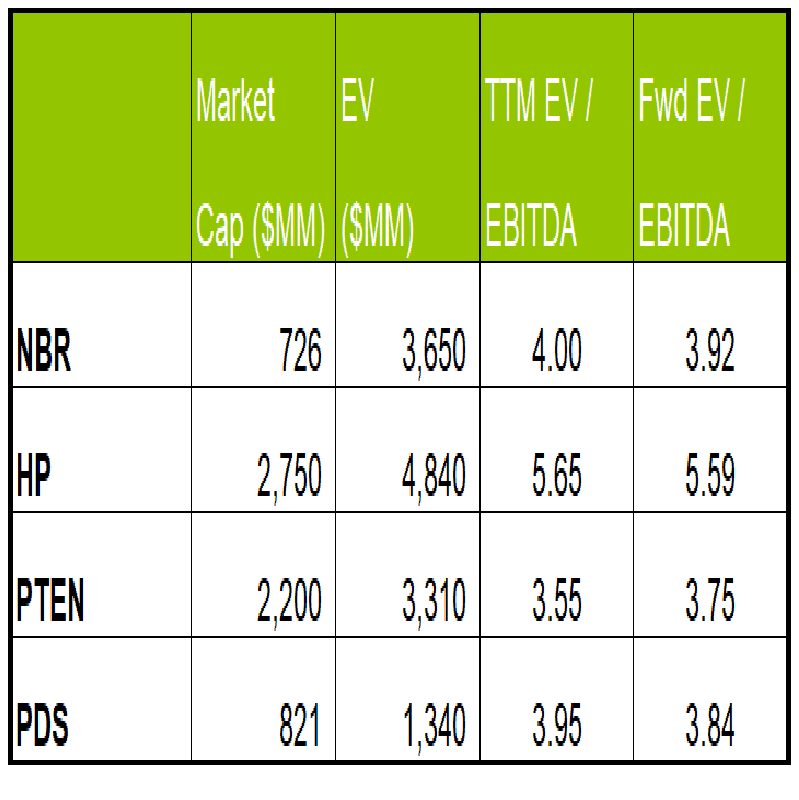

NBR is currently trading at an EV/EBITDA multiple of 4.0x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is lower. The current multiple is also lower than its five-year average EV/EBITDA multiple of 5.9x.

NBR's forward EV/EBITDA multiple versus the current EV/EBITDA is expected to contract, contrasting a mild rise in multiple for its peers because the company's EBITDA is expected to increase compared to a fall in EBITDA for its peers in the next four quarters. This typically results in a higher EV/EBITDA multiple compared to its peers. The stock's EV/EBITDA multiple is lower than its peers' (NINE, PUMP, and ACDC) average of 4.4x. So, the stock is undervalued compared to its peers.

Final Commentary

Nabors sees oil market uncertainty persisting due to tariffs, OPEC supply growth, and inventory overhang, but expects U.S. drilling to stabilize and improve by late 2026. Its international and gas-linked exposure should help offset near-term softness, with LNG and Middle East projects supporting rig demand. In Saudi Arabia, SANAD continues to expand its rig count, and a major tender could restore half the suspended onshore rigs by 2026.

Nabors’ balance sheet got a major boost from the $625 million Quail Tools sale, with proceeds used to cut debt and strengthen leverage. Integration of Parker assets is progressing well, with synergy gains building into 2026, supporting higher cash flow and operational efficiency. The stock is undervalued compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform