Articles

- BLOG / Articles / View

- Articles

NOV's Perspective in Q1 2026: KEY Takeaways

By Avik on May 25, 2026 in Articles

Outlook Explained

In our recent article, we have already discussed NOV's (NOV) Q1 2026 financial performance. Here is an outline of its outlook. NOV’s management estimated that the market initially expected a 2–3 million bpd oversupply driven by non-OPEC growth and easing OPEC+ cuts. This pointed to a challenging 2026, with disciplined North America activity and gradual Middle East recovery.

Offshore was expected to gain momentum as long-cycle supply became more important.

However, the outlook has shifted sharply due to Middle East disruptions. Significant production shut-ins have turned the market from surplus to a meaningful deficit. In onshore, customer demand is starting to improve, with early signs of increased investment following recent market disruptions. In North America, operators are accelerating DUC completions and reconsidering rig reductions, signaling tightening activity.

Middle East Impact & Challenges

According to NOV’s management, onshore service and rental operations saw limited disruption, while capital equipment faced shipping delays and higher freight costs. Logistics rerouting and restricted site access delayed inspections and deliveries. Supply chain issues worsened in March, impacting materials flow, manufacturing throughput, and costs. Aftermarket operations were hit by parts shortages, reduced customer activity, and project suspensions, especially offshore.

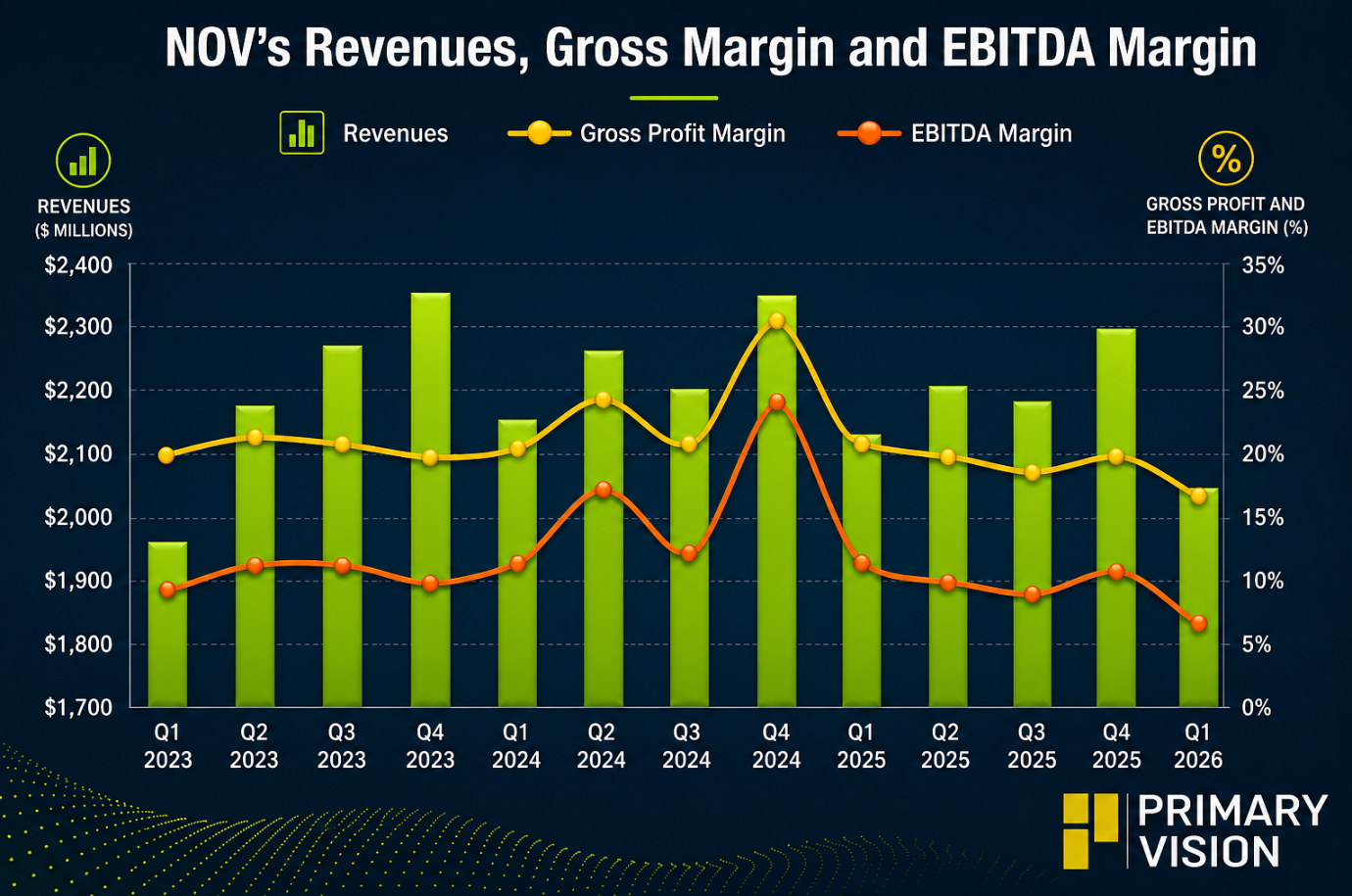

Most disruptions were timing-related, with deliveries delayed rather than canceled. Freight costs surged up to 3–4x, contributing to higher operating costs. The conflict reduced revenue by $54 million and EBITDA by $32 million, though orders remained relatively strong.

Strategic Priority

Service capacity is already tight, and improving pricing will be key to unlocking further investment. International land markets are strengthening, but new equipment will be needed as spare capacity is largely exhausted.

Middle East recovery is expected to drive a rebound in activity, followed by longer-term development programs. Offshore markets are entering a sustained upcycle, supported by improved project economics and rising demand. The company is investing to capture this growth, including expanding subsea capacity to address future supply constraints.

Q2 Forecast

The company’s management concedes that the near-term conditions remain uncertain due to ongoing Middle East disruptions, but the broader outlook is improving. Activity is expected to resume as conditions stabilize, supporting a pickup in industry demand.

NOV is positioned to benefit from increased reinvestment to restore production and capacity.

The company is focused on margin expansion through both revenue growth and cost optimization.

Cost actions, including headcount reduction and facility consolidation, are improving efficiency and profitability.

Relative Valuation

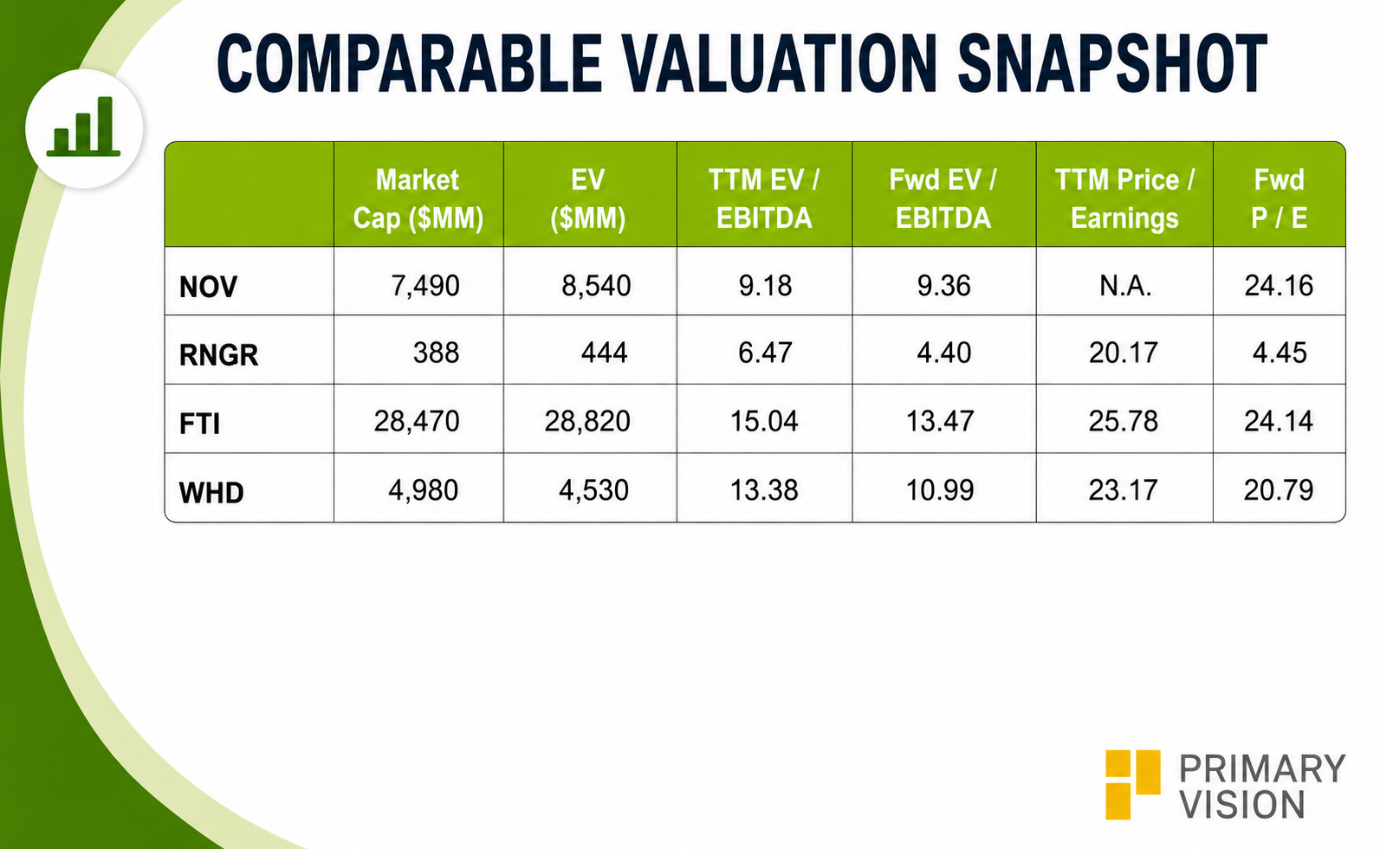

NOV is currently trading at an EV/EBITDA multiple of 9.2x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 9.4x. The current multiple is lower than its five-year average EV/EBITDA multiple of 12.5x.

NOV's forward EV/EBITDA multiple expansion versus the current EV/EBITDA contrasts with its peers because its EBITDA is expected to decrease compared to a rise in EBITDA for its peers in the next year. This typically results in a much lower EV/EBITDA multiple than its peers. The stock's EV/EBITDA multiple is lower than its peers' (RNGR, FTI, and WHD) average of 11.6x. So, the stock is reasonably valued, with a negative bias, compared to its peers.

Final Commentary

NOV’s outlook has shifted from an expected oversupply to a tighter market due to Middle East disruptions. This is already driving early signs of demand recovery, particularly in North America, with increased completion activity. However, near-term performance remains pressured by logistics, supply chain issues, and higher costs. Most of these disruptions appear timing-related, with activity expected to resume as conditions stabilize.

Looking ahead, tightening service capacity, offshore momentum, and international growth support a stronger cycle. Overall, I believe NOV is positioning for recovery through cost discipline, margin expansion, and targeted capacity investments. The stock is reasonably valued, with a negative bias, compared to its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform