Articles

- BLOG / Articles / View

- Articles

NOV's Perspective in Q4 2025: KEY Takeaways

By Avik on March 9, 2026 in Articles

North America Outlook

In our recent article, we have already discussed NOV's (NOV) Q4 2025 financial performance. Here is an outline of its outlook. The U.S. oil market is entering 2026 with oversupply, keeping operators cautious on spending. Activity is expected to decline mid-single digits year over year, with weaker oil-directed work partly offset by stronger gas basins. High inventories create downside risk to prices, limiting near-term upside. A modest recovery is likely by late 2026 into 2027, but fiscal discipline and service capacity constraints should cap growth.

NOV spent the past decade restructuring its business, consolidating operations, and driving efficiency to navigate multiple industry downturns. Ongoing cost actions, including a $100 million cost-out program, have improved working capital. While upstream spending is expected to soften in 2026, these efficiency gains should help offset lower revenue and support EBITDA resilience.

International Market Outlook and Backlog

NOV expects international activity to be “flat to slightly higher” in 2026, led by rig reactivations in Saudi Arabia and growing unconventional work. Expansion across the Middle East, Latin America, and Australia should support demand for high-spec drilling, completion, and production equipment. Over the longer term, Venezuela represents a potential incremental opportunity if industry activity recovers.

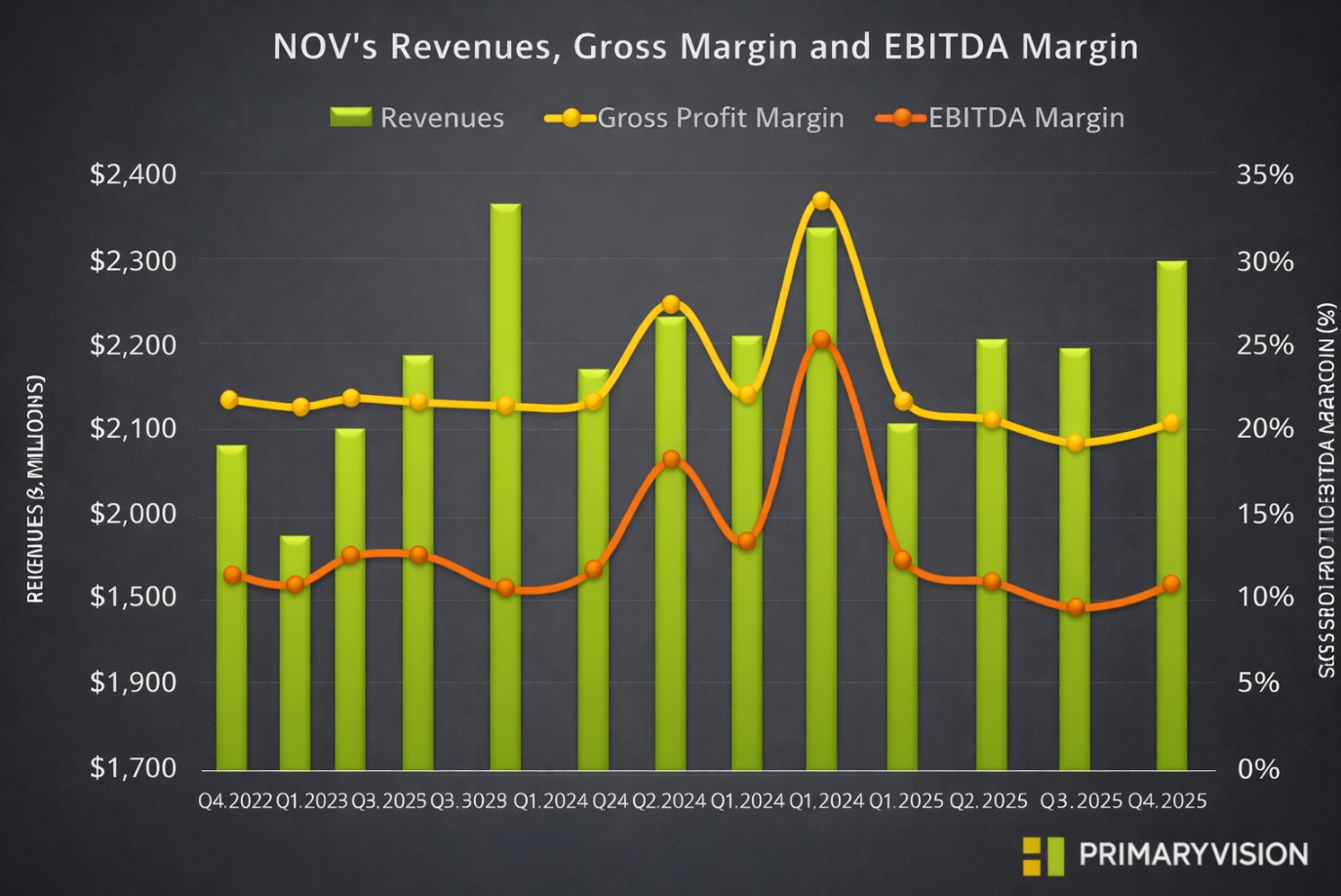

The company ended FY2025 with a $4.34 billion backlog and a book-to-bill of about 91%, supported by a 15% revenue increase from backlog. Offshore production technology demand drove more than 10% growth in offshore backlog and helped deliver another year of revenue growth and margin improvement in Energy Equipment.

Key Segment Drivers and Outlook

Industry forecasts point to low- to mid-single-digit offshore spending declines in 2026, but NOV believes the offshore market is nearing the start of a multi-year upcycle. Offshore economics have improved materially, with breakevens below $40 per barrel in many basins, supporting a shift back toward long-cycle deepwater supply. NOV’s automation, digital solutions, and industrialized FPSO infrastructure have helped lower costs and improve execution.

Looking ahead, management sees the potential for up to 10 FPSO FIDs in 2026 and expects an average of around 8 per year through 2030. While FPSOs may be smaller on average, a higher share is expected in gassier and harsher environments, which aligns well with NOV’s strengths in gas processing and turret mooring systems.

Offshore contracting activity has accelerated, with 59 floater contracts awarded since September 2025 versus 33 a year earlier. Also, open tenders show materially higher rig-day demand. Even though most contracts start in 2027, early rig preparations are already lifting demand for parts, services, and upgrades, supporting improved orders.

Q1 Forecast

NOV expects Energy Equipment revenue to increase 3%–5% year-over-year in Q1, with EBITDA of $145M–$165M. It also expects Energy Products and Services to see a seasonal decline in Q1, with revenue down 6%–8% and an EBITDA of $105M–$125M.

Relative Valuation

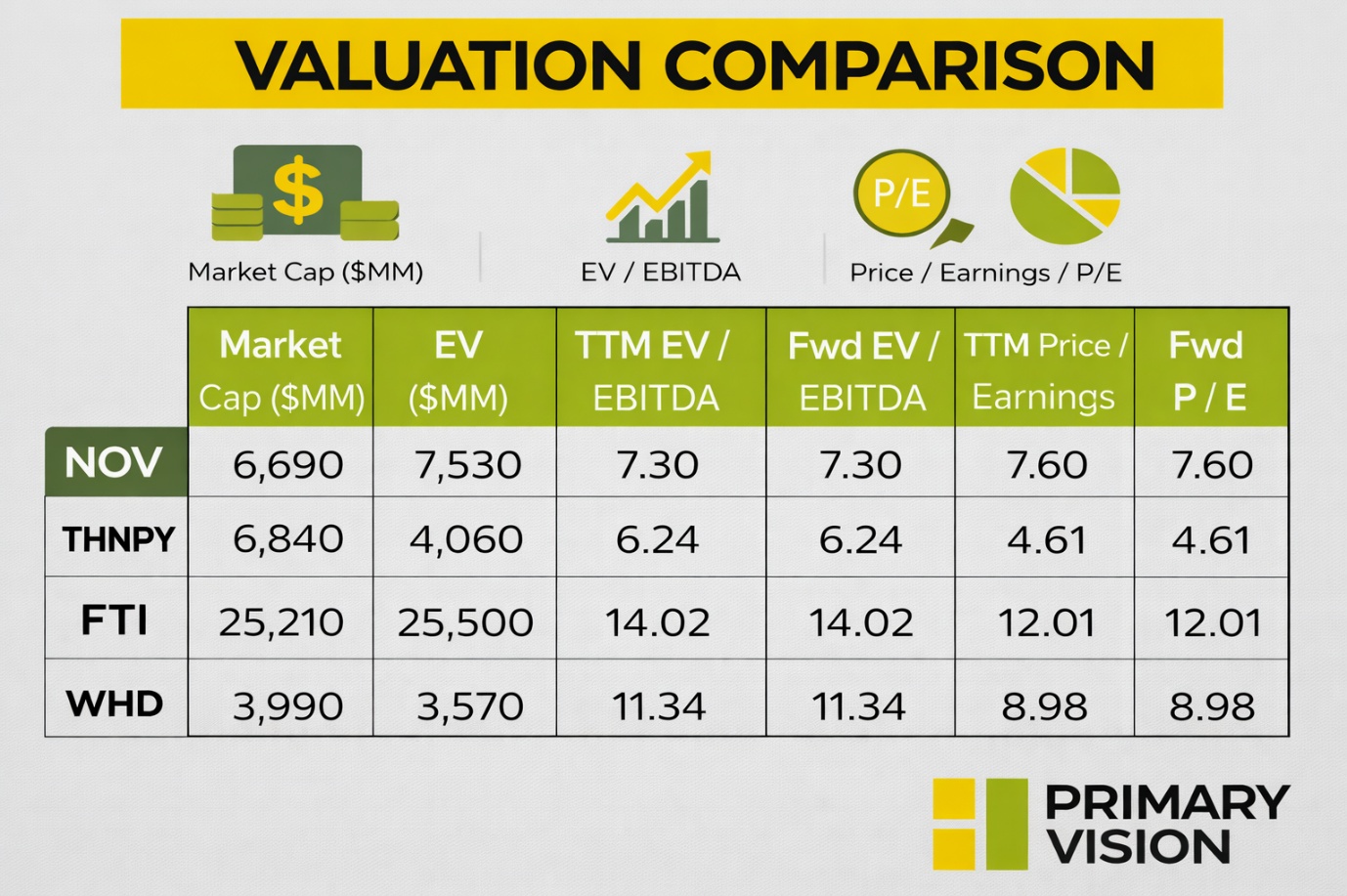

NOV is currently trading at an EV/EBITDA multiple of 7.3x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is 7.6x. The current multiple is lower than its five-year average EV/EBITDA multiple of 12.8x.

NOV's forward EV/EBITDA multiple expansion versus the current EV/EBITDA contrasts with its peers because its EBITDA is expected to decrease compared to a sharp rise in EBITDA for its peers in the next year. This typically results in a much lower EV/EBITDA multiple than its peers. The stock's EV/EBITDA multiple is lower than its peers' (THNPY, FTI, and WHD) average of 10.5x. So, the stock is reasonably valued, with a negative bias, compared to its peers.

Final Commentary

NOV enters 2026 facing a softer U.S. market, with mid-single-digit activity declines and limited near-term pricing upside due to oversupply and high inventories. Cost restructuring and efficiency gains from prior years should help cushion EBITDA despite lower upstream spending. International activity looks more stable, supported by rig reactivations, unconventional growth, and a solid $4.34 billion backlog.

Offshore fundamentals continue to improve, with better economics, rising contracting activity, and a growing pipeline of FPSO opportunities. Near term, segment performance is mixed in Q1, but improving offshore momentum supports a more constructive medium-term setup. The stock is reasonably valued, with a negative bias, versus its peers.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform