Articles

- BLOG / Articles / View

- Articles

Oilfield Services and AI Power Series: How Does AI Power Demand Break the Old Grid Model

By Avik on January 27, 2026 in Articles

Introduction: The bottleneck has shifted

The AI investment cycle is no longer constrained by chips. It is constrained by electricity. Large AI data centers increasingly require 100–500 MW per campus, comparable to adding a midsize city to the grid in a single location. The power system was not designed for this level of load concentration. Utilities plan in decades. AI scales in quarters. That mismatch is structural, and it is already reshaping who supplies power, how it is delivered, and which energy companies remain relevant.

AI is changing how energy companies think about their future. Several are no longer positioning themselves only as oilfield service providers or gas suppliers. They are starting to present themselves as power companies. The strategic logic is clear. Power linked to AI demand promises longer contracts, steadier revenue, and a less cyclical business mix.

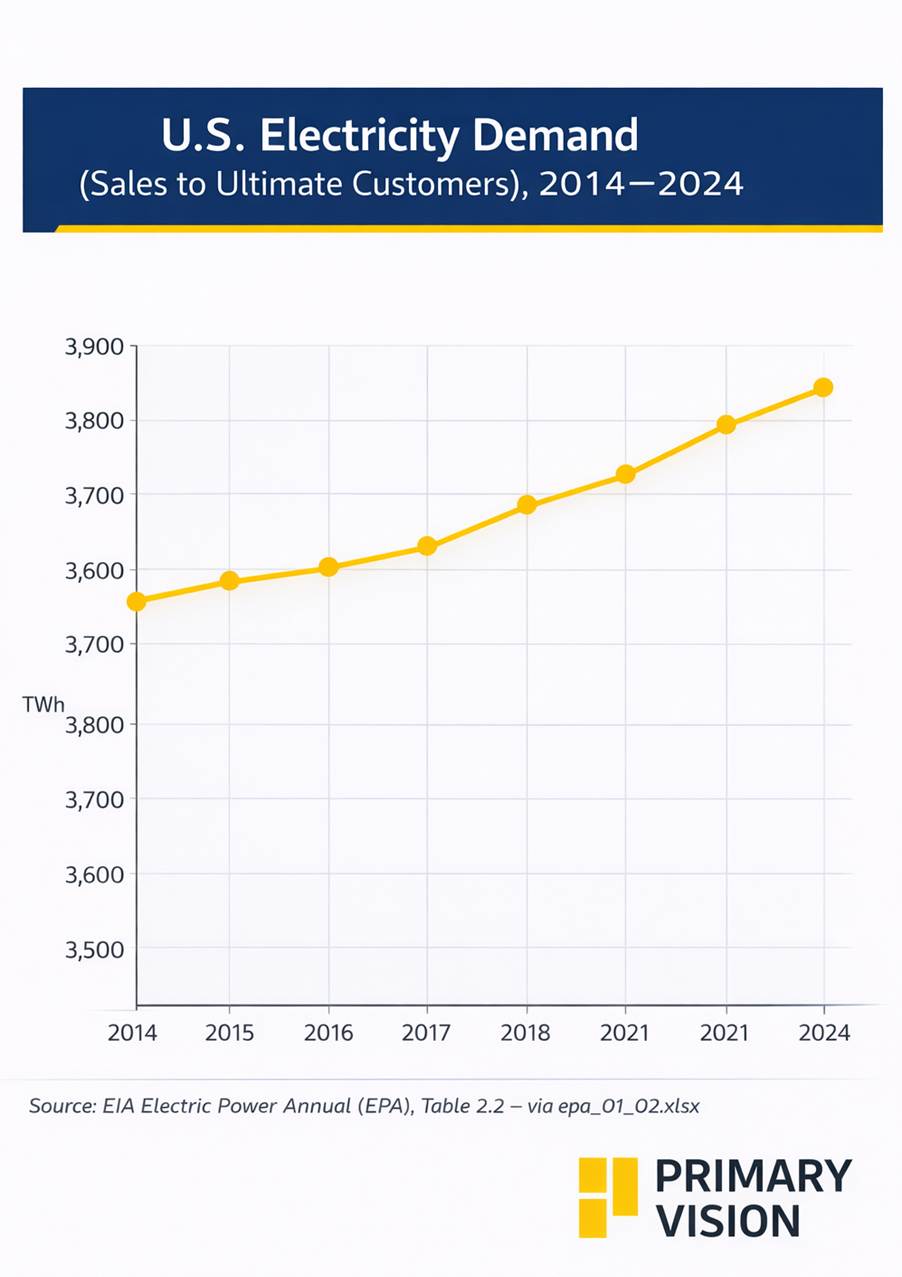

U.S. electricity demand softened between 2014 and 2020, reflecting efficiency gains and weaker industrial activity, before rebounding strongly from 2021 onward. According to the EIA, Demand accelerated through 2022–2024, signaling that structural drivers such as electrification, data centers, and industrial load are now outweighing efficiency offsets. The trajectory suggests demand growth is no longer cyclical noise but a sustained trend with implications for long-term capacity and grid investment.

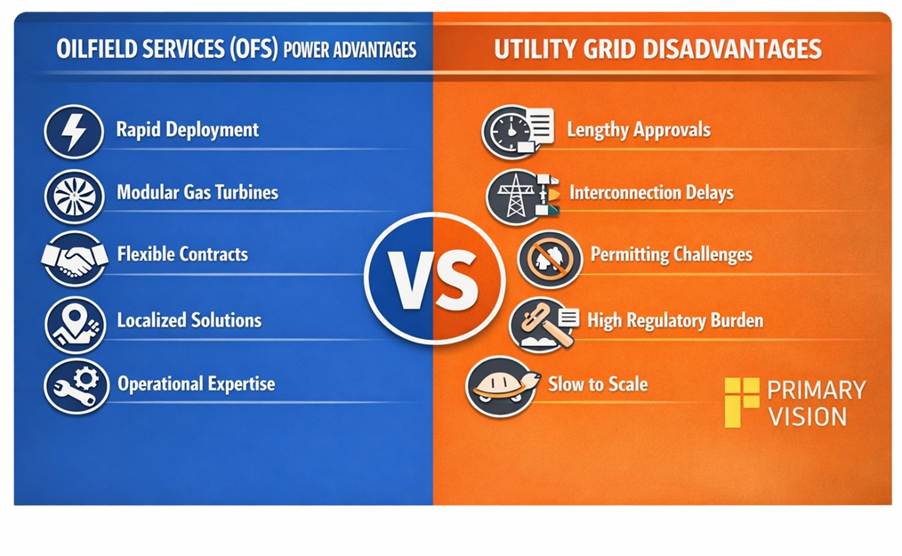

The old grid model was built for stability, not urgency

The regulated utility model works when demand grows gradually. It prioritizes fairness, reliability, and process discipline, which protects the system but also embeds friction. New capacity requires interconnection studies, environmental reviews, regulatory approvals, and cost recovery, stretching timelines by design.

Interconnection queues now span years across major markets, while transmission upgrades face chronic delays and new projects encounter litigation and community opposition. This is not incompetence but the natural outcome of a system built to minimize risk. AI infrastructure demands speed, and the grid’s structure was never designed to deliver it.

Why speed has become the economic variable

For hyperscalers, access to power increasingly determines revenue timing. A delayed data center delays model deployment, product launches, and competitive positioning, which gives speed real economic value. Power is no longer just an input cost; it is a gating factor on growth. Procurement behavior is shifting accordingly.

Buyers are no longer optimizing only for the lowest long-term price but for time-to-power certainty. That shift may appear subtle, but its implications are material. It creates demand for solutions that bypass traditional grid timelines and rewards suppliers who can deliver megawatts quickly, even if those structures sit outside the legacy power ecosystem.

The emerging alternative: OFS-style power supply

Oilfield services (OFS) firms were not designed to be utilities. But their operating model is closer to the problem. These companies already specialize in rapid equipment deployment, distributed operations, complex logistics, fuel coordination, and uptime-critical performance. That operational DNA matters when the core challenge is execution speed.

A new model is emerging. Behind-the-meter generation. Modular gas turbines. Co-located infrastructure. Direct commercial contracts. Power becomes a product rather than a regulated entitlement. Solaris Energy Infrastructure explicitly positions around this model. Its materials emphasize sub-12-month time to power, the ability to scale toward gigawatt-scale campuses, and experience managing complex AI load profiles. That positioning is not cosmetic. It defines the product.

Utilities optimize for process. These new suppliers optimize for deployment velocity. That distinction frames the competitive dynamic.

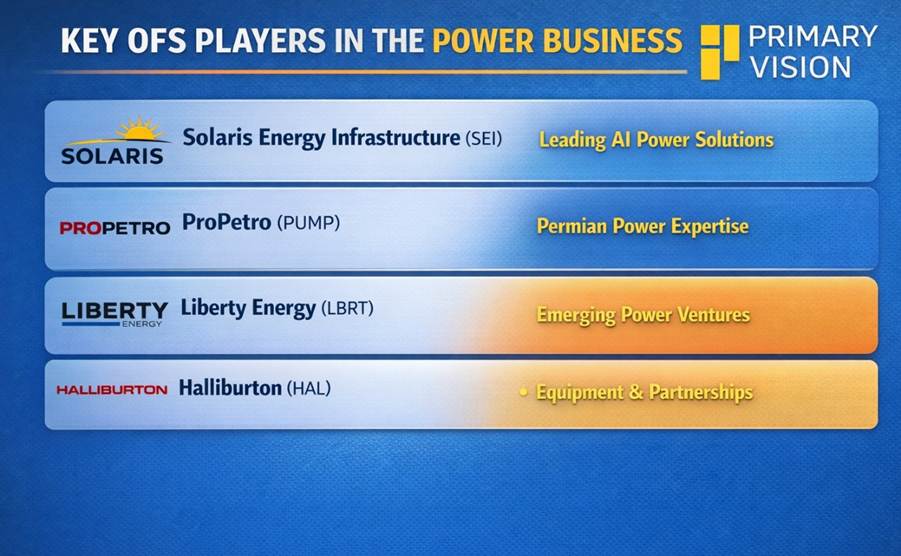

Who is executing versus who is positioning

The materials point to clear differences in maturity, even if most strategies are still evolving. Solaris Energy Infrastructure (SEI) appears furthest along, with disclosed scale ambitions, early customer traction, and investments in in-house technical capability that suggest this is becoming a core business rather than an adjacency. ProPetro (PUMP) is earlier but credible, having created a dedicated power subsidiary, secured meaningful equipment capacity, and explicitly framed data centers and non-oilfield demand as strategic targets, supported by Permian-based geographic advantages.

Liberty Energy (LBRT) has laid strategic groundwork through Liberty Power Innovations and the IMG Energy acquisition, but without disclosed megawatt targets or contracts, the power opportunity remains optionality rather than a valuation driver. Halliburton (HAL) is taking a more asset-light route via partnerships and equipment commitments, which limits capital risk but also caps strategic upside.

So, the dispersion here is real but underappreciated. Some companies are already shaping operating models around power. Others are still building narrative and infrastructure. That distinction will matter — but the real separation will become clearer only as contracts, execution, and financial contribution begin to show.

Geography is not incidental. It is the strategy.

These models only work in specific locations. Gas availability matters. Infrastructure density matters. Regulatory familiarity matters. Land access matters. ProPetro’s positioning is inseparable from the Permian basin, and its disclosures explicitly connect basin economics with future data center demand. That linkage is not incidental. It is foundational.

Solaris is pursuing a broader approach. Its materials target hyperscalers, industrial users, utilities, and microgrids across geographies. That expands the addressable market but also increases technical and execution complexity. Liberty’s current positioning remains closer to adjacency, which is a logical entry point. Whether it can scale beyond that will determine whether the opportunity becomes material.

This is not a national commodity market. It is a locational market. Advantage accrues to those with the right assets in the right places.

Risk Factors: Regulation, litigation, and backlash

Power is political. New entrants inherit risks utilities have managed for decades: air permits, zoning approvals, environmental challenges, community opposition, and grid fairness debates. Legal challenges from incumbents are also likely as private power scales. These risks do not disappear simply because projects are privately contracted.

Scrutiny will rise as large customers increasingly bypass the grid. Regulators will respond. Utilities will defend their position. Local communities will push back. So, regulatory risk is not a question of if, but when. Speed does not eliminate these risks. It only shifts when they surface.

Execution will separate winners from storytellers

Power projects fail for practical reasons. Bad engineering. Weak EPC partners. Equipment underperformance. Overpromised timelines. Poor contract structure. Fuel risk mispricing. Hyperscalers will not tolerate repeated failures. One high-profile miss can permanently damage credibility.

Utilities can absorb missteps because they operate within protected frameworks. New entrants cannot. Primary Vision thinks this theme will not lift all boats. It will be selective, with outcomes determined by execution rather than ambition.

Conclusion: Not a power shortage; it is a timeline conflict

The U.S. does not lack electricity in aggregate. It lacks the ability to deliver large volumes of power quickly to specific locations. That gap has created a new market. Oilfield services companies are attempting to fill it. Some are executing. Some are positioning. Some are narrating.

This is not a low-risk transition. It is capital-intensive, operationally complex, and politically exposed. But the prize is meaningful. Longer contracts. More stable revenue. A structurally improved business mix. Part 1 establishes one conclusion clearly: the grid model cannot meet AI’s timeline. Part 2 will address the harder question: which companies are positioned to benefit, and which are most likely to disappoint.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform